Now that the management has made it amply clear that they will utilize most of DyStar proceeds for the copper venture, I found it worthwhile to evaluate copper dynamics and management’s tall claims.

The Setup: ₹5,854 Crore and a Decision

After an 11-year legal battle with Senda International (DyStar’s parent), Manish Kiri finally got his payday, ₹5,854 crore from the Singapore courts. For context, Kiri Industries is a ₹500 crore revenue dyes company with a market cap of roughly ₹2,700 crore. The DyStar windfall is more than double the company’s entire market capitalization.

So what does the promoter do with this money?

No dividends. No buybacks. No special distribution to the shareholders who waited 15 years for this resolution. Instead, the board announced that the entire sum, after capital gains tax, would be deployed into a greenfield copper smelting and fertilizer complex. The board was explicit: this decision is final and firm (Q3FY26 transcript).

Shareholders who bought Kiri for the DyStar arbitration upside are now, whether they like it or not, investors in a ₹12,000-13,000 crore copper bet. This piece isn’t about whether that decision was fair to minority shareholders (that’s a governance discussion for another day). This piece is about whether the copper bet itself makes any sense, and whether the numbers Kiri’s management is putting out survive contact with reality.

To answer that properly, we need to start from scratch. Because copper smelting economics are genuinely unintuitive, and most of the bull case for Kiri falls apart once you understand how smelters actually make money.

Copper 101: From Rock to Wire

Think of the copper value chain as five stages, each adding value. Kiri is entering at stages 3-5. Understanding all five is essential to evaluating their business model.

Stage 1: Mining (the upstream). Miners in Chile, Peru, the DRC, and Australia dig up copper ore. Raw ore contains only 0.5-2% copper. The rest is rock, sulfur, iron, and trace metals — sometimes gold and silver. India has almost no copper mining. Hindustan Copper produces a mere ~25,000 tonnes annually, which is a rounding error in global terms. This is, by far, the most profitable part of the chain. Interestingly, Kiri is in active discussions to acquire a 20-40% stake in Makilala Mining Corporation in the Philippines (via Celsius Resources/Maharlika), which has an annual production capacity of 120,000 tonnes - more than 4x Hindustan Copper’s entire output (but <25% of Kiri’s RM requirement). Production is targeted for December 2027, roughly matching Kiri’s smelter timeline.

Stage 2: Concentrating. At the mine site, ore is crushed, ground, and processed using flotation (chemicals make copper particles float, rock sinks). The output is copper concentrate, a powder that’s 20-30% copper. This is what gets shipped globally in bulk carriers. This is what Kiri will be importing: roughly 1.2-1.7 million tonnes of concentrate annually to produce 0.5 million tonnes of refined copper (the ratio is approximately 2.5-3:1 because concentrate is only ~25-30% copper, with processing losses on top).

Stage 3: Smelting. This is the core of what Kiri is building. Concentrate is fed into a smelter — essentially a giant furnace operating above 1,200°C. The sulfur in the concentrate burns off as SO₂ gas, which is captured and converted to sulfuric acid (remember this, it becomes critical later). Iron separates as slag. The output is copper matte (~60-70% Cu), which is further processed into blister copper (~98.5% Cu), and then cast into anodes. The technology choice matters here; Kiri claims they’re using the latest generation tech, likely a top-blown or bottom-blown converter similar to what dominates Chinese smelting (about 80% of global capacity uses variants of flash smelting or Chinese-developed furnace technology).

Stage 4: Refining. Copper anodes are placed in electrolytic tanks. Electric current dissolves the anode and deposits 99.99% pure copper onto cathode sheets. The impurities settle at the bottom as “anode slime” and this is a meaningful profit center, because that slime contains gold, silver, platinum, selenium, and tellurium. The output is LME-grade copper cathode: the globally traded commodity, the benchmark product.

Stage 5: Downstream/Fabrication. Cathodes are melted and cast into copper rods (continuous cast rod, or CCR), drawn into wire, or manufactured into tubes, foils, and strips. This is where the biggest domestic value-add happens. A cathode sells at the LME price. A copper rod sells at LME plus a premium (₹5,000-15,000/tonne). Copper tubes command even higher premiums. Kiri plans to convert 3 lakh out of 5 lakh tonnes into rods and tubes in-house, this is a good strategy if they can execute, because it captures the fabrication margin instead of letting it leak to standalone converters.

