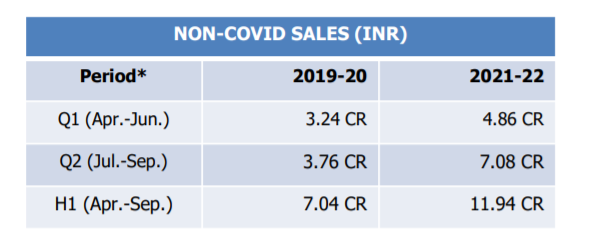

Kilpest India / 3BBB Q2 FY22 Investor Presentation -

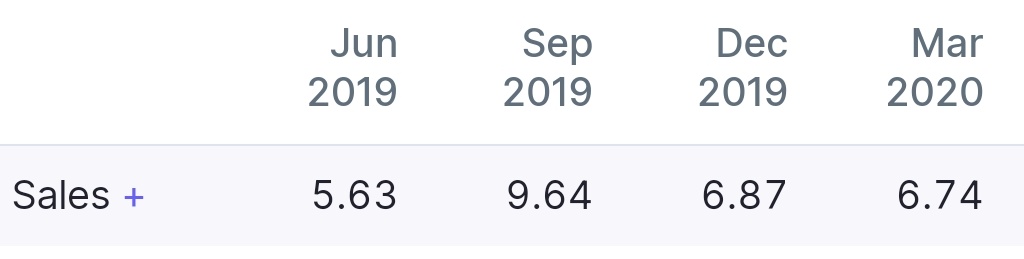

Non - Covid Revenue in 3BBB has started to increase YOY wise

Indicating Less dependency from Covid - RTPCR Kits

Kilpest India / 3BBB Q2 FY22 Investor Presentation -

Non - Covid Revenue in 3BBB has started to increase YOY wise

Indicating Less dependency from Covid - RTPCR Kits

In the presentation, the company has also reiterated intent to list on NSE and to pursue inorganic growth opportunities. Potential share buyback in case no acquisition target found. Nothing new in any of this.

On amalgamation

“BSE has asked for some clarifications, which are being replied. After receiving the fresh approval from BSE, we will apply for necessary approvals from SEBI and NCLT. We are hoping this process will take a year to be completed from now. Your company is working on faster approval of the scheme, which should result into unlocking the value of Material Subsidiary i.e. 3B BlackBio Biotech India Ltd.”

This is taking excruciatingly long. Not sure if the prices is as complex as they’re making it out to be, it is plain lethargy.

On HSB acquisition

They have said this help them market ‘Made in UK’ products, and cater to the European market and amplify the company’s brand image. Money will be invested in setting up sales and distribution, R&D, marketing efforts and accreditations. They’ve already taken a space in Manchester for R&D and production. Seems fairly logical. No mention of the amount of money paid for this acquisition or investments.

On NGS and Rapid Antigen

“Company expects to launch Rapid Test kits in FY 22-23 for various parameters. Although Indian market price realisation is not very attractive but as a wholesome strategy we are including this vertical, specially to focus on global markets.”

“We are again reviving the NGS kits revalidations and also development of few more parameters, keeping in mind the global markets. Unfortunately in India due to competition between labs the prices for NGS tests are also very un-remunerative, which was one of the reasons to not aggressively launch kits in India till date. NGS vertical can probably start adding some revenue in later quarters of FY 22-23 only.”

I’ll admit I don’t know much about the NGS market dynamics. But prima facie if it is such a competitive space in India, is there really any technological advantage that 3BB has? And why is it less competitive internationally if so many players able to make the kits? From this statement it seems like a commoditized space.

I am unable to answer this question. Would be much obliged if anyone has an answer. If NGS is such a competitive space, why should we be getting excited about it?

With the third wave unfortunately building up though, covid test kits sales in India and the UK are likely to pick up again and bring in fresh cash flows in addition to the main business. I foresee a breakout from the consolidation soon.

Disclosure: Invested and biased.

Full portfolio Vineet Jain portfolio

I have done some digging into your NGS question. I do not have much background in NGS, so most of my writing below cannot be trusted with too much faith.

