I don’t think we should be looking at this company as a covid play anymore. Apparently, the management also might not be that interested in covid related business as they have always highlighted drastic reduction in price and fierce competition but i like that they held on to their margins. I will be watching for growth of their core business particularly export numbers, progress on amalgamation and subsequent NSE listing and prudent use of cash. Promoter’s recent buying in Nov/Dec from market also inspires confidence.

Most likely they have been using Covid sales to build long-term relationship with the (customer) labs. They seem to have spent a lot of time in customer support/training for the Covid kits, which partly explains slower execution on other fronts (exports, NGS, antigen tests). They seem to have been selective in choosing customer labs, keeping the margins intact. Trurapid has come late but seems on the lines of the long-term strategy of offering similar non-Covid rapid tests.

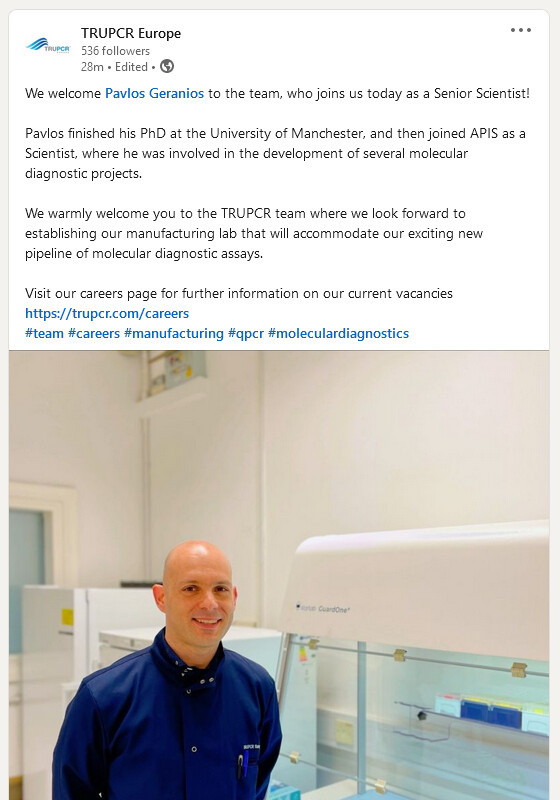

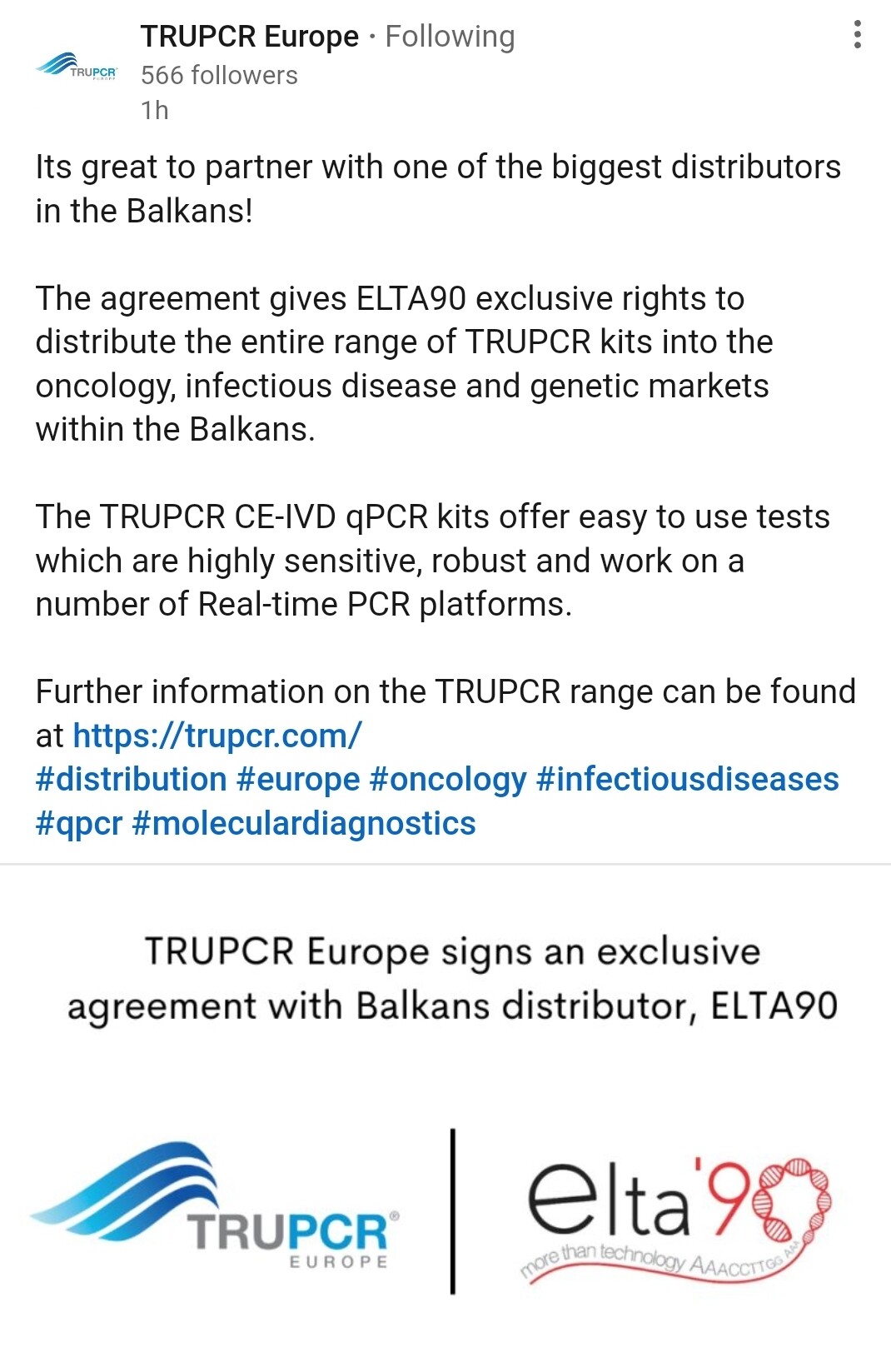

HS BioLabs is rebranded as TRUPCR Europe. The website (https://trupcr.com) indicates that company is focusing on expanding througout Europe and want to begin manufacturing the Kits there. TRUPCR Europe is also hiring in that direction.

Looks like the export numbers should be showing uptick in coming quarters.

In their 2021 AR, they have shown an expense of almost 3Cr as Directors Commission. This wasnt mentioned in Management remuneration. Is it strange or an acceptable accounting practice?

Also, I find it strange that their biggest contribution in Expenses is not detailed out for shareholders. 14cr of misc. expenses is very vague to me as an investor.

Results are okay. Progress on all fronts is much slower than my expectations one year back but now I have adjusted my expectations.

Some positives:

The non-Covid business is better articulated in the investor presentation. This can act as a catalyst for price re-rating at an opportune time.

Revenue growth guidance of 30-35% per year is in line with the investor expectations and the past.

Europe should start contributing to the revenue soon, with high margins given the past record.

