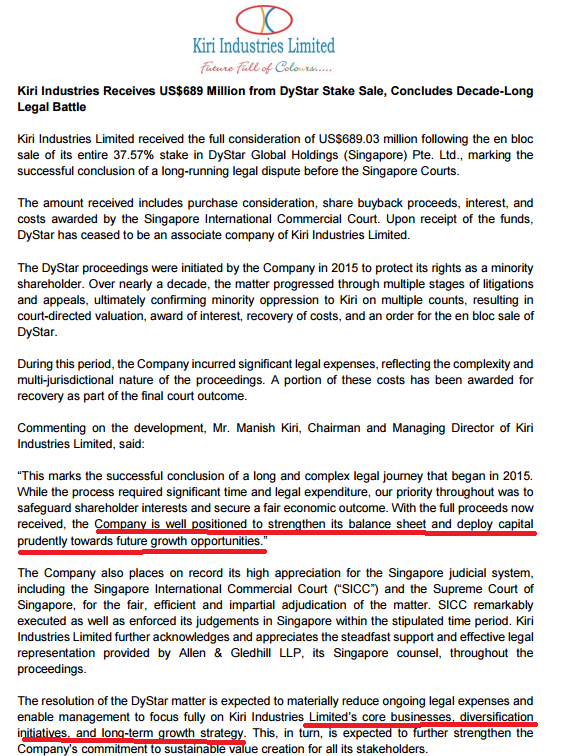

Latest press release from Kiri uploaded after market hours. It doesn’t even mention “rewarding shareholders” anywhere. It’s ironic that the case was fought to protect rights of minority shareholders. It seems, more than 90%+ fund to be deployed in new growth areas doesn’t necessarily mean dividend to account for ~10% proceeds. It may be much lower.

Seems like the market is pricing in the scenario that there is going to be minimal or no special dividend and immediate return from Dystar stake sale. And if that actually happens then there is going to be a prolonged period of sideways movement with substantial downside risk due to uncertainties involved regarding timeline and management’s execution capability for copper and fertiliser projects. It would be good to know what is the consensus here for holding the stock - is it long term return or expectation of immediate special dividend for minority shareholders.