There are NGS offerings in India from multiple companies, particularly in oncology prominently from Illumina and Thermo Fisher. Illumina’s offering is expensive. Thermo Fisher has a low-cost platform offering; in order to reduce costs, only certain genes understood to be contributing are sequenced, and experts from around the world can offer advice on the sequencing results via the platform. Replicating such a platform seems to be a pretty steep curve to climb. Surely companies like 3BB will focus on other diseases/treatments/methods.

It seems to be very early days in NGS. NGS has a fast-growing market. As gene therapy usage increases, there will be increasing demand of human sequencing. Much more than only human genome is of interest. The human body has more non-human cells—the human microbiome—than human cells. Some parts of the microbiome perform several positive functions related to immunity, digestion and many more and other parts negatively contribute. In the future, we may increasingly see personalised medicines that cater to the microbiome profile of the patient.

It seems to be very early days in NGS. Not sure which areas in NGS 3BB is focusing on. It has to be a well-thought strategic decision. I guess for now they want to focus on the western markets. I speculate the reason is that the Indian NGS market is largely restricted to oncology, which is dominated by Thermo Fisher. In the near term, 3BB investors can look forward to returns from exports and antigen kits, not from NGS.

Disclosure: Invested with large percent of my portfolio.

Is this causing worry to Kilpest share price?

Hope Tata will manufacture low cost in mass.

Disclosure: Invested in Kilpest

For kilpest India the main thing to watch out for this quarter is export revenue and export margin as products are sold at 2 to 3x in USA and UK.

Further this quarter govt had uplifted restriction on kits, covid cases are on a rise, USFDA approved kit, distributor company readily available in USA and most important is recently entered JV with UK company who has expanded their manufacturing site to store more TRUPCR products.

All in all this quarter will lead kilpest to new heights.

Disc- Invested

There is now a cheaper and instant lateral flow test, sourced entirely from China, PCR is almost not being used anymore in UK. I think India has been using the same rule for antigen testing (seems they are calling this as lateral flow), i.e. if positive then no PCR, only if negative and symptomatic then PCR. UK seems happy with ~90% accuracy

Disc: not invested

While lateral flow test is being used more in the UK, we cannot say PCR is almost not being used anymore. There is high prevalence and the move is aimed at ensuring PCR is available to those who need it. It seems PCR supply has not been keeping up with the demand.

In India too many state governments were using antigen tests during the times of high prevalence (they were criticised for doing so). Not only it reduces costs to the governments, it also ensures PCR tests are available.

After having acquired majority stake in HS Bio in UK with expanded capacity, the company still has around Rs 100 crore cash and investments. Subtracting that from the market cap, the market is giving only around Rs 250 cr valuation to the Covid + non-Covid diagnostics business. In the past, the company has shown extraordinary return on capital, so actually the market should be giving higher valuation to the cash component.

Promoters have been buying in Nov and Dec 2021 around 450 levels. I believe these prices will act as the new support. The current market price is very close to the 50-day moving average and the 200-day moving average. The last time this happened in April 2020 and March 2021, the stock price moved up significantly over the next few months.

Btw, 3bbb is developing antigen tests too.

When investing company we are investing in their capabilities not the earnings in here & now.

They are in process of developing antigen from last 1.5 years.

Management is not walk the talk. Just postponing its launch from one quarter to another. Not a good sign

When for a microcap, stock goes up many many folds in short amount of time ( 80s to 700s between first and second wave of Corona), and promoter do not sell at all , rather start to buy back recently when stock comes back to sub 500. Tells something about promoter.

No investments.

Unfortunately most of the market participants are still looking at Kilpest as a covid kits business and most of analysis/discussion ends up at covid kits and relevant business. Lets make it clear that the covid kits business was a windfall gain and its no more lucrative due to the following reasons:

So, focussing on just covid kits business is not a good way to assess the compnay fundamentally.

The management also emphasized already that they want to focus more on the export business with the core product offerrings.

