Lots of discussions in this board is like counting the chicks before they are hatched. A figure of 650-680 million $ is being suggested. But are we not forgetting one thing? It is a bidding process, right? So there is every probability that prices will be quoted lower. Then what happens? Rebidding? The process is then delayed. Moreover we do not know as to number of bidders. More bidders will give confidence.

Any learned member can throw light on the process and chances of amount received?

1 Like

Did anyone attend the investor meet yesterday at Mumbai and share the takeaways from that meet( on the court case)

This was precisely the reason why Longshen/Senda challenged the priority payment to Kiri in the last couple of appeals and which they have eventually lost… Kiri owns some 33 percent in Dystar so there is a lot of margin to recover the judgement amount..but the worry of Senda that it may not receive the full amount as per the valuation arrived for Kiri shareholding is real as there is a long stop date for conclusion of this sale process and therefore this cannot go on indefinitely

1 Like

Thanks for your clarification. In that case what prevents Longsz to be a bidder?

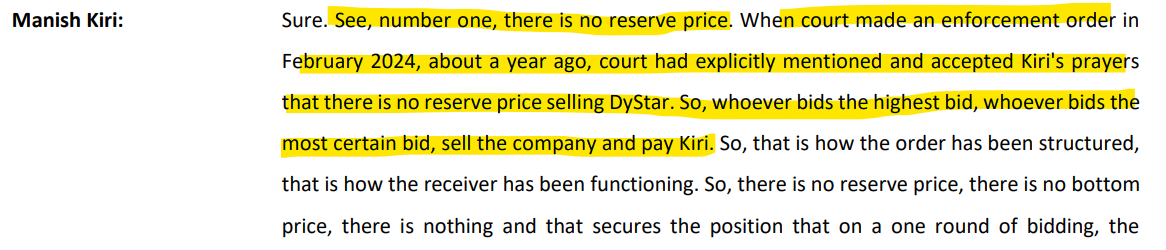

There is no reserve price in this bid so no chance of rebidding. Kiri entitled to 600 million usd on priority, irrespective of sale value, any gain or loss because of bid price on Senda account. Mgmt clarified bids in excess of $1.3 billion but yes if bids below 600 million, Kiri will get less than 600 million

Prabhat Ji, in its earlier judgement Longshen was asked by the Court to acquire the shares owned by Kiri at the derived valuation but it later came back to Court and expressed its inability to do so.

This also elongated Kiris wait for compensation .. if they are eligible to bid they would bid i suppose, through a subsidiary, a group company…but what is clear after the long protracted legal battle in Singapore courts is that priority payment is Kiris along with interest @5.33 % from sep 2023 until payment received (please double check) plus some costs from the enbloc sale of dystar

1 Like

Any acquisition of DyStar is bound to take time as per process.

-

Deloitte finalization and due diligence of bids may take 2 months from 07th Mar

-

DyStar shareholders should approve (2 weeks if the Chinese company does not sulk)

-

Creditors of DyStar need to approve

-

Acquiring company board should approve

-

All M&A in India go through Competition Commission of India (CCI) needs to approve (govt bureaucracy) and also SEBI on behalf of protecting shareholders. Similarly, Singapore might have similar antitrust laws to prevent anti-competitive practices

-

Since this is denominated in foreign currency, it has to go through our Foreign Exchange Management Act (FEMA) (again govt)

Multiple countries are involved in the deal - India, China, Singapore, acquiring company country

The biggest risk factor for further delay would be majority holder Longsheng choose to litigate further. If the deal is at least USD 1.9 billion then they get an equivalent share for their 66% holding as Kiri get 600 million for 33%.

In a good case scenario it might take 6 months from 07th Mar the bids receival date. Or the longstop date given by court this calendar year end.

2 Likes

You can read the previous concalls on the topic of Dystar valuation.

There is virtually no risk of Kiri not getting their due payment as they have been awarded their share by court.

Re-posting my old comment:

2 Likes

Manish ji has almost clarified via hints in the comcalls that dividends are the last thing on their minds but not completely closed out. They want to reinvest everything sooner or later and push for the growth trajectory as they are very hungry for it for over 10 years now. Another hint was the mention of their hydrogen initiative.

