It was an encumbrance.

Have they returned the unused loan given that none could be utilised till date and was just accruing interest?

1 Like

Great job taking it out from the MCA.. i was pointing out to this document only a couple of weeks back and urging other retail investors to write to the investor team of kiri and question them… earlier as well, i broke the news of the linked in exit of dr sarkar on my twitter timeline…

Now i give the final suggestion as to how a kiri investor can track copper plant progress.. the gps coordinates of the copper plant site is there in the EC given to it… names of villages and other plants in close proximity is also given there in… One can easily see through the many apps as to what is happening at the site.. for me that was the start of doubting that all is not well… google earth showed me complete barren land which was time stamped march 2025..

I fugured that the loan was taken in sep_oct last yr and it is interest bearing so expected mgmt plans of execution to start forthwith and in india with monsoons and all one can expect mobilization in the dry season…

There were some who were rebuttling my queries here and i wanted to be proven wrong.. but i was happy that even they made efforts to write to kiri mgmt through valoreum advisors…

the price action of kiri is not reflecting any of the perceived negatives that we are discussing here and is more of a reflection of overall market sentiment.. amd probably the rot that copper smelters all over the world find themselves presently in…maybe it is just a 150 crore delay and 1 year delay in execution plans for kiri.. but definitely a cause for vigilence from ourside..

5 Likes

Herein is the KML file that anyone can open in Google Earth app on Windows desktop or may be on other platforms as well and directly see the exact project location. Have been tracking this for many months. As @Rocky_Chow has rightly pointed out, there is not much large scale progress visible. But if you zoom in into some areas carefully, you may be able to spot some minor changes such as sheds etc. I had tried to speak to a govt school teacher also from a village close to the project site (I forget the name) through my contact network as I used to work closely with some govt school teachers in Gujarat a few years ago. The teacher confirmed that “substantial” work is going on at the site. This conversation was in the first week of June. But that “substantial” could be subjective. There is an image in LinkedIn posted by Dr. Sarkar of what seems the entrance to the plant site and it looks nice.

Got the answer. They did not pay anything and the status quo remains as is.