The Kiri-specific twist — Integrated Fertilizer. Smelting generates massive quantities of sulfuric acid as waste, roughly 3-4 tonnes of acid per tonne of copper produced. Most smelters sell this acid into the chemical market, often at thin margins. Kiri’s plan is to react this sulfuric acid with imported rock phosphate to produce phosphoric acid, then combine it with ammonia to manufacture DAP/NPK fertilizer. This converts a waste product (or low-value by-product) into a high-value product with a captive end-market. Hindustan Zinc does exactly this with zinc smelting waste acid. It’s a proven integration model, more on whether it actually changes the economics later.

The Part Nobody Understands: TC/RC and How Smelters Actually Make Money

This is the heart of smelter economics. Get this wrong and every subsequent analysis is garbage.

A copper smelter does not buy copper cheaply and sell it at a markup like a trader. A smelter provides a processing service. The economics work like this:

A miner ships copper concentrate to a smelter. The contract specifies that the smelter will convert this concentrate into refined copper. The smelter’s compensation for this processing service is the TC/RC — Treatment Charge and Refining Charge.

TC (Treatment Charge): A fixed fee per dry metric tonne of concentrate processed. Historically in the range of $50-100/tonne.

RC (Refining Charge): A fee per pound of refined copper produced. Historically 5-10 cents/lb.

Let’s make this concrete. Say a Chilean miner ships 1,000 tonnes of concentrate to Hindalco’s Dahej smelter. The concentrate is 25% copper, so it contains 250 tonnes of copper metal. The contract says Hindalco will pay the miner for 96.5% of the contained copper at the LME price, minus the TC/RC fees. The remaining 3.5% — roughly 8.75 tonnes of copper — is the smelter’s to keep. It’s baked into the commercial terms as part of the smelter’s compensation. (I’ll come back to this “free copper” concept, it confused me initially too.)

Here’s the critical thing to understand: the smelter buys the concentrate outright. The miner gets cash. The smelter keeps all the physical copper it produces, sells it in the domestic market, and its profit comes from the spread between what it paid the miner and what it realizes from selling the refined output plus all the by-products. The miner never sees any copper back.

So when Kiri says they’ll produce 5 lakh tonnes of copper and convert 3 lakh into rods/tubes, that’s 5 lakh tonnes of their copper to sell however they want. They’re not retaining some small fraction from toll processing. They’re buying raw material (concentrate), processing it, and selling the finished product.

The TC/RC Crisis: Why 2025 is the Worst Year in Smelting History

The TC/RC fee was traditionally a comfortable revenue stream for smelters. At $80/tonne TC (the 2024 benchmark), a smelter processing 1.5 million tonnes of concentrate earned roughly $120 million just from TC fees alone, before counting any other revenue.

Then 2025 happened.

The annual benchmark TC/RC collapsed to $21.25/tonne and 2.125 cents/lb, already a record low. Spot terms in Asian markets went further, falling to zero and then negative, hitting approximately minus $60/tonne in 2025.

Read that again. At negative TC/RCs, the smelter is literally paying the miner for the privilege of processing their concentrate. Traditional smelting economics completely inverted.

Why did this happen? Two forces collided. On the supply side, China built an enormous amount of smelting capacity — over 60 smelters — over the past decade, driven by strategic industrial policy (China wants to process raw materials domestically rather than import refined copper). On the demand side, mine supply didn’t keep up. The closure of First Quantum’s Cobre Panama mine in 2023 was a major trigger, removing roughly 350,000 tonnes of annual concentrate supply. The result: too many smelters chasing too little concentrate. The global copper concentrate market went into a deficit of roughly half a million tonnes in 2025, and a similar deficit is expected in 2026.

Why don’t smelters just… stop? This was my first question too. If you’re paying to process material, why not shut down?

Several reasons, and they reveal a lot about the industry’s structure:

First, by-products can make the total equation still profitable even at negative TC/RCs. A smelter’s P&L isn’t just the TC/RC line. Even at -$60/tonne TC, if sulfuric acid earns you +$100/tonne equivalent, and gold/silver from anode slimes earns another +$80, and you keep 3-5% “free copper” worth +$150, the basket of revenues still generates positive contribution margin. Chinese smelters in particular have been maintaining profitability through surging sulfuric acid prices, which have offset the negative concentrate processing margins.

Second, shutting down a smelter is catastrophically expensive. These furnaces operate at 1,200°C+ continuously. Shutting one down and restarting requires months, costs tens of millions of dollars, can damage the refractory lining, and triggers take-or-pay penalties on long-term concentrate contracts. Workers disperse and are hard to rehire. Smelters often prefer to lose money on the TC/RC line while keeping the furnace running, rather than face the even larger losses of a shutdown-restart cycle.

