For the past few days, partner brands like Omega, Armand Piguet, Rolex, Hublot have all been advertising full page print ads in leading newspapers like TOI and ET - after a long time!

The core premise here is that can we expect a good pick up in luxury watch sales in the Indian market? Supporting points for me were:-

Large discretionary spend ability for the rich - similar to demand for luxury cars (only if the supply could match it)

Base year affected by major retail disruptions - watches are very much a touch and feel product and COVID closures severely affected ETHOS

Large pent up demand from the wedding industry and upcoming wedding season should be bigger than even the usual (COVID permitting)

The manufacturing business for KDDL is a relatively stable cash generator - assuming no shortages in Swiss watch industry - across the globe demand trends should remain healthy

Overall, in my opinion, I priced in a much better scenario for the business moving ahead. The potential for the luxury watch industry in India considering posts earlier also was also a supporting factor.

Disclosure : Invested in the stock. Transactions in last 30 days. Not a registered advisor.

Crossed 1000 Cr market cap today. Will be interesting to see if it is covered by some larger funds now.

The advertising for the watch industry continues and hopefully the key triggers in terms of wedding demand and reopening over a very low base continues (if COVID does not disrupt things).

The company is also raising funds through shareholder deposits - recently got an email for the same.

because it unlocks value for KDDL shareholders in two steps

Price Discovery - imho Ethos is Undervalued because it is not independent. KDDL shareholders will hold ETHOS with 30-40% discount as holding company discount. in this Case value of parent will be discounted as it will be tracked as a proxy of ETHOS

Demerger - eventual demerger of KDDL and ETHOS so the holding company discount will go and value of parent will be discovered.