In line with this, acquiring stakes in HS Biolabs is an excellent step forward, will help them making inroads to european markets through their own local manufacturing, and grabbing market share.

They are building a new facility for rapid antigen kits (not only covid but few others also), and the purpose of doing it just to complement their product suite as a global MDx player:

Please note here that they had submitted their antigen kits to ICMR for validation sometime back, but it was not approved, and the co have not pursued again so far to re-validate it. May be they are still working on it, but i guess they are not just focussed on having antigen kits for covid-19 only as its not much profitable now(I think they earlier mentioned this once also).

https://www.icmr.gov.in/pdf/covid/kits/List_of_rapid_antigen_kits_06012022.pdf

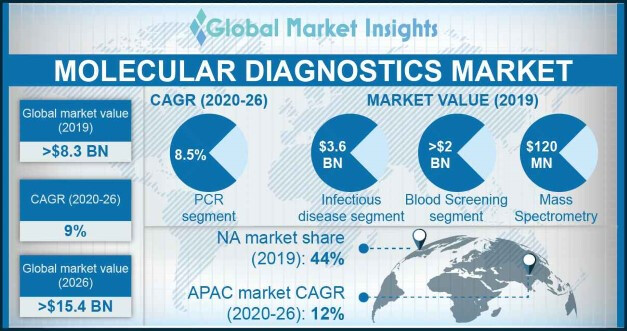

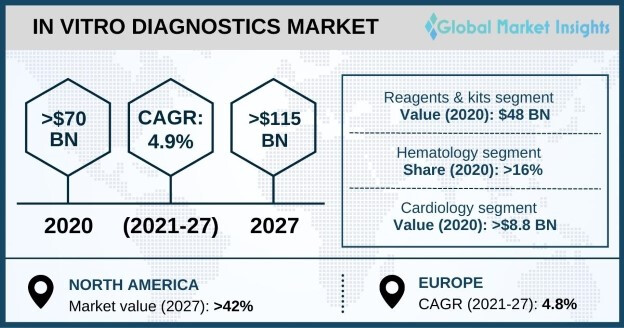

Since they are focussing more and more on being a global player now, lets have a look at how the molecular diagnostics industry is growing globally, particularly after the covid saga.

As per the GMI research report (which co also refferred in their presentation in the past) of 2019, the global molecular diagnostics industry was growing at 9% cagr, APAC market was growing at even faster pace (12%).

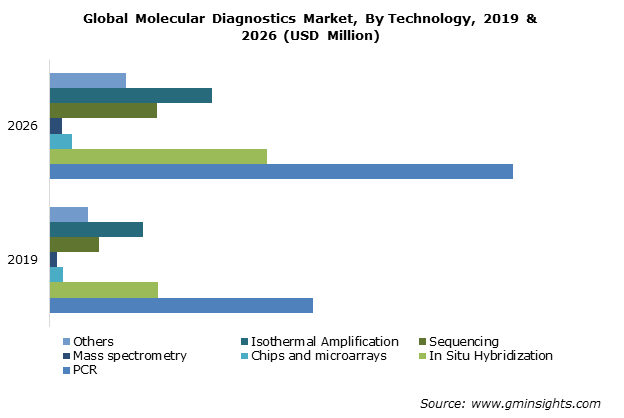

Among molecular diagnostics the PCR based segment takes the largest pie and also growing at the fastest pace, where Kilpest is present:

Source: https://www.gminsights.com/industry-analysis/molecular-diagnostics-market-report

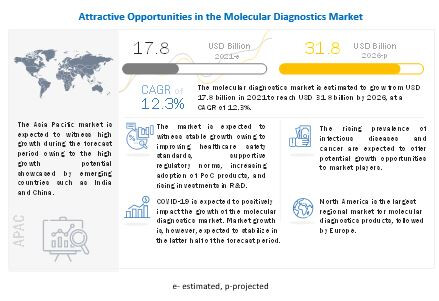

They have not published any report after Covid happened, but from other research houses, it is evident that the industry growth has been accelarated after covid and increasing prevalence of infectious diseases, the growth rate is een more in asia pacific region:

