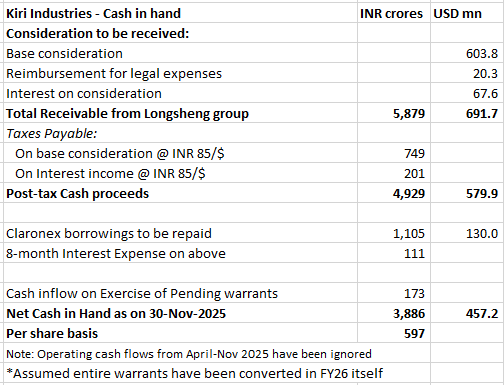

Please modify sheet and upload here for all of us to use. Thanks. Also tax needs to include surcharge and cess

There is no further surcharge and cess, tax rate was mentioned by the promoter in the conference call. Rest is a basic calculation, you can ask any LLM do using company’s latest annual report.

Also, I believe the suspicions of promoter siphoning money are overstated in this thread. If the promoter wanted to siphon money, they would not have infused their own capital through warrants and increased their stake. Which, by the way, they did so after being asked multiple times by the investors themselves in the earnings calls.

If they siphon of the money, they themselves tend to lose out the most as primary shareholders. Of course, this is depending on the fact that they don’t start reducing their stake which would be a red flag (see Gensol).

Their mistake is poor capital allocation decisions which is not unexpected when venturing into a completely new sector relying on a CEO who turned out to be unreliable. This remains a major risk which is why the share price doesn’t reflect the book value.

But they corrected their course and have committed to giving updates about the copper factory from the next earnings presentation. This would be a green flag in terms on transparency if this happens.

As posted above, company has given a detailed explanation regarding the firing of the CEO which is good in terms on transparency.

Raising funds at 15% is again a big issue, not sure if they couldn’t have raised debt at a lower cost in India. Again a poor capital allocation decision in hindsight. Not if they were expecting 25% IRR as they had projected.

Another issue is the company has been evasive about using the rest of 50% cash. Don’t think they are planning to pay dividend at this stage.

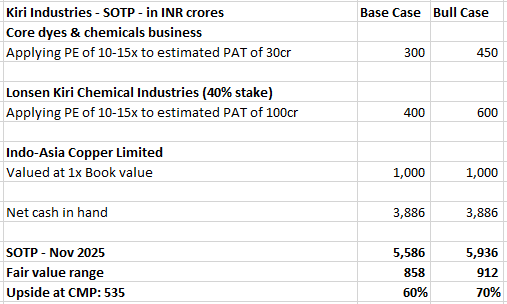

The stock is still relatively cheap so happy to hold even with all this uncertainty.

1 Like

Some other concerns:

The new CEO of Indo Asia Copper was the COO of Paradeep phosphate from 2018 to 2021, a company that has performed phenomenally before and after his tenure.

There is no information on his linkedin on what he was doing between 2021 and 2025.

Another concern is that we don’t have visibility on the copper plant. There are no images, Google Earth can be 3+ years old in remote areas, gate images on ex-CEOs LinkedIn are 3D renders.

Let’s wait for next concall and if there’s no further update, time to take a call

2 Likes

Google Earth imagery of the copper plant site is dated 9th March 2025. Go to hostorical imagery and scroll to the last on the side bar.. you will get the date of the latest imagery.

2 Likes

Share the link or co ordinates or image

Please go through the environemental clearance given to IndoAsia Copper.. It is in their website…you will be able to find out yourself the co-ordinates and also the proximity of its neighbouring mfg plant/ villages/ temple/pond/ports etc.. further in the EC committee minutes in the Gujarat governent website you will find the co-ordinates of the effluent treatment plant and also the naksha of the copper plant boundary.. Its interesting to find it yourself and I dont have to convince anyone that this is the exact place where the plant is proposed to be erected and is a completely barren 160-170 hectares of land in the march google earth images except for a portion of some boundary wall being erected… with mgmt saying that site work hasnt started yet in this concall and enquiry etc for machinery/technology is undergoing i doubt anything much has changed on the site…

Google Earth.pdf (2.0 MB)

1 Like

They raised 1000 plus crores in 2022-23 via loans and warrents to get EC and to put a boundary wall on land already purchased??

What a masterstroke

No Shrinivas the judgment finance would be bearing 12 months now… the EC would be a few months before that.. its not that delayed but the drama with Dr Sarkar, the allegations, the misuse of funds and position and decision making deviations points to a creation of a blame game where someone maybe made a scapegoat for failure to execute… obtaining an EC for a copper and fertilizer plant is no small feat.. but in the grand scheme of things of 6000+ crores the expense will be a drop in the ocean..

They are too close to Adani Copper plant to be able to grow and thrive.. and that kutch copper is only half done as on date.. definitely there will be positivity when Longshen ponys up the dystar sale proceeds but the large scale investment proposed by the promoter means shareholders have to wait a good 3 years from now to see the fruiction of those plans and the start of which reeks of poor or mismanagement

1 Like

Collecting more information on the new CEO:

- 66 year old which means he probably retired in 2021 and then came back. Not great.

- NIT Warangal BTech in Chem + previous experience with Hindalco

Buyer Longsheng Announcement on providing guarantees for holding subsidiaries. Attached is translated version of doc posted today 20AUG to Shanghai stock exchange

600352_20250820_FDDU (1).pdf (615.7 KB)

1 Like

@Swaroop_NS I am unable to understand the significance of the shared guarantee document in this context. Could you please elaborate something on it to help me understand?

Lonsheng is raising loans to pay kiri

I think it is a routine announcement, nothing specific to deal

Why will they routinely raise 1 billion dollars?

Where is it given they raising. This is just statement of current guarantees provided.

Zhejiang DyStar → Got credit with Zheshang Bank up to RMB 800m.

Zhejiang Hongsheng → Financing up to RMB 440m.

Zhejiang Annuo → Financing up to RMB 150m.

Subsidiaries are borrowing 1 billion guaranteed by lonsen

Suddenly why so much loans they require?

1 Like

It could be old credit lines. Where does it say when given. Any minor issue

Longsheng posted a bunch of documents on Shanghai SE. The semi annual report notes no further progress on litigation other than to say it is with Chinese Ministry.

Major litigation and arbitration matters:

Litigation or arbitration matters have been disclosed in the interim announcement and there has been no subsequent progress.

On May 29, 2025, the Company held the 19th meeting of the Ninth Board of Directors, which reviewed and approved the “Proposal on the Purchase of 37.57% of the Shares in DyStar Global Holdings (Singapore) Pte. Ltd.” The Company, or its subsidiary, Anno Chemical (Hong Kong) Co., Ltd. and/or other wholly-owned subsidiaries, will be the

transferee upon closing to purchase 37.57% of the issued share capital of DyStar Global Holdings (Singapore) Pte. Ltd. held by KIRI. The closing consideration is US$696,547,800 plus any adjustments (if any) made on or after the closing date. To date, the Company has applied for filing and registration of the acquisition with the National Development and Reform Commission and the Ministry of Commerce.

3 Likes

4 weeks left as of Oct, the deadline date, look like no body is interested to buy Kiri stock. Institutional interest is nowhere in it even HNIs are not interested to buy at current level. Whats going on

?

1 Like