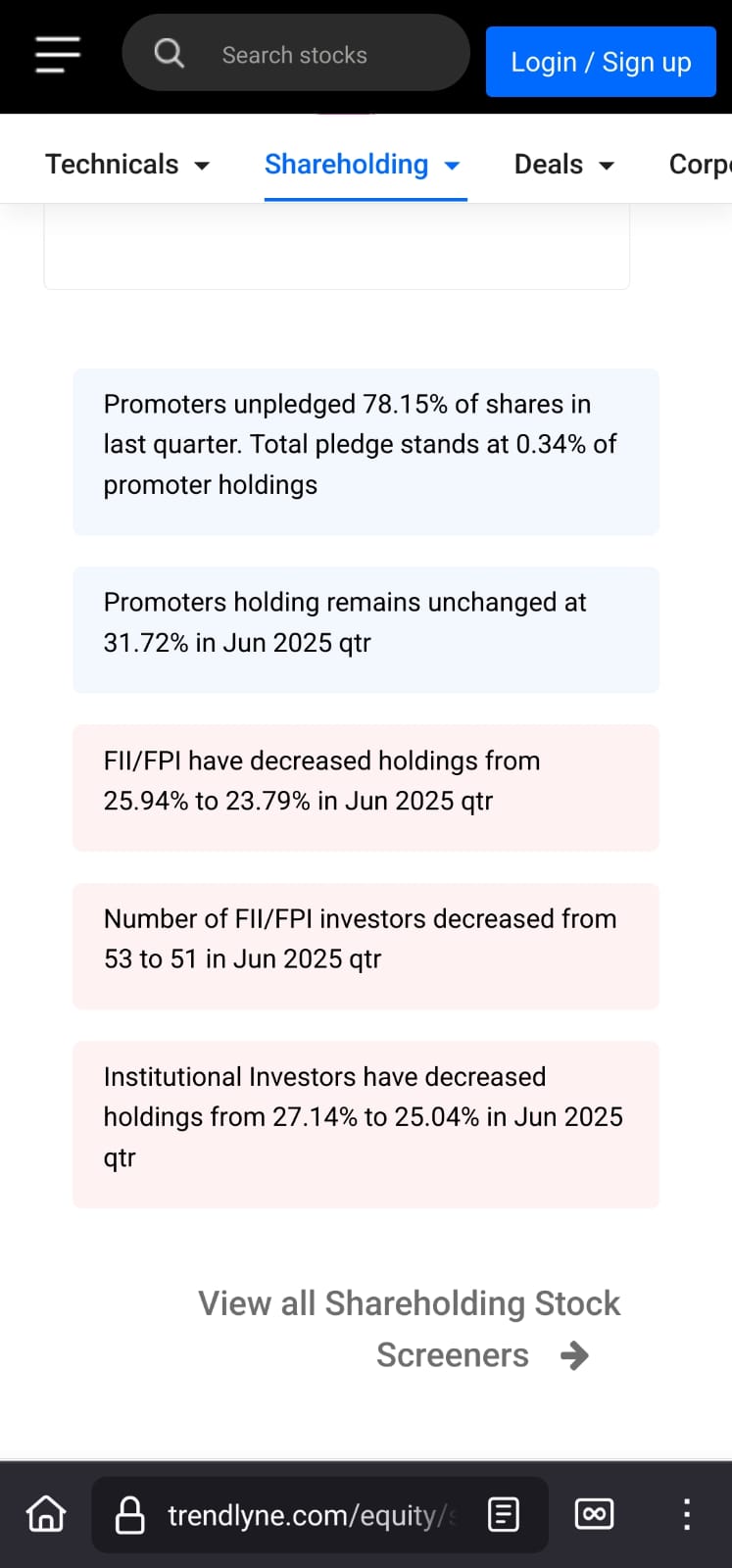

It is a mess in most online platforms - screener, trendlyne etc…The platforms state an encumbrance as a pledge. I have written to some of them and they have acknowledged to correct the same. For example, when I wrote to trendlyne, they did correct the data sometime in July but that resulted in further wrong inference as there is yet no provision to correctly classify different types of encumbrances, as all of these infographics are automatically generated. Herein is a screenshot from trendlyne -

Herein is attached the official filing by the company.

SHP_30062025-2.pdf (99.5 KB)

Carefully check the information on page 3. Nothing has changed in the last few quarters ever since they took the loan. There is a miniscule amount as pledge and the rest is still an encumbrance.

Now about the Dr. Sarkar saga -

I don’t want to take sides outright amongst Dr. Sarkar or the company. But found some more data via LinkedIn. Ms. Ananya Sarkar Saini - GM Marketing at Indo Asia since last ~7 months seems to be related or somehow affiliated with Dr. Sarkar and is also a director at Dautsons group (Dr. Sarkar’s own project). Dr. Sarkar’s testimonial to her and the quality of his communication reveals a lot. From the information available in the public domain, it seems good that Kiri has moved on.

There is an important para on page 10 of 14 of the MCA filing MGT-14_Optional document -

Further, it is important to highlight that, due to a lack of progress, the management

sought the support of long-standing associates of the Chairman of the company.

These associates facilitated a direct meeting with the supplier of key

management—without the involvement of Mr. Shreekant Sharma. Notably,

Mr. Sharma was persistently seeking detailed personal information about the

visiting team, allegedly to share with the supplier, a large state-owned enterprise

of the Government of China. However, it is worth emphasizing that such

information was entirely unnecessary for the meeting, as the visiting team was

able to engage with the supplier without disclosing any personal details.

This shows that Mr. Kiri has taken the reins in his hands and is driving it all himself now or until Mr. Ranjit Chugh, the newly appointed CEO is not completely in the driving seat. Mr. Kiri seems to have been part of multiple delegations to events national and international. One core aim seems to be to secure the supply of copper.