Neutral:

The company is trying to expand in the Mid-east. While it gives more choices to the company to sell its products profitably, how well the geographical diversification will be handled remains to be seen.

Negative:

The agrochemical business has stopped contributing to the bottomline again. It is discouraging to see them attempting to expand to neighboring countries in the future. They should have gotten rid of this business at a good price. The tendency to hold on to this business despite low margins contradicts the focus on high margins in the diagnostics business.

Deducting the cash of around Rs 100cr, the business is available for around Rs 160cr. The stock remains severely undervalued partially due to delay in meeting investor expectations. However, given the past record, the management seems to have a way of slow and steady progress, and exceeding expectations in the longer term.

Sharing summary of new article on DNA Extraction Kit Market.

" According to Arizton latest research report, DNA extraction kits market expected to grow at a CAGR of 7.7% during the forecast period 2022-2027. Kits for extracting RNA and DNA are in high demand. The DNA from the samples is used in PCR, genome sequencing, and cloning. As the need for this application develops, the market for DNA Extraction kits will grow as well. The increased scope of applications has largely increased the usage of DNA extraction kits. More R&D in the fields of biologics, molecular science, and genomics will further increase the use of DNA extraction kits."

I have a question, if someone can please answer: If they haven’t disclosed valuation at which they bought HS Biolabs, how can one develop confidence on the prudence? It is one thing to write in presentation that we are valuation conscious but some proof of that would be helpful right? They have given HSB revenue. If we know the valuation, we can find the P/S multiple. (At least I could not find this number, please correct me if they have given it)

HS Biolabs – rebranded as TRUPCR Europe – seems to have given Kilpest not only a foothold in the European market (for sales) but also an access to a good talent pool in molecular biology.