Third, China’s smelters operate under a national strategic mandate. China needs refined copper for its EV, grid, and manufacturing sectors. The government would rather subsidize smelting losses than become dependent on imported refined copper. This isn’t pure market economics — it’s industrial policy.

Fourth, most volume is on annual contracts, not spot. Many smelters locked in the $21/tonne benchmark for 2025. Spot has gone to -$60, but the bulk of their volume isn’t at spot. The blended realized TC/RC is still positive for most smelters. It’s only the marginal incremental tonnes that are at deeply negative rates.

And fifth, non-Chinese smelters ARE shutting down. Japan’s JX Advanced Metals announced output cuts. Mitsubishi Materials stated conditions have significantly deteriorated. Glencore received a government bailout to keep its Mount Isa smelter in Australia running. The equilibrium will eventually be reached when enough non-Chinese capacity exits — but “eventually” can take years.

Anatomy of a Smelter’s EBITDA: The ₹60,000/Tonne Breakdown

This is the part that surprised me most. Hindalco’s copper business earned roughly ₹3,025 crore EBITDA in FY25 on approximately 500,000 tonnes of production. That works out to about ₹60,500/tonne, or roughly $720/tonne.

But if TC/RC was only ~$25/tonne on concentrate, how is Hindalco earning $720/tonne of EBITDA on refined copper? Because TC/RC is just one of six revenue streams. Here’s how the full EBITDA per tonne breaks down approximately:

TC/RC income (~₹5,000-7,000/tonne of copper): At the 2025 benchmark of ~$25/tonne on roughly 2.5 tonnes of concentrate per tonne of copper, plus the RC, this gives about $50-80 per tonne of refined copper. In FY24 when the benchmark was $80/tonne, this component alone was ₹15,000-20,000/tonne — which is precisely why Hindalco’s EBITDA (from copper) dropped sharply from FY25 to Q3 FY26.

“Free copper” (~₹6,000-10,000/tonne): Smelters retain 3-5% of the copper content that isn’t “payable” to the miner. On 500,000 tonnes of refined output, that’s roughly 15,000-25,000 tonnes of copper that Hindalco didn’t pay the miner for. At $9,500/tonne LME, that’s $150-240 million, spread across all tonnes sold.

Sulfuric acid (~₹21,000-28,000/tonne at current elevated prices): A smelter generates roughly 3.5 tonnes of sulfuric acid per tonne of copper. At the currently elevated acid prices of ₹6,000-8,000/tonne, this contributes ₹21,000-28,000 per tonne of copper. In normal years (acid at ₹3,000-4,000/tonne), this drops to ₹10,500-14,000. This is the single largest swing factor in smelter economics — and the one most investors miss.

Precious metals (~₹10,000-20,000/tonne): This depends entirely on the quality of concentrate. Chilean concentrate has decent gold content. Hindalco produces gold and silver bars at its Dahej refinery. With gold at $2,600+/oz, precious metal recovery can contribute ₹10,000-20,000 per tonne of copper. This is variable and somewhat unpredictable, but it’s meaningful.

Domestic cathode premium (~₹3,000-5,000/tonne over LME): India is a net importer of refined copper. Buying domestic from Hindalco takes 7-15 days; importing takes 45-90 days with LC/advance payment and logistics friction. Domestic buyers will pay ₹3,000-5,000/tonne more to avoid the working capital hit and quality uncertainty of imports.

CCR rod premium (~₹5,000-10,000/tonne): When Hindalco sells a continuous cast rod instead of a cathode, it earns an additional conversion premium. With over 70% of their copper going out as rods, this is a substantial contributor.

Adding it up:

| Component | Per Tonne of Copper Sold |

|---|---|

| TC/RC (at ~$25 benchmark, blended) | ₹5,000-7,000 |

| Free copper (3-5% payable deduction) | ₹6,000-10,000 |

| Sulfuric acid (current elevated prices) | ₹21,000-28,000 |

| Precious metals (gold, silver, selenium) | ₹10,000-20,000 |

| Domestic premium + rod/tube premium | ₹8,000-15,000 |

| Total gross revenue uplift | ₹50,000-80,000 |

| Less: Operating costs (power, labor, maintenance, logistics) | (₹20,000-30,000) |

| Net EBITDA per tonne | ₹30,000-50,000 |

Hindalco’s FY25 figure of ₹60,500/tonne was at the high end because it was a perfect storm: elevated acid prices, still-decent TC/RCs from legacy annual contracts, record gold prices, and a weaker rupee. In Q3 FY26, EBITDA has dropped to ₹595 crore (annualized ~₹2,400 crore), roughly ₹48,000/tonne — as TC/RCs collapsed despite higher copper prices. The acid revenue partially offset the TC/RC decline.