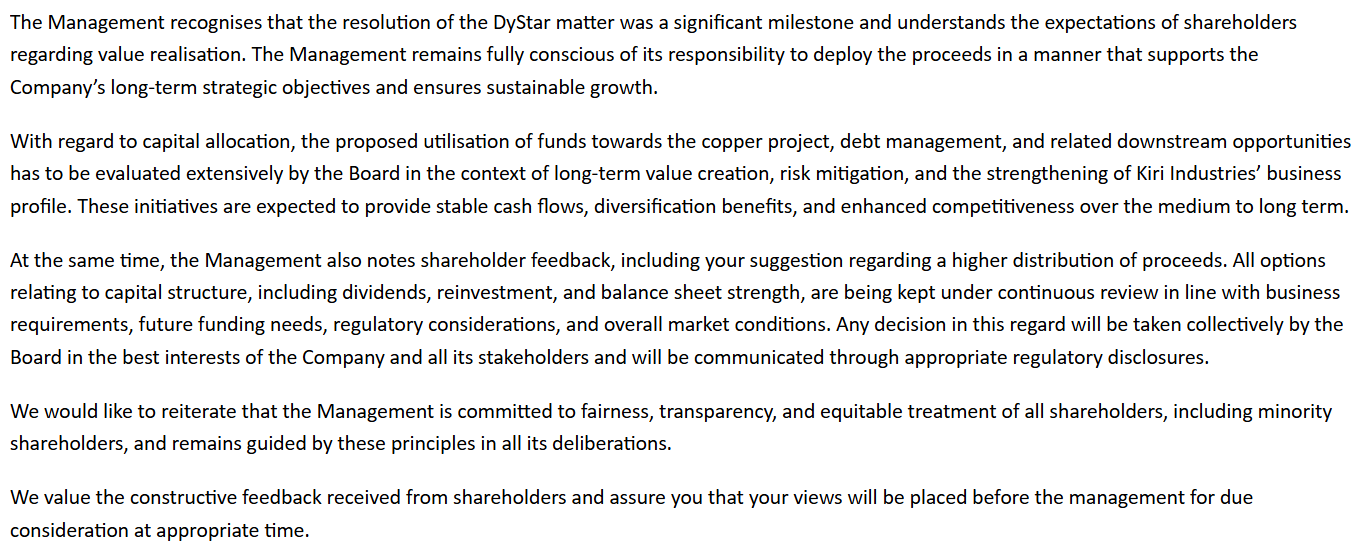

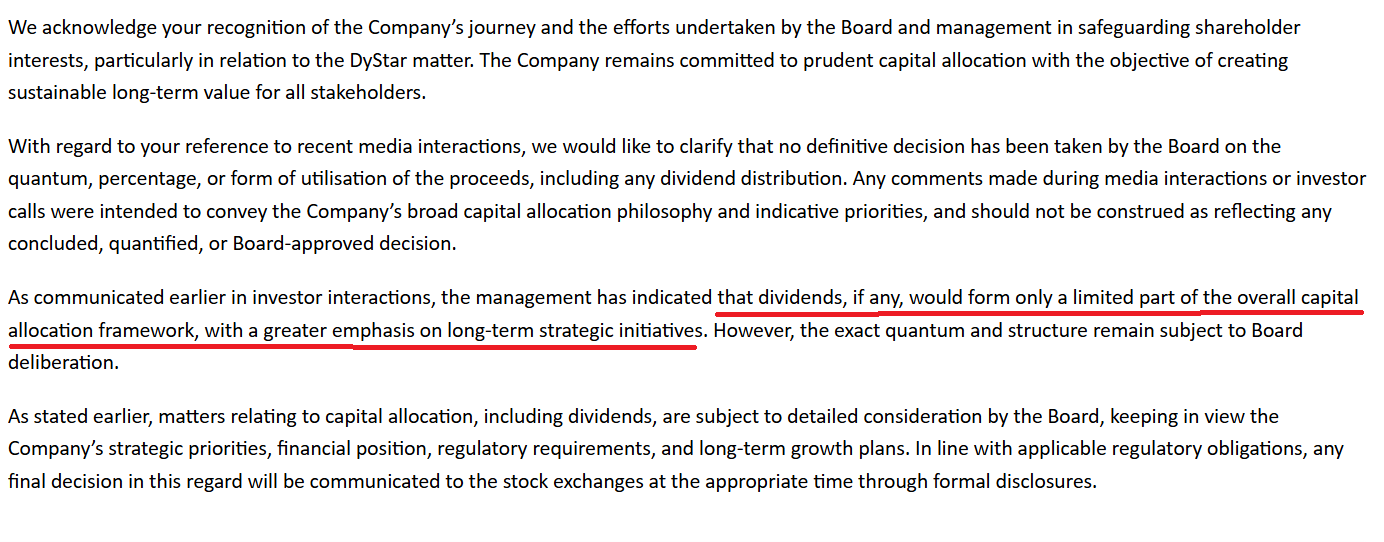

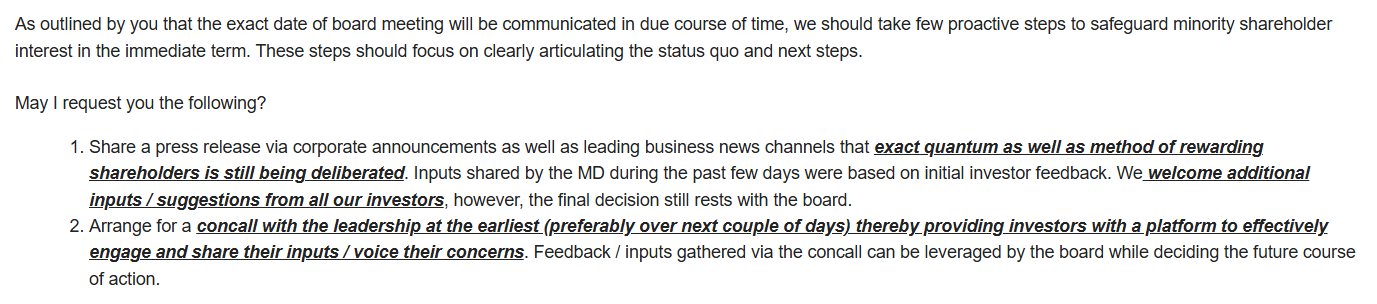

Got the below response from Kiri’s end post sharing my concerns regarding dividend payout.

So, those reaching out may follow above instructions for quick revert. Best Wishes.

3 Likes

Very good initiative. Let us all inundate Kiri managements with messages with required details.

Rather than demanding a large one-time dividend, shareholders should push management to prioritize accelerated copper project execution. With full utilization revenue potential of ₹40-45k crores, Phase 1 capex of ₹2,500-3,000 crores should deliver ₹8-10k crore revenue by FY28 (20-25% capacity), scaling to ₹40-45k crores by calendar year 2029 —representing 50x growth from current ₹800 crore revenue base. Management’s disclosed discussions with Tata Consulting Engineers and the experienced new copper board provide execution credibility. Structure the project for commercial production start by Q1 FY28 within the 36-month target. ₹8-10k crore revenue stream creates permanent multibagger value vs temporary dividend payout.

3 Likes

I honestly don’t see how paying dividend right now is better than lowering debt equity ratio by the same amount. Focus should be on 1. Financial closure of copper project 2. Good treasury management of funds 3. Speedy execution on copper project with detailed update with results

2 Likes

Hmm…looks like the stock needs a new set of investors. Here’s my hypothesis. There are two broad sets of investors.

Investor set 1

The stock currently has a large representation of investors who were waiting for the DyStar payout to come in. Many of them have been waiting for years, amidst all the uncertainty. Now that the DyStar money has finally come in, they are looking for a meaningful reward for their patience. If they are told they have to wait ANOTHER five years for the copper business to be established and settled, they do not think it fair. Such investors have been showing their displeasure by exiting, leading to the unfortunate situation (for both the investors and the company) of the company trading at a value less than the cash proceeds received from DyStar. I hope Manish Kiri realizes this and revises his stance, and provides a more meaningful immediate reward for this set of investors who have been through a long and painful journey along with Kiri.

