Even Meghmani Organics is into CPC Blue space, I saw their AR and noted 86% capacity utiisation and EBITDA margins for that division of 14%. Kesar’s capacity utilisation for FY18 is around 40% and EBITDA margins of 22%. Have to see how they plan to increase the capacity utilisation.

The company’s ROCE has been increasing from -3 to 55 in 10 years

P/E of 5, ROE: 44, ROCE: 55, ROIC: 42

Promoter holding: 63%

Company has good consistent profit growth of 176.22% over 5 years

Stock is trading at 1.14 times its book value with no debt, is the management integrity in question, as they don’t pay any dividend?

Kesar Petroproducts has signed an MoU with Govt. of Assam to invest Rs. 2,000 cr. for production of methanol from raw bamboo. Present M. Cap. is Rs. 272 cr.

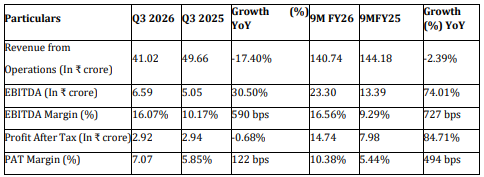

3% revenue growth YOY, 111% EBITDA growth, 71% PBT growth and 102% PAT growth.

PAT growth looks higher as company as company has not made any tax provision in this quarter.

If seen on QOQ, revenue is flat, EBITDA has fallen by 15% and PBT by 22.7%; underperformance is largely due to higher COGS compared to last quarter which resulted in gross margin compression of 240bp

Operational Resilience: The company faced challenges due to US-India tariff developments, which created temporary pressure on volumes and margins. However, they maintained operational discipline and focused on improving capacity utilization.

Shift in Product Mix: Kesar has successfully transitioned from being a crude manufacturer to a pigment manufacturer. The management noted that crude sales now account for only 1-2% of revenue, while higher-margin products like Alpha Blue (151) now contribute significantly.

Utilization: The company is currently operating at 65% to 70% of its installed capacity.

Outlook (Revenue & Margins)

Bottom-Line Growth: Management is maintaining guidance for 100% year-over-year bottom-line growth for the full year.

Margin Targets: They are targeting EBITDA margins of 15% to 16% for the current year. Long-term guidance suggests these margins could improve to the 16-18% range as high-margin “core products” contribute more.

Growth Guidance: The company reiterated a long-term CAGR of 18% to 20% for top-line growth over the next three years. Specifically for next year, they are focusing on a 20% top-line growth target.

New Product Integration (Fertilizers & Chemicals)

Complex Fertilizer: A major strategic move is the launch of technical-grade complex fertilizers derived from by-products. This product is an import substitute for India and will be used primarily in drip irrigation.

Commercialization: Commercial production of the fertilizer started in Q4 FY26. It is expected to contribute ₹30 to ₹40 crores in revenue at full capacity (3,600 metric tons per annum).

Zinc Phosphate: Another core product, Zinc Phosphate, is expected to come online toward the end of next year’s final quarter.

Capex & Cost Savings

Asset Capitalization: A significant ₹78 crore Capex for the complex fertilizer plant was sitting in Capital Work-in-Progress (CWIP) and was capitalized during the reported quarter.

Cogen Power Plant: The company is operationalizing a power plant in phases. While the boiler is active, the turbine is expected to be on board within three months. This is conservatively expected to save ₹3 to ₹4 crores annually in power costs.

Other Key Financials

Debt & Working Capital: The company has decreased its long-term debt. They do not anticipate needing incremental fund-raising to support current growth plans as they optimize their working capital cycle.

Dividend Policy: Management confirmed that a dividend policy is in the works and investors could likely expect dividends starting next year.