In the last month or so they have hired couple of PhDs in molecular biology/genetics from University of Manchester. Hopefully this more than compensates for the loss of their R&D Head.

The Nov 3 2021 deal disclosure did not disclose the price or consideration paid for the 70% stake acquired in HS Biolabs. What we do know from related party disclosures on June 7 2022 is 10.4 cr has been invested in HS Bio. If this was a pure primary transaction with no purchase of shares from HS Bio owners, then the pre-money valuation is 10.4 cr/70% = ~15 cr.

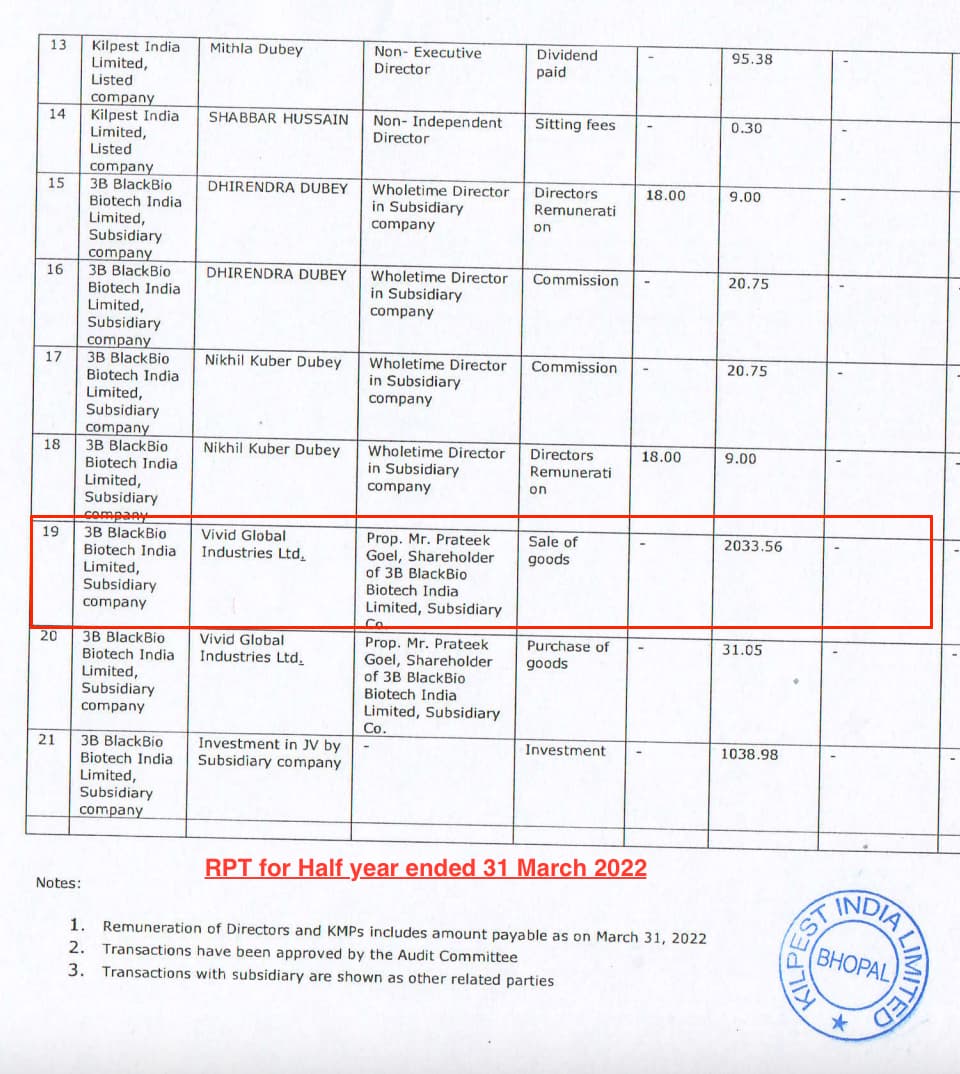

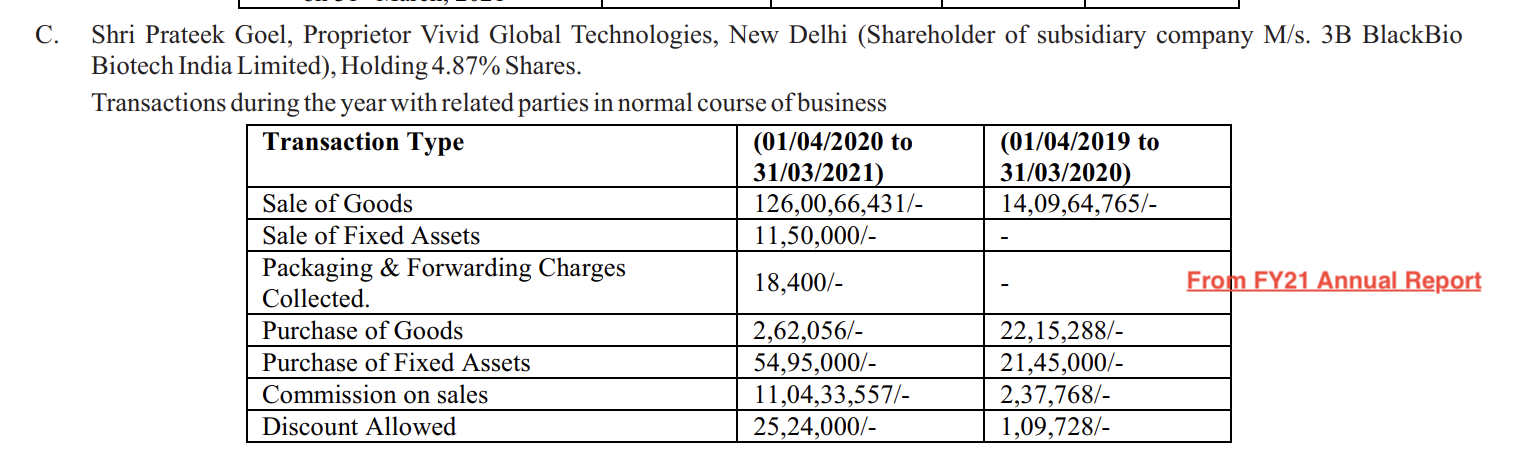

On the topic of disclosures, another thing which missed my attention earlier was the related party transactions between 3B Blackbio and Pratik Goel’s (KMP) unlisted company Vivid Global. Nearly the entire diagnostics sales is routed via this unlisted company. There is no clear business reason for such an arrangement.

Thanks Sahil, all great points there. From LinkedIn one can see that they have hired a couple of senior scientists and rejigged the titles a bit so there is decent bench strength on the R&D side and I expect they will fill this position as well.

On the RPT topic, point well taken and I do agree that RPT are par for the course in Indian business. What I have normally seen in promoter run companies is a certain % of purchases from unlisted promoter companies, rental agreements between promoter and co, commissions etc. In this case, the entire sale of the diagnostic business is happening to Vivid Global which to me is unusual. A rational explanation for this could be that Vivid has some licenses or pre qualifications that 3BBB does not have - but this is not apparent and might be worth digging into.