Investor set 2

On the other hand, there seems to be emerging another set of investors who see a management that is smart (took a bold and calculated risk on Dystar and bought it at an attractive value, which proved to be a great call) as well as resilient (was able to stand against a much larger Longsheng in a protracted legal battle and emerge victorious). They see INR 5k+ cr cash in the hands of such management. They see a key hurdle of regulatory approvals already cleared for the copper business. They read about rising copper prices every day. They believe that the management could create much more value out of this 5k cr, and believe this is a great time to enter this ship.

There may be some overlap between investor sets 1 and 2, but it does not seem to be a large overlap - these are mostly distinct. The stock price is likely to experience some pain as the investor base transitions from largely set 1 to largely set 2. Set 2 will have to balance governance concerns with the promising outlook they project for the future.

While the transition from investor set 1 to set 2 occurs, I hope the Kiri management and board rethink the initial plan on using the DyStar proceeds, and provide a more meaningful reward to the patient set 1 investors, who have been with the company through a long and painful phase.

7 Likes

Seems Investor set 2 and the Kiri management are aligned in their thought process. Lets see when this set starts overpowering the set 1 and arrest the fall in price.

in 5 years, copper will be in another zone, cash will be gone, and new set of investors will also wait for copper cycle to get rewarded…and the cycle will continue…

it would have been best for kiri to give a sizeable amount to shareholders, while work on copper plant with leverage.

9 Likes

There is a third set of investors that would rather wait for a couple of years and not lock their money ahead of times. Cycles are shorter. Cash may evaporate. The pile of debt may increase before phase-1 sees the light of the day. Core business may struggle more than it currently is.