Source: Molecular Diagnostics Market Size, Share, Trends and Revenue Forecast [Latest]

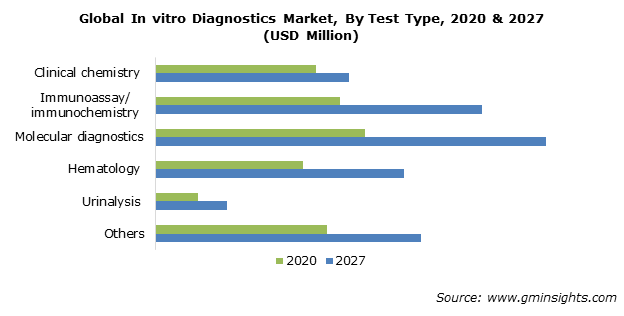

Molecular diagnostics takes the largest pie globally from total IVD (In Vitro Diagostics) market:

Source: In-vitro Diagnostics Market Share - Forecast Report, 2032

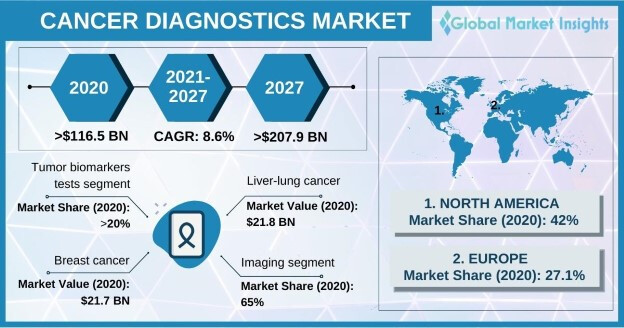

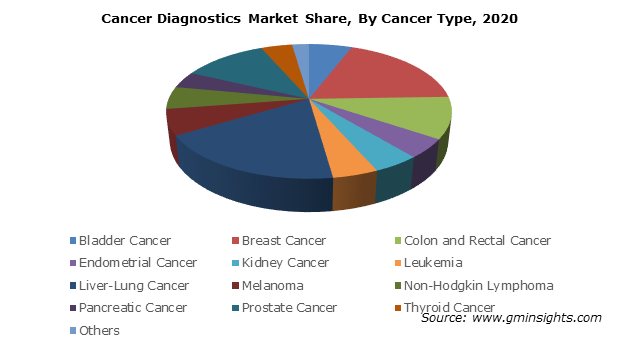

Now, lets look at the oncology diagnostics market growth and the opportunuty size:

https://twitter.com/punitbansal14/status/1481866845405782016

As per the GMI report, the oncology diagnostics market is growing at 8.6% annually till 2027, biomarkers segment forms 20% of it:

Also, read this good report on the PCR based oncology diagnostics growth:

https://www.marketwatch.com/press-release/oncology-molecular-diagnostics-market-new-innovations-trends-research-global-share-and-growth-factor-2021-11-26

The oncology molecular diagnostics market is expected to register a CAGR of more than 12 % during the forecast period.

Key Market Trends

Polymerase Chain Reaction (PCR) is Anticipated to Observe a Significant Growth

Based on technology, polymerase chain reaction (PCR) is anticipated to witness significant growth. Presently, the polymerase chain reaction (PCR) is the most preferred technology for studying cancer. The major factors contributing to the increasing demand for PCR in oncology molecular diagnostics are greater sensitivity, quantification, ease, precision, and reproducibility, better process quality, fast analysis, and lower risk of contamination.

I have compiled some important parts from various research reports, just to keep a record in this thread and to refer later.

All in all, it is quite clear that the molecular diagnostics and also cancer molecular diagnostics market with huge opportunity is growing at roughly double digit, at a time when covid as a infectous disease has just shown its devastative nature to the world and the role that molecular diagnostics can play to defense it. Also its a good strategy from management to focus more on export/global market and aquiring a european distribution player. We need to see how it goes and also very importantly how can management utilize the cash reserves to benefit from this huge industry tailwinds.