The crucial insight for investors: Sulfuric acid alone constitutes 30-40% of a copper smelter’s EBITDA in the current environment. In normal acid price years, it’s 20-30%. This means a copper smelter isn’t just exposed to the copper cycle — it’s simultaneously exposed to the chemicals cycle, the precious metals cycle, the currency cycle, and trade policy. It is, emphatically, a deeply cyclical, multi-variable commodity business. Hindalco’s copper EBITDA has ranged from roughly ₹1,400 crore (FY21) to ₹3,025 crore (FY25) on essentially the same assets — a 2x swing purely from external cycles. On a highly leveraged balance sheet (which is what Kiri will have), that swing can be equity-destroying.

The Copper Cycle: When Does Supply Meet Demand?

Two separate cycles interact here, and understanding their phase relationship is essential:

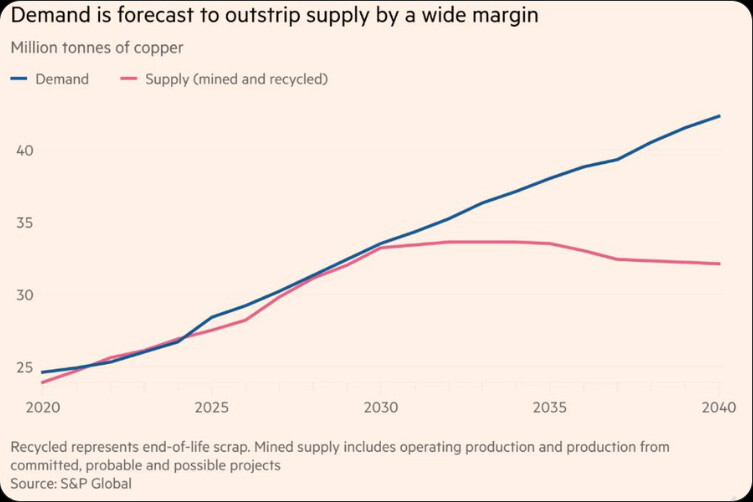

The Mining Cycle (concentrate supply): New copper mines take 10-15 years from discovery to production: permitting, environmental approvals, financing, construction, all painfully slow. Current global mine output is ~22-23 million tonnes. The pipeline of new projects is thin because exploration spending was depressed during 2015-2020. The global concentrate deficit is expected to persist through at least 2027-2028.

The Smelting Cycle (refining capacity): Smelters take 3-5 years to build and are being erected much faster than mines. China has added massive capacity. In India alone, Adani (0.5 MTPA), Kiri (0.35 MTPA primary smelting + 0.15 MTPA secondary), and Hindalco (expansion by ~0.2 MT) are all coming online between 2025 and 2029. Globally, there’s smelter overcapacity relative to concentrate supply, but an undersupply of refined copper relative to end-use demand. This is the fundamental tension.

The Demand Cycle: India’s copper demand is currently ~1.7-1.8 million tonnes (about 6-7% of global consumption of ~26-27 MT, not 10% as sometimes claimed; the 10% figure is a projection for 2050). Demand is projected to reach ~3.2 million tonnes by FY2030, driven by electrification, construction, and the EV transition. Current domestic production plus Adani’s ramp-up gets India to maybe 1.3-1.5 MT by 2027-28. The gap remains enormous, and the import substitution opportunity is real.

When does it normalize? The concentrate squeeze probably eases around 2028-2030 as new mines in Chile, Peru, and the DRC come online. TC/RCs should recover from current negative levels toward the $30-50/tonne range. But the “golden era” of $80+/tonne is probably gone for a long time due to structurally higher global smelting capacity.

For Kiri specifically, their smelter commissioning in late CY2028 could actually time reasonably well with concentrate markets loosening. But they’ll still face 2-3 years of ramp-up in what could remain a tough margin environment.

Kiri’s Actual Plan: Timeline and Capacity

Let me lay out what Kiri’s management described in the Q3 FY26 call, because the timeline details matter enormously and are easy to misread:

Phase 1 (April 2027): Downstream plants only. Copper rod mill, copper tube mill, potentially copper foil facility. These plants will buy LME-grade copper cathodes from the open market — either imported or purchased from Hindalco/Adani — and convert them into rods and tubes. This is a fabrication business. It’s capital-light relative to smelting, equipment deliveries are shorter, and construction is simpler. The full 3 lakh tonne downstream capacity could theoretically be available from early operations, though utilization will ramp gradually.