With these many unknowns in a new business territory, wait-and-watch seems like a decent alternative. There is a saying in my village that goes like this. A cloth merchant opening a restaurant takes time to learn that while cloth can sit on a shelf for a year, a plate of food dies in a few hours. Not saying it would happen, but why risk.

Disc: I got in and out a couple of times from Kiri. Currently no holdings. Willing to change my opinion in 30 months from now.

1 Like

Kiri Industries: Why the Market Is Voting Against the Current Capital Allocation Plan

(A Shareholder Perspective)

![]() The Core Paradox - ₹6,200 crore cash received from DyStar - Current market capitalisation ~₹3,500

The Core Paradox - ₹6,200 crore cash received from DyStar - Current market capitalisation ~₹3,500

crore - Stock price has fallen after cash realisation

This is not a market mistake. It is a clear vote of no confidence in capital allocation.

![]() What the Market Is Saying (Implicitly) “We do not trust that the cash belongs to shareholders.”

What the Market Is Saying (Implicitly) “We do not trust that the cash belongs to shareholders.”

Reasons for market discount: - ~90% of DyStar proceeds proposed to be locked into long-gestation

capex - Minority shareholders receive only a small fraction upfront - Returns from new projects are

uncertain, execution-heavy, and far in the future

Cash has value only when shareholders believe they will receive it.

![]() Indo Asia Copper Project – The Real Numbers Total project cost: ₹8,000 crore (conservative) Spent so

Indo Asia Copper Project – The Real Numbers Total project cost: ₹8,000 crore (conservative) Spent so

far: ~₹700–900 crore (land, EC, engineering, early works) Remaining capex required: ~₹7,200 crore

Funding already arranged: US$130m (~₹1,100 crore) via Claronex (largely allocated, partly spent)

The project is still at an early phase.

![]() Key Point the Market Understands (but Management Ignores) Kiri does NOT need to withhold

Key Point the Market Understands (but Management Ignores) Kiri does NOT need to withhold

shareholder returns to fund the copper project.

Realistic funding mix: - Equity from DyStar proceeds: 3,000–3,500 cr - Project / term debt: 2,500–3,000 cr

- Internal accruals & others: 700–1,000 cr - Special dividend to shareholders: 2,500–3,000 cr - Total: Fully

funded

Why the Current Plan Is Being Punished Markets penalise companies when: - Excess cash is

Why the Current Plan Is Being Punished Markets penalise companies when: - Excess cash is

reinvested without a return framework - ROCE visibility is low - Minority shareholders have no assurance

of future payouts

This is why cash > market cap and stock continues to fall.

A ₹3,000 Crore Special Dividend Is Not “Anti-Growth” It would: - Return litigation gains to

A ₹3,000 Crore Special Dividend Is Not “Anti-Growth” It would: - Return litigation gains to

shareholders - Enforce capital discipline - Reduce overinvestment and ROCE dilution - Restore trust and

credibility - Narrow the valuation discount immediately

Most importantly: It proves the cash belongs to shareholders.

1

Governance Issue, Not Sentiment Kiri successfully fought minority oppression at DyStar. Minority

Governance Issue, Not Sentiment Kiri successfully fought minority oppression at DyStar. Minority

shareholders now ask for: - The same fairness - Respect for capital - Alignment of interests

The Ask (Simple and Reasonable) - Declare a special dividend of at least ₹3,000 crore - Cap equity

The Ask (Simple and Reasonable) - Declare a special dividend of at least ₹3,000 crore - Cap equity

contribution to the copper project - Fund the rest through structured project debt - Publish a capital

allocation framework

Final Thought The market is not against growth. It is against growth at the cost of shareholders. A

Final Thought The market is not against growth. It is against growth at the cost of shareholders. A

balanced approach will: - Re-rate the stock - Attract long-term capital - Strengthen management

credibility - Create sustainable value for all stakeholders

One letter can be ignored. Hundreds cannot.