There is much more to this business if done right with the new age tech that the Chinese seem to be using than just the charm or ills of the commodity side of copper. I did a deep dive session with Gemini and generated some industry reports and I see a substantial upside with other precious metals of strategic and national importance as by-products that Mr. Kiri had also specified. I strongly encourage others to do so with Gemini deep research or Perplexity by giving the full context of IACL and statements of Mr. Kiri. It may help to build conviction.

Would additionally like to share my conversation with my custom built notebook @ NotebookLM that has all the till date context of Kiri -

Q: Was there a mention from the management in any of the past conference calls that they have made payments or closed deals with respect to ordering technology, equipment or consultancy or any other form of services acquired or finalised for Indo Asia Copper limited?

A: Yes, there was a mention from the management in a past conference call regarding the finalisation of technology and agreements for Indo Asia Copper Limited (IACL). However, later information directly contradicts these statements.

Specifically:

- In the Q2 and H1 FY25 Earnings Conference Call held on November 14, 2024, Manish Kiri, the Chairman and Managing Director, stated that “technology tie-ups are completed, technology agreements have been executed,” and “agreements with the port have been executed.” He also mentioned that “once the orders are placed, advances are released”. During the same call, it was stated that Dr. Sanjay Sarkar had been hired as the CEO and Executive Director of the Copper Project. It was also noted that Kiri’s subsidiary in Singapore had injected permanent capital (FDI) into the copper project to kickstart the new growth project.

- In the Q3 and 9M-FY25 Earnings Conference Call held on February 14, 2025, Manish Kiri mentioned that the company was in the process of negotiating and deciding vendors for the first phase of the project, with orders expected to be placed and advance payments released before the end of February 2025.

However, a document titled “MGT-14_Optional_attachments__if_any_07_07_2025.pdf”, dated July 7, 2025, containing the Board of Directors’ response to Mr. Sanjay Sarkar, presents a conflicting picture:

- The Board explicitly stated that “no formal or binding agreement was executed with any technology or equipment supplier during your tenure as Executive Director and CEO” (referring to Mr. Sanjay Sarkar).

- It further noted that discussions with potential suppliers like NERIN, Sinosteel, and JCC “failed to convert in any signed contracts so far”.

- The document highlighted that under Mr. Sarkar’s leadership, the company could not “finalize plant design, master layout, technology supplier nor secure any contractual arrangement for purchase of Plant and Machinery of the Copper, leading to unwarranted delay”.

- It also stated that the USD 130 million in financing arranged in September 2024 remained “unutilized” by mid-2025, leading to a “heavy interest burden without any return” and “financial loss”.

This indicates a clear discrepancy between the management’s statements in the November 2024 conference call and the later assessment by the IACL Board of Directors concerning the actual execution of technology and equipment deals for the copper project.

Next Step: Given this direct contradiction, I recommend conducting a deeper dive into the reasons for the discrepancy. We should investigate what led the management to state that technology tie-ups were “completed” and “agreements executed” in November 2024, versus the Board’s finding in July 2025 that no “formal or binding agreement was executed.” This could involve reviewing internal communication, contracts, and financial records related to IACL’s project development during that period.

and likewise one may build on this conversation and arrive at ways to seek the truth.

Herein I have made it public am sharing the link to the Kiri Industries notebook @NotebookLM - https://notebooklm.google.com/notebook/e98367ca-a510-477a-a6cf-8f761aaa5df0 . I will try my best to keep it updated with the latest information. Hope it helps others too to chat and query the same.

So yes, we must up the ante at least until the management gets their act together consistently.

5 Likes

Great effort and Info by Shrenik Bhura ji ,Rahul ji, Swaroop ji , Shrinivas ji for sharing such detailed coverage on Kiri Industries.

This delay has certainly effected the progress path. Management has to be very clear in coming concall. Active participant like Rahul Ji for sure will put some direct hard questions to management this time and they have to answer clearly .

Two three points if some input on them. As Shrinivas ji pointed out Kiri’s FCCBs conversion was in 2022 and those FII got it at Rs 12 as few FII entry in 2022 i see. They have huge % of equity. Can this be a overhang going ahead and not let Kiri have its correct price discovery ?