Phase 2 (End CY2028): Smelter + refinery + fertilizer plant. These come online together (they have to, the smelter’s waste acid feeds the fertilizer plant). Once the smelter is running, the downstream plants switch from buying cathodes externally to consuming their own. This is when the fully integrated economics kick in.

The integrated smelter-to-tube chain therefore starts, at the earliest, in late CY2028, more realistically H1 CY2029 after commissioning issues. First-time operators almost always encounter delays. Even Adani’s Kutch Copper, backed by vastly deeper resources, was delayed by over a year from its original schedule (https://www.bloomberg.com/news/articles/2025-06-18/india-s-new-copper-plant-finally-starts-amid-acute-ore-shortage).

This has a critical implication that I think many investors are missing:

Kiri’s FY28 revenue guidance of ₹20,000-25,000 crore is based purely on downstream rod/tube fabrication using purchased cathodes. The smelter won’t be running in FY28 (April 2027 to March 2028). So while the topline math works, 2.5-3 lakh tonnes of rods × ₹8 lakh/tonne (the copper price is largely pass-through) = ₹20,000-24,000 crore, the EBITDA profile is entirely different from what an integrated smelter generates. You’re earning only the fabrication premium: maybe ₹5,000-10,000/tonne, which translates to ₹150-300 crore of EBITDA at best.

Management guided ₹1,200-1,500 crore EBITDA for FY28. Basis my research, that number is essentially impossible from just rod/tube conversion on purchased cathodes. They’re likely baking in the smelter starting mid-year which is the aggressive timeline risk. If the smelter slips to mid-2029 (entirely plausible for a first-time execution), FY28 and FY29 EBITDA will look nothing like what management presented.

Benchmarking Kiri Against Hindalco and Adani

Now let’s see if Kiri’s steady-state guidance — ₹4,500-5,000 crore EBITDA “within 3-4 years” of full operations — survives comparison with the two players who actually operate copper smelters in India.

Hindalco (Birla Copper, Dahej)

India’s largest copper producer. Fully integrated: smelter → refinery → CCR rod mill → copper tubes → copper foils (recently commissioned for EV batteries). They’ve operated for 25+ years, have fully depreciated core assets, captive power, a captive jetty, and established long-term concentrate supply agreements. They’re the world’s second-largest copper rod producer outside China.

FY25 (record year): Revenue ~₹54,000 crore, EBITDA ₹3,025 crore on ~500 KT. Margin: 5.6%. EBITDA per tonne: ₹60,500.

Q3 FY26 (current environment): Revenue ₹18,233 crore, EBITDA ₹595 crore. Annualized: ~₹2,400 crore. Margin: ~3.3%. EBITDA per tonne: ~₹48,000.

Adani (Kutch Copper, Mundra)

Brand new 0.5 MTPA smelter, started June 2025. Latest-generation technology, captive jetty at India’s most advanced private port (Mundra), backed by the Adani Group’s balance sheet and industrial execution capability. Still ramping up as of Q3 FY26, Robbie Singh noted on the concall that full utilization was expected “over the next 2-3 months.”

Adani’s EBITDA guidance at 70-80% utilization: ₹2,800-3,100 crore. That works out to roughly ₹80,000/tonne, significantly higher than Hindalco’s best-ever year. Adani’s potential justification: newer technology with better efficiency, by-product pricing at current elevated levels, Mundra’s logistics advantage, and downstream integration from day one.

Now here’s the Kiri comparison that should make you pause.

| Parameter | Hindalco (FY25 record) | Adani (guidance at 70-80%) | Kiri (steady-state guidance) |

|---|---|---|---|

| Production | ~500 KT | 350-400 KT | 500 KT |

| EBITDA | ₹3,025 Cr | ₹2,800-3,100 Cr | ₹4,500-5,000 Cr |

| EBITDA/tonne | ₹60,500 | ~₹80,000 | ₹90,000-100,000 |

| Promoter track record | 30+ years in copper | Adani Group | Dyes company |

| Plant age | 25+ years, depreciated | Brand new | Not yet built |

| Current status | Fully operational | Still ramping (8+ months in) | Ground-breaking stage |

Kiri’s steady-state EBITDA per tonne is higher than both Hindalco’s best year and Adani’s optimistic guidance. For a first-time operator with zero prior experience in metallurgy, this doesn’t add up.