2

2 Likes

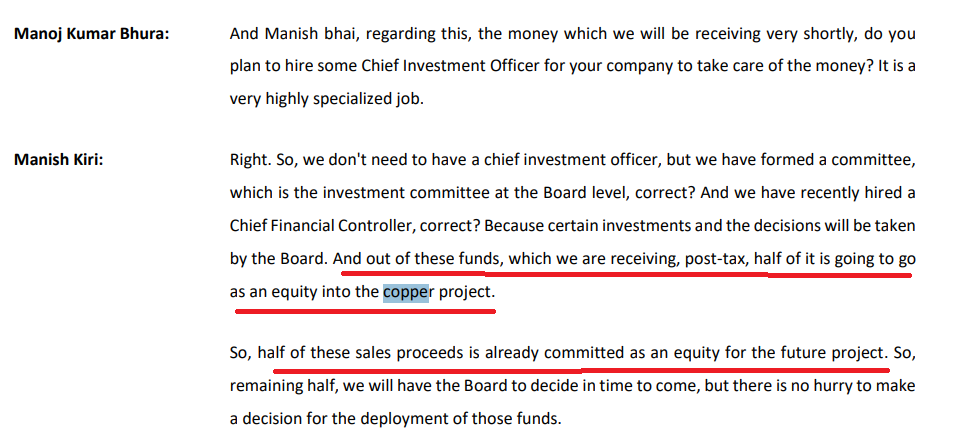

Management has been setting expectations vis-a-vis sharing the reward with the shareholders:

- Pre receipt of Dystar proceeds - “~50% of the proceeds will be used as equity contribution towards Copper project”

- Post receipt of Jan 1 '26 - More than 90% will be for new investments i.e. <10% will be for rewarding shareholders (CNBC)

- 2nd Jan on NDTV - A very small sum will be for dividend (comment that literally broke the camel’s back in terms of correction in price)

- 2nd Jan press release post market hours - no mention of rewarding shareholders

- In the latest response received, they even mentioned - dividend, if any

I may be reading too much into some of the recent communication but it seems management has made up its mind and is further reinforcing it in subsequent communication.

The gritty and battle-hardened promoter that Manish Kiri is, I doubt if there will be any change in stance so one should brace up of miniscule dividend.

Btw, I too, was of the opinion that a meaningful dividend - ~1000 Crs would have been announced keeping in view the pain that the investors have gone through over the past decade. That would have still left enough in the kitty for future capex requirements. Even fertilizer is a downstream project, which given the Copper projections, could have been easily funded via accruals and some debt.

Investors may go through two contrasting examples of Aster DM and Hinduja Global to understand the difference as to how shareholder wealth is created or destroyed and minority interests are upheld or otherwise.

Screenshot of the earlier concall where commitment was for 50% of post tax proceeds towards the Copper project.

1 Like

I have posted this query to IR at KIRI, will update answer when i Get reply.

I have following queries/suggestions:

-

Giving dividend while taking debt seems unnecessary. A buyback will be much .better as people who want payout can tender shares and those who do not will not tender shares. It can help promoters increase stake as well as set a floor price for the share which has gone into a tailspin

-

Loans given to related parties Chemhub Tradelink Pvt. Ltd., Kiri Infrastructure Pvt. Ltd., Metallonia Metals Pvt. Ltd. are a red flag which many investors have shared concern over and should be cleared as soon as possible

-

A con-call to reiterate status and copper plant project would be great including proposed capital structure

-

If any further investment planned other than copper project, please try to see the gestation period is less

-

Pls consider getting equity partner in IACL which will lend it credibility as well as set benchmark for subsidiary valuation

-

Please expedite board meeting for deciding and disclosing capital allocation plans

2 Likes

Had sent an email yesterday seeking following actions immediately but haven’t received any response yet. Will update if there is any meaningful response.

The management is useless, they have clearly stated in an interview that a very small portion of received capital will be given to the shareholders as dividends and rest will be “reinvested” in the business.

It’s really sad to see that there is no activist Investing in India.

