Hope the operator stays calm and should not play the game again, can’t trust kiri after loosing due to operator games earlier, after these results i did not see any operator game, earlier un necessarily the stock use to touch lower than 270 and used to come back with out any reason,

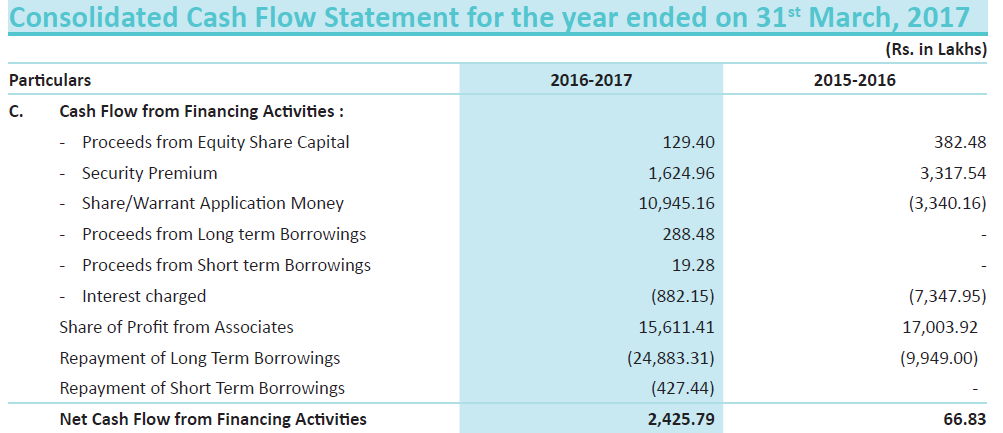

While going through AR for 2016-17, I came across interesting point. Consolidated cash flow The company has shown "Share of profit from associate - Rs. 156.11 Cr under cash in flow from financing activity.

I understand company can show 38% of Dystar’s profit as profit from associates under P&L but Dystar has to declare dividends for Kiri (for the same amount) to show under cash flow of the consolidated company. Am I missing something here?

Disclosure- invested with around 2% of my portfolio

Cant understand why fellow valuepickrs are not talking about kiri?!

Results on monday and expected to be bumper.

The long term uptrend of this stock is truly sensational. I expect the dystar issue to be resolved in favor of kiri in the singapore courts in the next 3 months.

The matter is in a singapore court as is public info.

The next set of dates are in jan. As per my sources we are very positive. I would reccomend following the blog by a fellow valuepickr it specializes in kiri and is truly brilliant. One can never be certain with a court matter, it could take longer than 3 months.

Leaving the court matter aside the valuation of kiri at cmp is very attractive.

a)TOTAL SALEs::: 256 CRORE v/s 237cr QoQ and v/s 260cr YoY

b) NET PROFIT:::::30CRORE v/s 30cr QoQ and v/s 25cr YoY

c) Excise Duty/GST ::::30CRORE v/s 16cr QoQ and v/s 16cr YoY (due to thisGST FACTOR only NP was flat otherwise it would have broken all records)

d) EBITA MARGIN %:::::17% v/s 17% QoQ and v/s 14%YoY

e) EBITA:::::39CRORE v/s 34cr QoQ and v/s 38cr YoY

In the current quarter, exports have grown by53% YoY and 23% sequentially QoQ.

3)KIL has been able to achieve reduction in its outstanding

debt from a peak of Rs.853 Crores to Rs.159 Crores. Though the outstanding

debt of Rs. 159 Crore shall gradually retire by the FY2022, KIL shall not be required to pay any interest on the said debt as the same is converted into Noninterest bearing Securing Receipts.

KIL is focusing on organic growth in the Colors business by upgradation of

facilities, strengthening its product mix and adding dispersed dyes in its portfolio.Capex has already commenced on the Disperse Dyes facility and capacities will

come on stream in a phase-wise manner over the next year and a half. With these in place, the turnover is targeted to double from FY18 to FY20_. Most

important, this expansion will completely capital non dilutive: it will be

entirely funded by KIL’s internal accruals, without resorting to additional

external debt or new equity.

There has been a structural decline in competition as several Chinese players

have either moved out of or stopped growing in the product-markets targeted by

KIL.

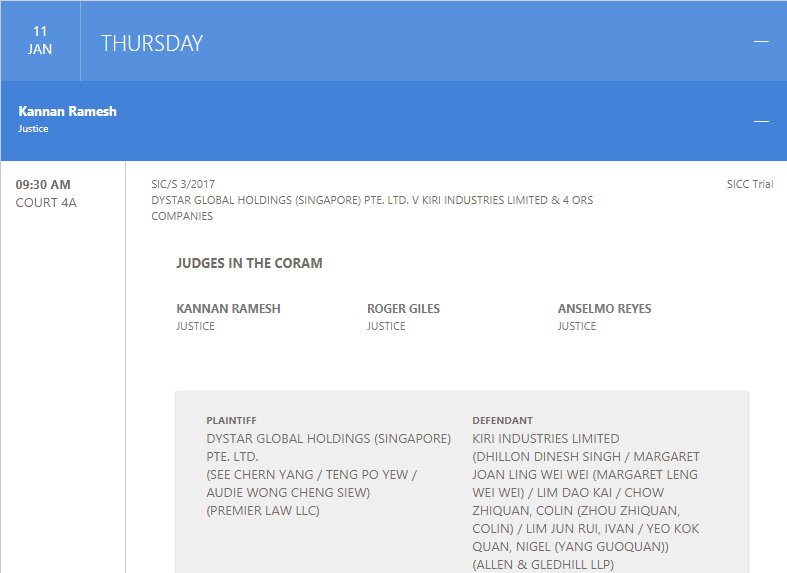

Updates of Court Case in Singapore:

As you may be aware, KIL has filed a case against the majority shareholders of

Dystar for minority oppression in Singapore International Commercial Court (SICC).

Trial of witness of the parties to the legal proceedings are in progress and hearings

were held between November 6, 2017 and November 13, 2017. The further tentative

trial dates are between January 8, 2018 and January 16, 2018.

Kiri remains a value buy despite the huge volatility. Pls visits quora and read Gopal Kavallireddi view on Kiri. Crisp and concise. The recent fall to 500-525 level has been an oppurtuntiy to add to to holdings.