Point number 5 has disproportionate weight as per my understanding.

There already are technologies that would change the way diagnostics functions. For eg, lab-on-a-chip, leveraging microfluidics to have concurrent tests with much lower reagent volumes. Reagent and other raw material minimisation, requirement of lesser staff and reduction in the unit cost of a test in return. Simplistically, from economic POV. There are other many advantages as well.

This could severely challenge the economic model. Not very soon but from a terminal risk POV. The disruption has many externalities as well, starting from regulations all the way to the ability to be done at scale.

I am not sure of the domain covered by NGS foray of Kilpest and if this is relevant. Had a DNA based test past week, details of which are personal in nature. This was not offered by the typical labs and had to go for a genomics company (most of which seemed busy with PCR). They charged 16k for this and it took 8-9 days. The prescribing doctor had offered an alternate test for 2.5 k with 95% accuracy but gene test was 99.99%, so better to save at D-mart instead.

They called it an Illumina machine based (Sanger was the older method before NGS). While researching this found that most websites with details were based outside India, mostly UK, australia etc. So it might be Kilpest is indeed targeting the right markets, given the expensive nature. Likely insurance covers it in many developed countries. While resident in EU, all insurers had to offer a basic policy with absolute 100% coverage, without any fine print or exclusions. It may be difficult to generate enough demand in India. Selling in UK might be easier, targeting india-based company’s products to a Dr. Patel etc.