I have a strong feeling that their Indo Asia copper will.be acquired by the behemoths sooner or later. Some will jump on me saying that we are counting our chickens before they have hatched but if one has followed every development related to the litigation and the copper scene globally and in India, then one will share the same clarity as I am able to see.

Also hydrogen is the only next major breakthrough sector with a large scale multi sectoral impact globally after copper. Feel free to correct me please.

So this company’s board has its eye on the best bets and is at the springboard of being a growth stock given its current valuation. Once it runs up post or just prior to the receipt of the amount, then we may or may not see the effect of commodity businesses.

This is specifically for others who are still doubtful about this stock yielding returns in the medium term -

It is worth one’s while to dig deep and study every published document instead of simply casting doubts herein. One hint - for those who may not be aware, use Google alerts and set alerts for Kiri industries, copper demand, copper supply, dystar. One will be alerted as the story unfolds.

Also in their last and I guess the only “fancy” presentation from them they have hinted that they may be open to expansion in their current dyes business but they have sufficient spare capacity as yet and have multiple times denied the imminent possibility of expansion capex in the dyes business, so that is just for presentation sake. But the idea of the presentation shows that they are waking up to the idea of attracting institutional interest and announcing more loudly that they are about to arrive.

Disclosure: Invested with high conviction from low levels and almost bought every major dip.

6 Likes

What will be the cash Component that kiri will receive, if bids came at low pricing?

The cash amount is purely dependent on the bidder’s pricing.

Till the bidder is not finalised we can not expect the the exact value of cash that kiri likely to be received.

Management guided that they will recieve the amount in this Financial year and later they further postponed the time!

It takes time and those who are having patience and conviction can hold further.

Disc: Had positions

1 Like

Kiri gets priority payment of USD 603 million as per Singapore court order. Meaning if buyer pays 610 million Kiri will get 603 and the other partner Senda will get the balance 7 million. Although Kiri holding in DyStar is only 33 percent vs Senda owns 67 percent.

As per mgmt talk in last concall, the bids were between 1.3 to 1.9 billion but we can never be certain until amount is realized. You are right it could take time of about 6-9 months.

3 Likes

The global Organic Dyes Market Size is estimated at $4.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 5.3% to reach $7.7 Billion by 2034.

1 Like

“Copper is the next gold” say’s Vedanta’s Group chairman Anil Agarwal. So many new plants announced in last few months - by Birla, Adani, others. But, I think there will be enough room for all given the huge demand and that India is importing large amounts now. For Kiri execution will be the key for their new copper plants.

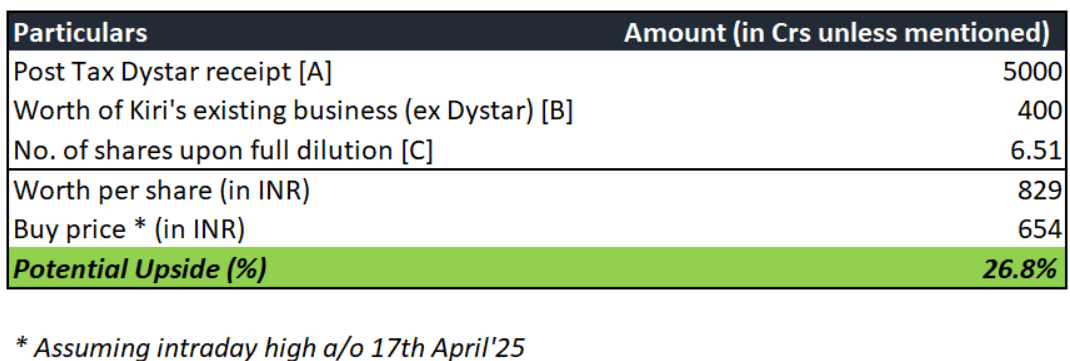

At current prices, here’s how I see the risk reward ratio:

Majority of Kiri’s ~₹3500 crs market cap comes from the anticpation of the Dystar proceeds. Assuming a conservative price-to-book of ~1x, Kiri Industries’ worth (ex - Dystar proceeds) would be ~400 Crs. As such, we may expect the following upside from the stock on a fully dilutive basis (i.e. given that promoter exercises all the warrants) and the sale price works out.