i believe over the next 18 months … holding KDDL could be rewarding

Disc - holding KDDL for past 18 months… hence biased…

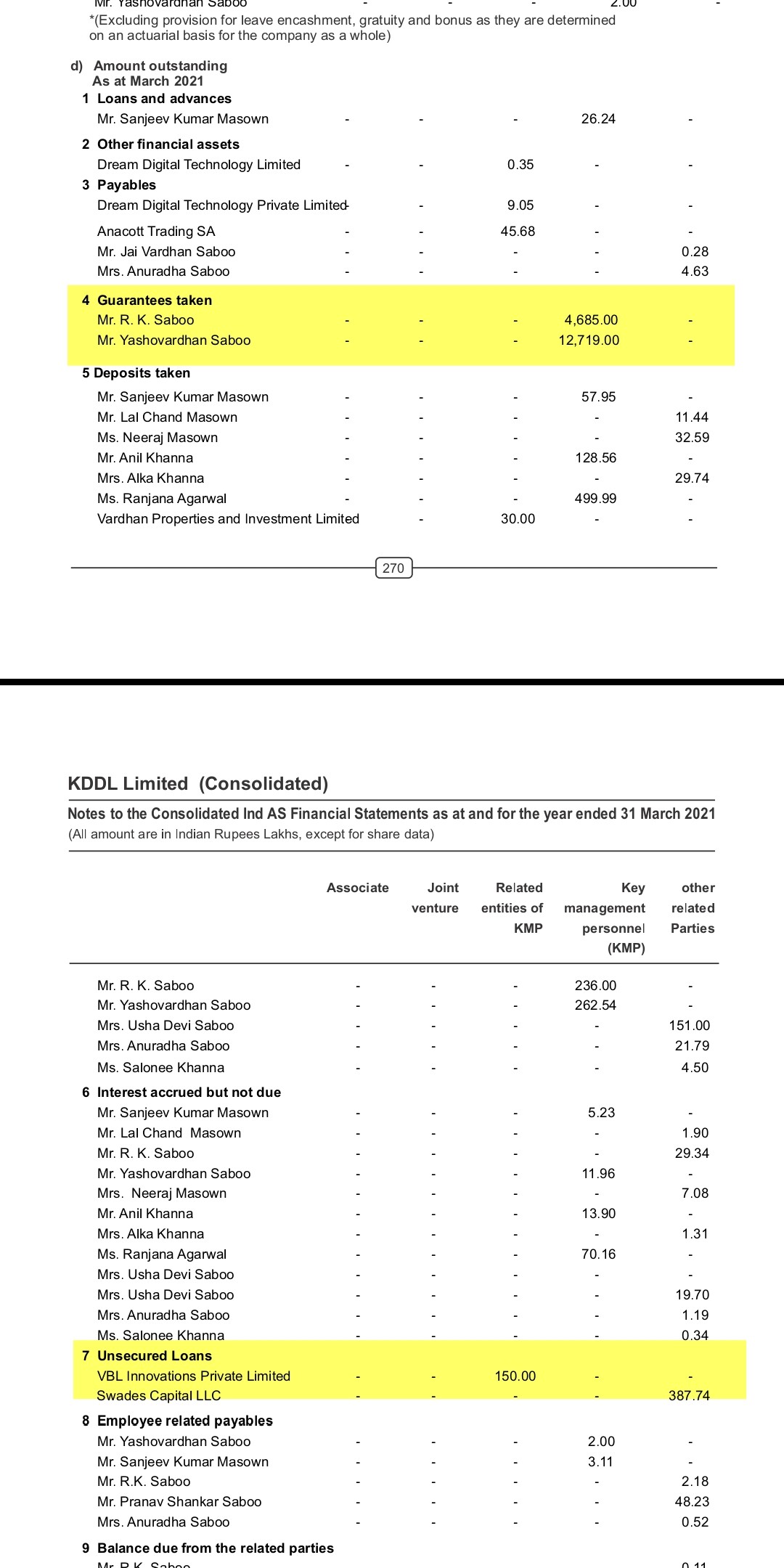

company has been listed for over a decade and governance track record is very good. given that it is a promoter driven company and lot of promoters in management there are related party transactions… but transactions are not significant

Not all related party txns are the same. The management has personally guaranteed close to 170cr in debt. That’s actually a good thing.

Bankers often ask small companies to do so. My guess is that the need for PG will go away after the ipo. The corporate governance record of this company is quite stellar.

–Our Model is omni-channel --its combination of online & offline. The leads which start online and get converted are typically 33/35%

–During Covid, it jumped to 40% but currently its as mentioned above. There is no margin difference between online & offline as our terms are the same

–Demand in the 2nd Qtr has been robust in a seasonally weak Qtr & Q3 is our highest Qtr

–Overall Revenue for FY23 --Start of the Year the growth tgt was 25% and then it was upped to 35% & now what ? --We are still looking at the same growth with demand which has developed in the last 2/3 yrs. The mkt is very strong.

–They have 50 Stores in 17 Cities

–Mkt share of 13% in premium & luxury watch mkt in India

–No. of stores ? --Lot of store openings depend on Malls , we hope to open 8 to 9 stores in this FY23 , we are starting fit-outs and most of them will be operational in Q4. Over next 3 yrs we hope to expand by about 35 stores , this includes stores in 9 or 10 new cities & also increasing presence in Metros and smaller Metros

–Avg. selling price is 1.6Lakhs.

–Pre-owned revenues of 75 Crs & tgt this year to cross 120 Cr in FY23, it is a fast growing mkt. Selling pre-owned watches with credibility means setting certifying the watches and making sure that refurbishment is superb and this depends on the skills of qualified watchmakers which we are constantly upgrading.

–Exclusive brands we have added 2 & before Year end we will add 2 or 3 more.