Can they compete with global players? I think two things are most important here, distribution channel and their product quality. Product quality of Kilpest can match with global players which has been discussed already in this thread at length (also being only USFDA-EUA approved covid kits from India talks about their kits quality) and they are already working on distribution channel. They have partnered with Genophyll for US market and acquired HS Biolabs for european market. Also, cost-comepetitiveness will be in their favour being an indian player. Even if they can grab a smaller pie from the global market, base effect will be at play and Kilpest can reach to greater heights.

Remember, this company was growing their non-covid diagnostics kits business at more than 40% cagr before covid arrived. Even during covid, that growth did not stop.

Disc: Invested from lower level, my views are biased. I am not sebi registerd advisor and this is not any recommendation.

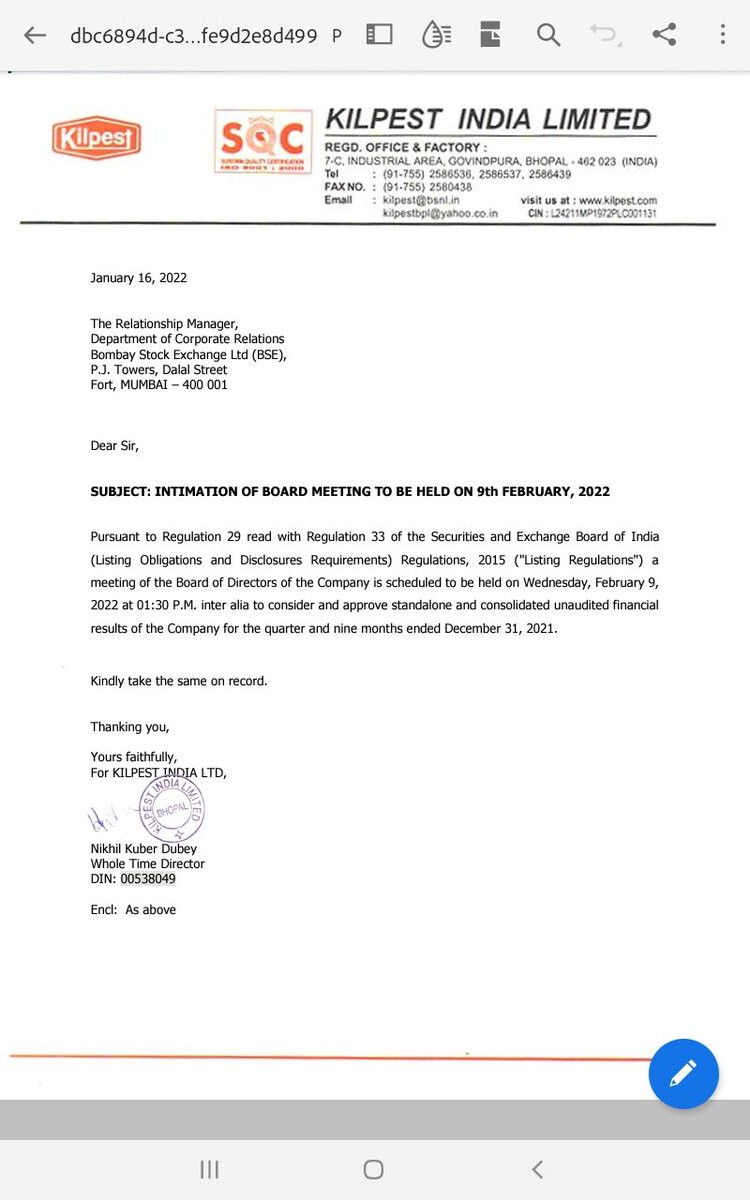

Corporate Announcement Update -

Company will have board meeting on 9th Feb To discuss 9 Month Ended & Q3 Results of Company

We are pleased to inform you that finally after extensive efforts our “TRURAPID® COVID-19 Ag Test”

has been approved by ICMR (Indian Council of Medical Research) on February 2, 2022.Now we will try to build this product assuming that COVID testing will continue depending on the

disease progression with time.Although the prices for Rapid Antigen Test for COVID have dropped to a very low level, still we will do

our efforts.