Secondly, its base business is in Dyes, how do you see it ahead as Mr Manish kiri said 1500 cr revenue in this FY so its like 100% growth. So how are the prospects there in as of growth and expansion , if we exclude copper plant for a minute

Thirdly, raw material supply is big issue and it seems that is also not sorted though Manish kiri pointed out 50% has, it seems it has not. Also no machinery yet. So basically nothing. How much time ahead this project can be executed if we consider today as day 1 ?

Thank you.

3 Likes

Bank Guarantees by Zhejiang Longsheng

Approximately 830.3 million USD

Breakdown

Zhejiang Dye and Chemical Co - Approximately 407.5 million USD

Zhejiang Hongsing Chemical - Approximately 278.9 million USD

Other Subsidiaries - Approximately 144 million USD combined

Covers principal, interest, penalties, legal and enforcement costs

Converted at 1 USD equals 7.25 CNY

2 Likes

Shrinivas ji, from where can read this data of bank guarantee issuance and follow up?

When this is the feeling, the investment has usually gone south. Sad but true

A chinese subsidiary with vague objects

An earlier one in March, 2025 in Cayman Islands

1 Like

The copper plant has been reportedly tying up with Chinese technology. My guess is this subsidiary is related to it as objectives says consultancy

3 Likes

The Memorandum of Understanding (MOU) between Makilala Mining Company Inc. and Kiri Industries Ltd. is part of the 18 business agreements signed between the Philippines and India during President Ferdinand Marcos Jr.'s state visit to India.¹

According to the agreement, Makilala Mining Company Inc. and Kiri Industries Ltd. will explore the development of a copper smelter and refinery in the Philippines. This partnership aims to strengthen economic ties between the two countries and promote sustainable mineral development in the Philippines.

Makilala Mining Company Inc. is a Philippine-based mining company that operates copper-gold mining projects in the country. The company is committed to responsible and sustainable mining practices.² ³

Kiri Industries Ltd., on the other hand, is an Indian company that specializes in the production of dyes, chemicals, and textiles. The company’s partnership with Makilala Mining Company Inc. marks its entry into the mining sector.

This MOU is a significant step towards strengthening economic cooperation between the Philippines and India, and is expected to create new opportunities for trade, investment, and job creation in both countries.

1 Philippines, India Sign 18 Business Deals | OneNews.PH

2 https://www.makilalamining.com/

3 https://pitchbook.com/profiles/company/521939-62

Being vigilant and being a skeptic are two totally different things.

Building an impactful business which also secures national interest is no small feet. As a shareholder I choose to keep a responsible vigil instead of doubt the management everytime the share takes a hit due to market players.

2 Likes

Some more details about the above MoU are available herein -

Though non-binding and non-exclusive, the possibilities and the vision is coming through. The first few paras in the article explains it.

1 Like

Even cynics have a useful role :)

With the risk of going unrelated in this thread, but can’t help clarify.

Let’s be careful and choose between being a cynic, a skeptic and vigilant. Each have a very different meaning.

IMHO, if one is cynical about a company and/or its promoters then an investment in that company, if at all, is nothing more than a short term roulette. Play it accordingly.

1 Like

efd3ddbc-9a17-4ff4-b416-d81fd264aecc.pdf (3.8 MB)

Results. No mention of copper project in Press release. expect fireworks in today’s concall

Attended concall, management seems quietly confident though they were not able to answer why they took such high cost loan of $130 million if everything was anyway going to be phased. Total copper project 8000 cr (3000 cr equity + 5000 cr debt), 5000 cr net of taxes expected from Dystar. some payout to shareholders, rest war chest for future. Chemical biz guidance lowered to 1200 cr from 1500 cr

2 Likes

He wanted to issue warrents and justify it so only all this drama

Cash is not required by kiri to do anything but how will u issue warrents so only this copper project shield

Could you please elaborate on this line of thought? I am unable to understand what exactly do you mean.

He said half of 130 million dollar loan is sitting idle then why you need a warrent issue to infuse capital?

I think retail investors must file a complaint of raising loans and capital and doing nothing with it.