Yes, the fertilizer by-product helps explain some of the gap — maybe ₹400-600 crore of additional EBITDA from converting waste acid to DAP/NPK at advantaged costs. But even netting that out, Kiri’s implied copper EBITDA of ₹3,900-4,400 crore on 5 lakh tonnes is ₹78,000-88,000 per tonne. Still higher than Adani’s guidance, with far less execution credibility.

My Realistic EBITDA Estimate

Building it from components at steady state (FY31-32 at earliest, full ramp-up):

| Component | Conservative | Optimistic |

|---|---|---|

| Copper smelting/refining | ₹1,500 Cr | ₹1,900 Cr |

| Downstream rod/tube premium | ₹200 Cr | ₹300 Cr |

| Precious metals recovery | ₹200 Cr | ₹500 Cr |

| Fertilizer (1.1 MT at advantaged costs) | ₹330 Cr | ₹550 Cr |

| Total | ₹2,230 Cr | ₹3,250 Cr |

A realistic range is ₹2,200-3,250 crore at peak steady state, assuming everything goes right. That’s roughly 50-65% of what management is guiding. The only way to get to ₹4,500 Cr+ is to simultaneously assume copper prices rise to $12,000+/tonne, TC/RCs recover to $50+/tonne, acid prices stay elevated, precious metal recovery is exceptional, and utilization exceeds 90% from year three. All of these happening together is a bull case, not a base case.

The Fertilizer Angle: Clever or Bullshit?

I was initially skeptical of this. Layering a fertilizer plant on top of a copper smelter sounds like “vertical integration for the sake of the investor presentation.” But after digging in, I think it’s actually the smartest part of Kiri’s plan.

Here’s why:

Most smelters are at the mercy of the sulfuric acid spot market. When acid prices are high (like now — ₹6,000-8,000/tonne due to tight sulfur markets and fertilizer demand), selling acid directly is more profitable than converting it. Hindalco does exactly this, and their Q2 FY26 results specifically called out higher acid realization as the offset to collapsing TC/RCs.

But acid prices are violently cyclical. Over the past 20 years, prices have spent roughly 12 years below $60/tonne, with sharp spikes to $150-300/tonne during supply squeezes (2008, 2024-25). When Adani’s smelter + Kiri’s smelter + Hindalco’s expansion all come online simultaneously, they’ll collectively dump over 5 million tonnes of additional sulfuric acid on the Indian market. Prices could crash back to ₹2,000-3,000/tonne. At those prices, the acid contribution to smelter EBITDA drops from ₹21,000-28,000/tonne of copper to ₹7,000-10,000/tonne. That’s a ₹5,000-8,000 crore swing across the entire Indian copper smelting industry.

The fertilizer plant gives Kiri a captive buyer for its own acid at any price. By converting acid to DAP/NPK fertilizer, Kiri guarantees a floor value for its acid output regardless of spot market conditions. Even in a crashed acid market, the fertilizer conversion margin is worth more than dumping acid at ₹2,000/tonne. It’s an insurance policy against the chemical cycle.

Why didn’t Hindalco or Adani do this? They don’t need to. Hindalco has 25 years of acid offtake relationships with established buyers. Adani has the balance sheet to ride out acid price cycles. Building a fertilizer plant requires ₹2,000-3,000 crore of additional capex, importing rock phosphate (another commodity chain), setting up agricultural distribution networks, and dealing with the government’s Nutrient Based Subsidy (NBS) regime. These are metals companies — they don’t want to be in fertilizer distribution. Kiri, as a new entrant with no existing acid offtake relationships, is in a different position. The captive consumption hedge makes more strategic sense for them.

The margin reality, though, is modest. Indian fertilizer is heavily regulated. DAP/NPK margins are typically ₹2,000-4,000/tonne EBITDA under the NBS regime. But Kiri’s structural cost advantage, near-zero raw material cost for sulfuric acid, which everyone else has to buy at market price, could give them ₹3,000-5,000/tonne EBITDA. At 1.1 million tonnes, that’s ₹330-550 crore. Meaningful, but it’s not going to transform the overall picture. India imports 8-9 million tonnes of phosphatic fertilizer annually, so 1.1 MT is digestible without creating oversupply domestically.

The Red Flags

1. The Debt Overhang

After capital gains tax on the DyStar proceeds, Kiri will have roughly ₹4,000-4,500 crore of equity for a ₹12,000-13,000 crore project. That means they need ₹8,000-9,000 crore in project debt, roughly 65:35 or 70:30 debt-to-equity.