We were hoping for this announcement but I am a bit disappointed by the understated announcement. No mention of exports or development in other markets.

I feel mostly it will be covered in investor presentation during the upcoming result

Hello @msandip . Thanks for detailed updated.

Could you find or calculate the covid vs non-covid revenue and profits?

Tried to arrive at rough valuation of the company-3BB (ignoring agrochem business altogether)

A. Non-covid

sales (4.86+7.08+7.79) + 8(Assuming similar run rate of last 2 qtr with marginal increase)

PAT @ 45%

B. Covid+Non-covid

Sales: (H1FY22 consolidated-standalone= 39Cr) + 4.18 (Q3FY22 covid sales)+4.59Cr (Jan 22 covid sales) + 8Cr (assuming Q4 Non-covid sales) + 2Cr (assuming covid sales in Feb & Mar 22)

PAT @ 40 (assuming slightly lower margins due lower prices of covid kits)

Based on above, and assuming post amalgamation and renaming it gets PE of 30; I think the non-covid business can be of around 500Cr i.e. 12.6*30 + (cash) with negligible borrowings.

Would love to know if i am missing anything.

Q3 results were along expected lines, nothing to write home about.

The hypothesis for me to invest heavily in Mar/Apr 20 after tracking 3BB for a few years was i) it was one of the few test manufacturers in the country ii) valuations were attractive and iii) relatively shareholder-friendly promoters and iv) I believed Covid was here to stay.

Looking back now over ~2 years of Covid, I must confess I am disappointed with the execution of Kilpest management.

Let’s review what’s happened since Covid started:

They did well to capture Wave 1. This was the “RT PCR” wave and fit perfectly with 3B’s existing capabilities and strengths. Prices were very attractive and they executed well to scale up manufacturing, reaping a ~100 cr windfall in the process.

Wave 2 in April 2021 was bigger than Wave 1 and devastating for the country. This was the “Rapid Antigen” wave and 3B missed a majority of the testing demand which had shifted from PCR due to the immense testing requirement nationwide. They were able to capture a small portion of PCR testing at subdued prices. Of note is that 3BB had been trying to secure approval for TruRapid and failed a couple of times. Scores of other Indian and global firms brought antigen tests to market and they weren’t nimble enough to acquire or partner with any of them.

Wave 3 in Dec/Jan recently was completely missed by 3BB. This was the “Self Testing” wave and 3B didn’t even attempt to build a self testing kits although the writing was on the wall about where Covid testing technology and consumer preferences were going. Their excuse for not pursuing antigen and other kinds of tests was that the prices were too low. This doesn’t ring true - Mylab alone reported selling over 500,000 kits in the first week of January and has probably sold millions of kits at a price of ~200 each. Another huge missed opportunity for 3BB.

Consider what someone like Mylab, founded in 2016, has achieved meanwhile:

This is the progress and nimbleness displayed by the leading testing companies globally, who have brought new products to market and deployed cash aggressively for growth.

3BB on the other hand seems to be satisfied with the windfall from Wave 1 and the only noteworthy development was acquiring HS Biolabs late last year to set up a European subsidiary. As I wrote at the time, I still don’t understand the rationale for this acquisition given that HS Biolabs is just an agent and 3BB has claimed that its India cost structure is its competitive advantage. Other priorities like NGS kit development, listing on the NSE, M&A/buyback etc have not moved at all and we were told the management was “busy with Covid” - viewed in hindsight these were symptoms of a deeper issue of management bandwidth and growth mindset.

To be fair to the management, they have consistently tried to downplay expectations and give a fair assessment of what normalised performance might look like. For my part, it is the lack of ambition and missed opportunities that pinch and I wonder if they will feel the same way down the line.

Apologies for the long post but wanted to reflect on reasons for reducing my position since I have been writing consistently while investing. Valuations now seem decent at 15x core earnings ex cash but reducing to a tracking position until growth trajectory and management hunger become more visible