Thanks @Ananth_2016 for initiating a thread on Kennametal. I had also worked on the company and prepared a brief note on Kennametal Inc few months back. Sharing it here:

About the company

Kennametal India Limited (KIL) is a subsidiary of Kennametal Inc which holds 75% stake in the company. KIL is engaged in manufacturing of tools and engineered products for metal working, mining, construction and other engineering applications. The products include cemented tungsten carbide, high – strength steel (HSS) and wear resistant carbide products.

The company has two major segments – hard metal and hard metal products and machining solutions which contributed 85% and 15% to company’s sales during FY18 respectively.

Brief history of KIL

KIL, formerly Widia India Limited, was founded in 1964 by Krupp Widia AG, Germany (Krupp Widia), and an Indian promoter, Sak Industries (Sak), to manufacture tungsten carbide metal cutting tools. In 1995, Cincinnati Milacron (CM) acquired Krupp Widia. Sak Industries retained its 25.7% stake in Widia India. In May 2002, Kennametal Inc acquired CM’s global operations, and gained 51% stake in Widia India which was renamed as KIL. Subsequently, Kennametal Inc acquired Sak’s stake in the company and post open offer held 88.16% stake in the company. Currently, Kennametal Inc, hold 75% stake in the company, following dilution to the public post the new SEBI rules of promoter not holding more than 75% stake in the listed company.

Business segments

Hard metal and hard metal products

In the hard metal and hard metal product segment, the company has industrial, infrastructure and Widia segment. Industrial segments mainly caters to industries like steel, automobiles etc while infrastructure caters to segments like mining, construction etc while Widia also caters to the industrial segment. A snapshot of the tools in the segment is given below:

Machining solutions

The machining solution segment is only catered by KI and not by other companies of Kennametal group. In the machining solution group, the company manufactures customised machines, primarily catering to automobile original equipment manufacturers (OEMs). This division follows an in-house designing and outsourced manufacturing model.

Key segments served by the company

The key industries served by the company includes automobiles including 2 – wheelers, cars, CVs (LCV, MHCV) and tractors, steel, aerospace, defence and railways, for green field manufacturing set up, oil & gas and mining. Although, the company doesn’t give the breakup of sales within the segments, the company seems to be largely dependent on automobiles with most of the other segments not growing well. However, it seems that some of the segments like aerospace, oil & gas, mining, defence and railways and even private capex are reviving which should help in growth of the business.

Competition

The major competitors of the company including Sandvik and Iscar (owned by Berkshire Hathaway). Sandvik and Kennametal both claim to be the market leaders in the machine tools segment with 25 – 27% market share each (as per CRISIL) with Iscar holding around 15 – 20% market share. The rest of the market share is held by imports from Europe and other Asian players.

What makes KIL interesting?

Revival in capex cycle: There are green shoots that capital investment in manufacturing including Greenfield facilities, oil & gas, energy and mining are also reviving which should help the company in higher growth.

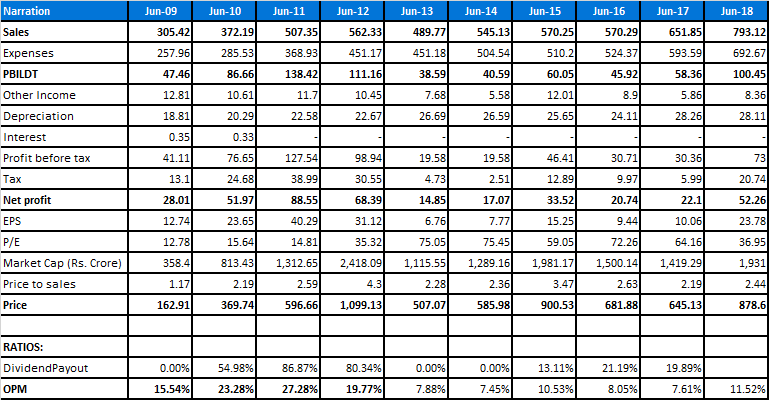

Operating leverage and other cost cutting measures leading to improvement in profitability margins: Let us first look at the key financials of the company over the past 10 years:

During FY11, the company had PBILDT of 27.28% which has reduced over the years and has now shown some improvement during FY18 with margins improving to 11.52%.