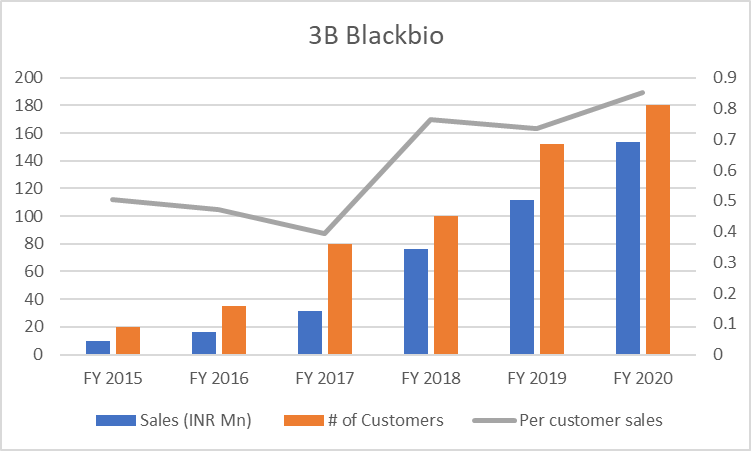

(Deliberately taken only till FY20 since 21 and 22 has large component of Covid sales. Although they are giving non-Covid sales, they are not giving no. of non-Covid customers)

Reasons I could think of:

1 Cross selling new products to existing customers

2 Gaining wallet share in existing products from existing customers

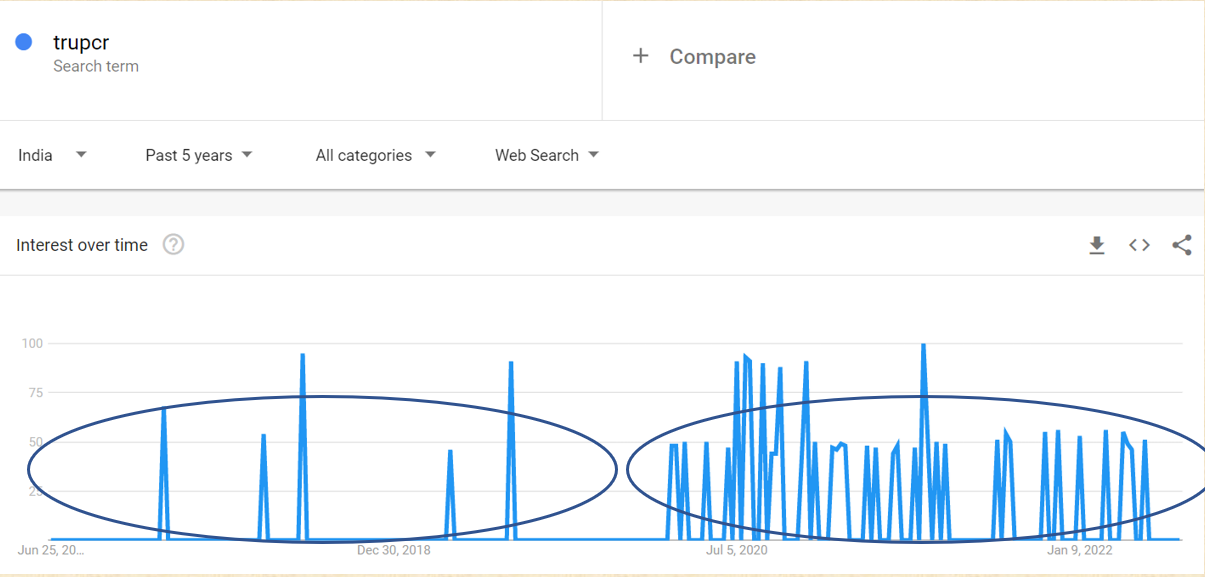

GTrends for trucpr hints that perhaps Covid has accelerated non-Covid testing too

Would just like to add why it might make sense to have some manufacturing on-site in UK. Philips has sold off almost all its traditional biz, the only one retained is healthcare for strategic reasons. There is demand in Europe and govts do not want to spend money on buying non-european stuff. So it makes sense to have more than just a front-end in UK. Several pharma companies seem to be doing this also.