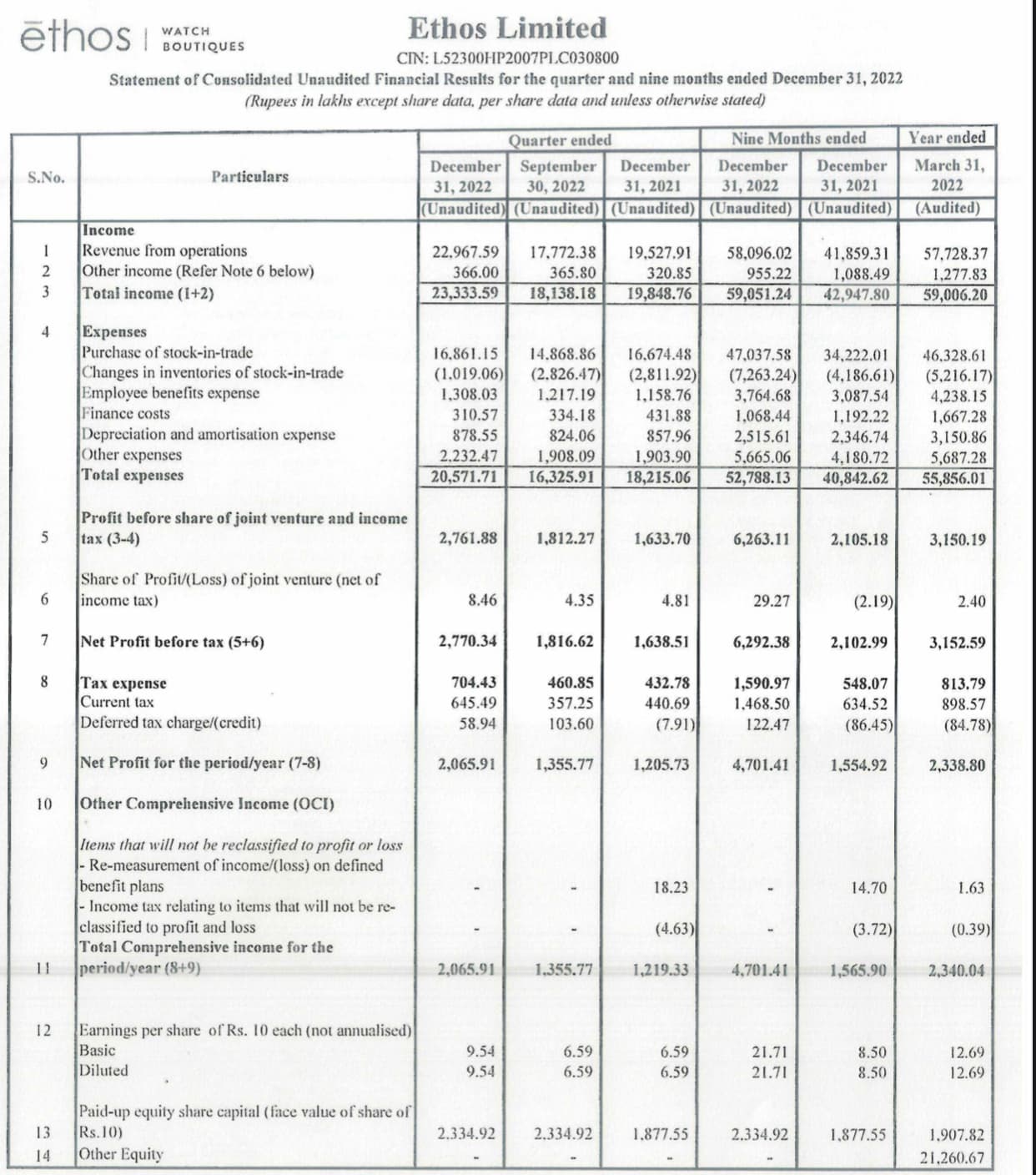

Concall summary for Q3FY23

1. EBITDA margin - 9M at 12.8%(7.9%), Q3 at 13.5%(10.7%), improved 150 basis points QoQ

2. GM - 9M at 31.5 vs 28.3, Q3 31% vs 29%

3. Exclusive brands - 39 @ 27% of total stores for 9M.

4. 5% growth in ASP in 9MFY23 vs FY22.

5. Repeat customers at ATH @46%

6. 50 stores operational.

7. SSG at 16% for Q3 and 31% for 9M

8. Margin expansion owing to inhouse brands. This expansion is despite the extra 2cr spent on hosting GPHG event. Its sustainable and should be increasing in future. Levers for expansion

a. Operating leverage

b. Exclusive brands because they get the distribution and retail margins

c. Reducing discounts

9. Entered in to exclusive agreement with Bell & Ross, Speake-Marin, Trilobe, and German watch brand Tutima.

10. Bell & Ross was already present in India but decided to work exclusively with Ethos.

11. New brands have a certain gestation period too.

12. Opened new store in Indore and Bangalore.

13. Exports business of Swiss watches reached all time high of 24.8Bn Swiss francs. Main contribution from precious metal watches

14. Export of Swiss watches to India went from 156.8 to 187.6 Mn Swiss francs (19.6% YoY) vs 97Mn in 2020.

15. On time to open 40 stores in next 24 months. Location for next 12 months already signed up.

16. Don’t see any demand issue as of now. (Even Ferrari sees good prospects). Although there were supply chain issue which affected CPO.

17. CPO -

a. 1le digit growth in CPO bcs of supply chain issues. So might miss target of 70cr in FY23.

b. For CPO Q4 should see 70% YoY growth. Next year should see 100% over FY24.

c. Opening large service centre which should be operational in next 4 months.

d. Expect

e. Move to consignment models.

i. Q4FY23 - 30% sales through consignment model

ii. FY24 - 50% sales through consignment model

iii. FY25 - 85% sales through consignment model

iv. This will improve ROCE

v. Expect billing of about 100cr in FY24

18. Stores start breaking in the 1st year and have a 3 year payback period. If store doesn’t start meeting targets within 2-2.5 years then management starts looking at the viability seriously.

19. Store in Indore opened in December is already profitable in January.

20. Will be willing to undercut retailers for existing brands as long as ROC is strong like more than 25%.

21. Inventory days at 156days vs 160 QoQ.

22. Rimowa (from LVMH group) store in Jio Plaza may start from May June. In terms of scale won’t move the scale for maybe 2 years.

23. This year there would be 20 brands which create products designed be ethos. Example - Loius Monet hasi a whole collection exclusively for Ethos, in talks with RADO (which is not event an exclusive brand) for an exclusive timepiece .

“Silvercity Brands AG is a Switzerland based watch company which was incorporated on 6th March 2023”. Don’t understand why did they buy a company incorporated just a few weeks back?

Couldn’t find much on the acquiree except that it’s into leasing of intangible.

“On the same address as Silvercity Brands AG there are 2 other active companies registered. These include: Estima AG, PYLANIA AG.”

Interestingly both these companies are owned by KDDL