In my honest opinion the company should be taken over, liquidated and all the cash should be redistributed to shareholders. The mgmt is really bad at capital allocation and hence is just destroying wealth for shareholders!

Very Greedy Management!

1 Like

I have been tracking this company since past few years. I will keep the story broad.

The guidance given by company managements seem unreasonable. They claim they will have a PAT of Rs3500 odd cr in 5 years on investment of Rs6-8k cr. However, company is new to this copper business. The company has gotten funds now but many companies already have lot of money to fund such capex. In my view, promoters havent made any money since 2010. Now , doing a lot of capex which will benefit promoter than minorities. Or it could be a experiment for the promoter which could take many years to fructify( learning takes years). For me a complete EXIT is warranted.

Disc: Sold the stock few months back

Let us stop this bickering. As we are discussing the matter, I am sure that it is not going to influence Manish Kiri. I was sure long before about this. Manish Kiri wants the whole pudding. Why nobody questioned loans ganted to related parties? Earlier also he assured distribution to shareholders but was intentionally ambivalent regarding amount. Certainly he was not alluding to 10/15 per share. Because this is routinely dished out by most companies and they don’t brag about it.

Why not raise it in Board meeting? Manish Kiri does not have majority holding. So if majority shareholders decide, we can force management to change. Is it not some kind of oppression of minority shareholders interest, like the case Kiri fought legally?

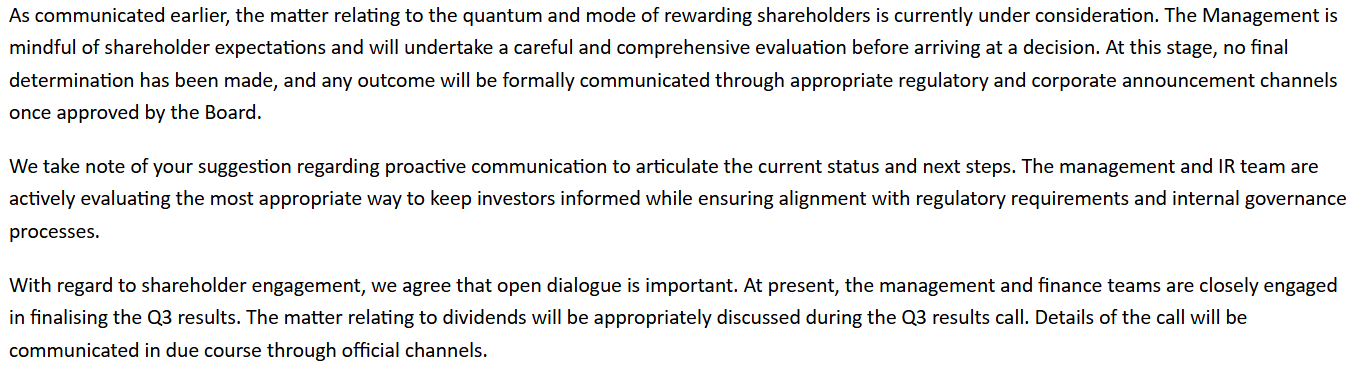

Response received ;

Thank you for sharing your detailed suggestions and perspectives.

We appreciate the time taken to articulate these points and your continued engagement as a shareholder.

We would like to clarify that no final decisions have been taken regarding capital allocation, including dividends, buyback, investments, or funding structures. All such matters including utilisation of proceeds, capital structure, related-party transactions, and future investments—are under active review and will be subject to detailed evaluation and approval by the Board of Directors.

Your inputs regarding shareholder rewards, clarity on related-party exposures, project gestation timelines, potential strategic partnerships, and the need for enhanced communication through a concall have been duly noted. These suggestions will be placed before the management and the Board for consideration as part of the ongoing deliberations.

The Company remains committed to prudent capital deployment, transparent communication, strong governance practices, and long-term value creation for all shareholders. Further updates will be shared through official and regulatory channels once decisions are finalised.

Thank you once again for your valuable feedback and support.