At 8-9% cost of debt, annual interest alone is ₹700-900 crore. Add principal repayment starting year 2-3 of operations (₹750-1,000 crore annually on a 10-12 year schedule), and total debt service is ₹1,500-1,800 crore per year. Against my realistic EBITDA range of ₹2,200-3,250 crore, the Debt Service Coverage Ratio is 1.2-2.2x. Banks want 1.3x minimum. There’s very little room for error in a bad cycle.

The real danger zone: EBITDA below ₹1,500 crore makes the project stressed. Below ₹1,200 crore, it’s in trouble. Below ₹800 crore, it’s NPA territory. And remember: Hindalco’s EBITDA on the same capacity has fluctuated between ₹1,400 crore and ₹3,000 crore purely from external cycles. On Kiri’s leveraged balance sheet, a cyclical trough could mean the difference between a 3x return and capital destruction.

A point worth noting: even if EBITDA is ₹1,000 crore, the company can technically pay ₹800 crore of interest. But that ignores depreciation (~₹600-800 crore annually on ₹12,000+ crore of assets), principal repayment, and working capital needs. A copper smelter needs massive working capital: at any given time, you’ve got ₹3,000-5,000 crore of copper inventory in various stages of processing. If copper prices drop 15%, your inventory value drops ₹500-700 crore, triggering margin calls. The “₹1,000 crore EBITDA means we can service debt” framing ignores all of this.

Financial closure hasn’t been confirmed yet. Manish Kiri said “before end of March” on the Q3 FY26 call. If it slips, it’s the first red flag that execution won’t match the presented timeline.

2. Execution Risk: The Sterlite Parallel and Beyond

Every copper smelter conversation in India eventually comes back to Vedanta’s Sterlite plant in Tuticorin. That plant was shut permanently in 2018 after community protests (13 people were killed by police) driven by 23 years of documented environmental violations, gas leaks causing respiratory issues, groundwater contamination with arsenic at 20x permissible limits, proximity to a biosphere reserve, and a consistently adversarial relationship with the local community.

Can Kiri face the same risk? The specific Tuticorin scenario is unlikely: Kiri’s plant is in Gujarat (politically far more industry-friendly than Tamil Nadu), it’s greenfield with modern emission technology, and the regulatory environment is different. But the fundamental risk doesn’t disappear. Copper smelting inherently produces SO₂ emissions, heavy metal contaminated slag, and effluent discharge. One major gas leak, one groundwater contamination incident, and the entire project faces existential regulatory action. This risk is manageable through world-class EHS compliance, but it’s never zero.

Beyond environmental risk, the execution concern is simpler: this is a dyes company building one of the largest copper smelters in India, with no metallurgical experience, in a project 20x the size of anything they’ve ever attempted. They’ve hired TCE as owner’s engineer, which is competent but not a substitute for in-house metallurgical expertise. The CEO leading the copper division (Ranjit Singh Chugh), his credentials and track record weren’t elaborated in the transcript, which itself is a minor yellow flag. Even Adani — with vastly superior execution capabilities, Mundra’s infrastructure, and a 500+ person project team — took over a year longer than planned to commission Kutch Copper. First-time operators in complex process industries almost always slip.

3. The Capex Looks Tight

Adani invested approximately $1.2 billion (₹10,000 crore) for Kutch Copper’s 0.5 MTPA smelter alone. Kiri claims ₹12,000-13,000 crore for: 0.5 MT copper smelter + refinery, 1.1 MT fertilizer plant, downstream rod/tube/foil plants, precious metals refinery, and all supporting infrastructure + the investment has an .

Either Kiri is using significantly cheaper technology, or this number will see cost overruns. The copper smelter portion alone, benchmarked against Adani, should be ₹10,000-11,000 crore. That leaves only ₹1,000-3,000 crore for the entire fertilizer plant, downstream facilities, and infrastructure. It feels tight.

4. Trade Policy Risk

This one doesn’t get discussed enough. India currently has a 5% customs duty on copper cathode imports. But zero-duty imports through FTA routes (UAE, ASEAN, Japan) are already entering India and displacing domestic production — the industry body IPCPA has been pushing for a 3% safeguard duty. If FTA loopholes widen rather than narrow, the domestic cathode premium that supports smelter economics could compress significantly. Kiri’s profitability depends partly on government trade policy remaining supportive of domestic smelters — not a bet I’d make with high conviction over a 7-10 year horizon.

The Investment Case: Risk-Reward at ₹2,700 Crore

Let’s be honest about what you’re buying at ₹2,700 crore market cap today.

You’re getting the existing dyes business (maybe worth ₹500-700 crore on standalone earnings), a free option on the copper project execution, and a lottery ticket on Manish Kiri’s ability to deliver a ₹12,000 crore project in a cyclical industry he’s never operated in, financed with 70% debt.