The parent company, Kennametal Inc, has taken various initiatives to improve the profitability margins which should also trickled down to the Indian subsidiary.

Some of the initiatives include – focus on reducing the number of products and phase out the ones which have low margins, improved sales execution and focussed initiatives driving growth, have different sales force for Kennametal and Widia brand, modernization and automation of facilities to reduce employee costs, strategic sourcing of key raw materials .

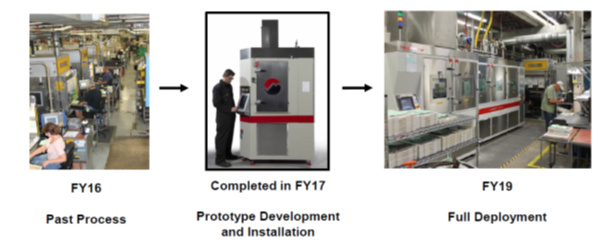

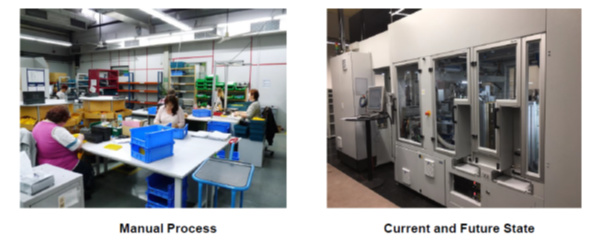

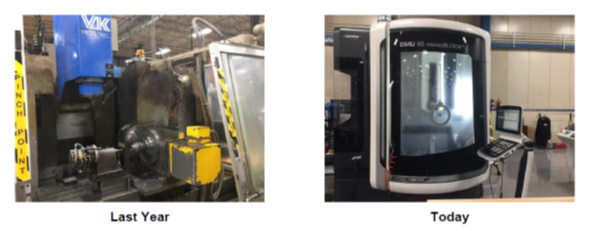

Some of the automation initiatives are given below (taken from Kennametal Inc Investor day Presentation):

Some of these initiatives are also visible in the steps taken by the Indian subsidiary which are expected to improve its profitability margins including:

Giving VRS to employees : KIL has initiated VRS scheme for its employees and has incurred exceptional losses of Rs.5.50 crore and Rs.7.70 crore during FY17 and FY18 respectively. Although, these initiatives might hamper the short term results but would result in reduction in employee cost in the medium to long term.

Incurring capex for expansion and modernisation . During FY16 – FY18 the company has incurred capex of Rs.148 crore including capex of Rs.54 crore during FY18. As per the presentation given during last AGM, the company had used capex during FY17 for capacity enhancement, modernization and capability upgrades.

Operating leverage to play out with increasing sales: From September, 2016, the sales of KIL has increased every quarter on a yoy and qoq basis. With lot of companies in the capital goods sector talking about demand revival, the company is expected to benefit from the same. Most of the industry segment, the company serves including automobile, steel, oil and gas and even new capex seems to be reviving. Furthermore, IIP nos are also showing some turn around in the capital goods sector. Increase in sales can lead to operating leverage playing out in the company and thus increasing the PBILDT margins.

Key Risks

Depreciating rupee to impact gross margins: KIL imports tungsten and carbide as the same are not mined in India. Furthermore, the company also imports some of the finished goods not manufactured by KI from other companies of Kennametal group like Kennametal Europe and Kennametal Inc. Although, the company also exports its products to other group companies and to other countries in south east Asia, the same was much less than the imports.

Expected revival in capital goods industry doesn’t happen

(Disclosure: Invested. This is not a recommendation or an advice to purchase the stock)

Some other readings on the company KMT FY18 Investor Day .pdf (3.1 MB)

KMT Q1 FY19 slides Nov 5 FINAL.pdf (1.1 MB)

A detailed report on Sadvik which gives some details on the tungsten carbide tooling industry.