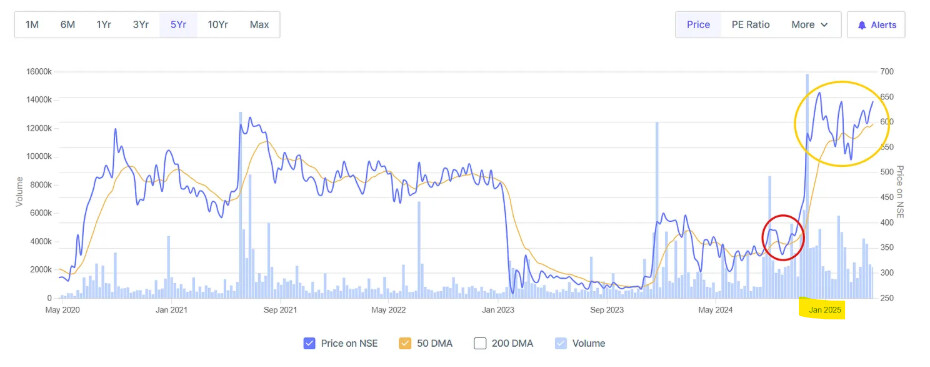

Since Nov’24, after the promoters exercised the warrant the stock has doubled from ₹350 to ₹650 in anticipation of a quick resolution. The enthusiasm persisted in January’25 when SICC awarded the interest and legal fees payment of USD 83.8 Mn. In the last 3-4 months however, the stock seem to be consolidating b/w ₹530 - ₹650. This consolidation is due to the absence of any formal bids.

I believe that the if the stock price where to appreciate, it would in a staggered approach. Bid start to come in > buyer is finalized and sale price gets fixed > Important regulatory approvals are in place. However, the markets discounts the future and thus the impact of the proceeds would be fully priced in way before the actual money is received.

The Risks

- Sale Price - The elephant in the room is that there has been no known official/formal bid from any prospective buyers. In 2024, Deloitte & Touche LLP was appointed to invite bids and oversee the auction process with expected completion by Dec 2025. But no new updates regarding any strong interests or bids have been notified. Also there isn’t any reserve/floor price which creates further uncertainty in the final sale amount.Also, given prospective buyers would know there is some desperation to sell Dystar along with global certainty owing to tariffs and all, the final sale amount may be settled at a significant discount. Also, given the size of the acquisition, it may be a cash and stock deal rather than an all-cash deal which may complicate the payout.

-

Timeliness - Given the judgement from SICC is in full favor of Kiri, there is little that Longsheng can do to overturn the same. The main risk as of now is that receipt of the proceeds being delayed beyond the end of 2025 for regulatory reasons such as acceptance of a formal bid and due diligence by Deloitte. Then there are approvals required from shareholders and creditors of DyStar. Followed by possible regulatory approvals from the Competition Commission of India, SEBI and FEMA (due to exchange of foreign currency). Also, correspondence of all these will involve jurisdiction of multiple countries – India, China & Singapore. All this can can lead to a drag on the time to receive the money. This point was very well pointed out by @Swaroop_NS ji.

-

Then there is a tail risk that Longsheng chooses to litigate further. Chances are low but we have seen it happen before.

The bet is on the receipt of the money and the investment is likely to be exited once the likelihood of the same is entirely established. In between expect volatility if the bids are lower than expected or Longsheng comes up with new antics.

For people who are new to this thread/ having gaps in knowledge or requiring a refresher, I have written on Kiri’s case with Longsheng in great details. The history of the company and the case, the latest triggers including the warrant exercise, judgement based funding and much more are exclusively covered here: Kiri Industries: 3500 Cr mcap Co awaiting a 5000 crore payment

2 Likes