The Bull Case

If by FY31-32, Kiri is running the full complex at ₹2,500-3,250 crore EBITDA and you value it at 6-8x EV/EBITDA (Hindalco copper trades at ~5-6x, a growth-stage Kiri might warrant a slight premium), enterprise value is ₹15,000-26,000 crore. Net of ₹9,000-10,000 crore debt, equity value is ₹5,000-16,000 crore. Call the midpoint ₹8,000-10,000 crore — roughly a 3-4x from today’s mcap over 6-7 years.

The Bear Case

Project gets delayed 2 years, copper cycle turns down, acid prices crash as Indian smelting capacity floods the market, EBITDA at ₹1,200-1,500 crore is barely enough to service debt. Equity value is ₹2,000-3,000 crore — roughly flat or worse after 7 years of capital lock-up. In the extreme bear case (sustained downcycle + execution failure + debt restructuring), the equity can be worth less than the current market cap. This isn’t hypothetical, it’s exactly what happened to Essar Steel, Bhushan Steel, and Videocon when leveraged commodity bets met cyclical troughs.

The Probability-Weighted View

| Scenario | Probability | Equity Value | Return |

|---|---|---|---|

| Project fails or stalls, capital destroyed | 10-15% | ₹800-1,500 Cr | -45% to -70% |

| Project completes, bad cycle, stressed | 20-25% | ₹2,000-4,000 Cr | -25% to +50% |

| Project completes, mediocre cycle | 30-35% | ₹5,000-8,000 Cr | +85% to +200% |

| Project completes, good cycle | 20-25% | ₹10,000-15,000 Cr | +270% to +450% |

| Everything goes right, bull cycle | 5-10% | ₹18,000-25,000 Cr | +570% to +825% |

Expected value: roughly ₹5,500-7,000 crore, or about 2-2.5x from current price over 7 years. That’s a ~12-15% CAGR — decent but not spectacular for the risk profile.

The Milestone-Based Approach

If I were allocating capital here, I wouldn’t take a full position today. The asymmetry improves dramatically as execution milestones are hit. Here’s the framework:

Milestone 1: Financial closure confirmed (Target: March-April 2026). This is the first hard proof point. If it slips, it tells you the project is already behind schedule before construction starts. A small tracking position (1-2% of portfolio) before this milestone is reasonable for anyone who wants optionality.

Milestone 2: Downstream rod/tube plant commissioning (Target: April 2027). This proves basic execution capability. The downstream plants are simpler to build and operate, but successfully commissioning them demonstrates the management team can deliver on timelines. Revenue will flow but EBITDA will be thin (fabrication margins only). If this happens on time, add to the position.

Milestone 3: Smelter equipment delivery and construction progress (CY2027-2028). Any meaningful delay here pushes the integrated economics by 12-18 months.

Milestone 4: First cathode production (Target: Late CY2028). The real value creation moment. This is when Kiri switches from being a rod/tube fabricator buying cathodes to an integrated smelter selling its own refined copper with by-product economics. If this happens within 6 months of guidance, the stock likely re-rates significantly.

In my opinion, stock won’t go from ₹2,700 crore to ₹15,000 crore overnight. There will be a multi-year ramp-up during which you can average in with progressively better visibility on execution. The market will give you opportunities: cyclical fears, delay announcements, interest rate concerns will all create entry points.

Closing Thoughts

The macro thesis behind Kiri’s copper pivot is real. India’s copper demand-supply gap is large and growing. Import substitution is a genuine opportunity. The integrated smelter-fertilizer model is clever. Copper demand at 3.2 million tonnes by FY2030 against ~1.3-1.5 MT of domestic capacity leaves room for new entrants.

But there’s a wide gap between “the thesis makes sense” and “this management team can execute it at these margins with this leverage.” Kiri’s EBITDA guidance of ₹4,500-5,000 crore is roughly 1.5-2x what industry benchmarks support. The capex looks tight against Adani’s comparable spend. The TC/RC environment is the worst in smelting history. The promoter has no relevant experience. And the entire equity is levered to a single project outcome with no parent entity backstop.

Position sizing matters more than timing on this one. Treat it as a levered call option on Indian copper demand, and size it accordingly.

Disclosure: I don’t currently hold a position in Kiri Industries. This is not investment advice — it’s an attempt to understand a complex industrial project using publicly available data. I may be wrong on several assumptions. I’d love to hear from anyone who understands smelter economics better than I do, particularly on the TC/RC outlook and sulfuric acid price dynamics. Happy to be corrected.