This story seems very interesting to me.

@mikaarun - Your numbers for FY15 matched the actual numbers almost eerily and also the pics/graphs in the KDDL investor presentation and yours. I’m assuming you just pulled the data from their investor presentation from last year. Started having integrity doubts there for a second!

So I was going through the results PDF of KDDL which also has the investor presentation slides. Need help from you guys to understand a couple of aspects :-

-

EBITDA margins for ETHOS have been alternating up & down every year - 9.2%,8.8%,9.6%,8.9%,9.6% from FY11-15.

Since the rate of branch expansion will be a lot lesser going forward, I’m assuming the EBITDA margins should start moving in only one direction from next year - up that is! Your thoughts??? -

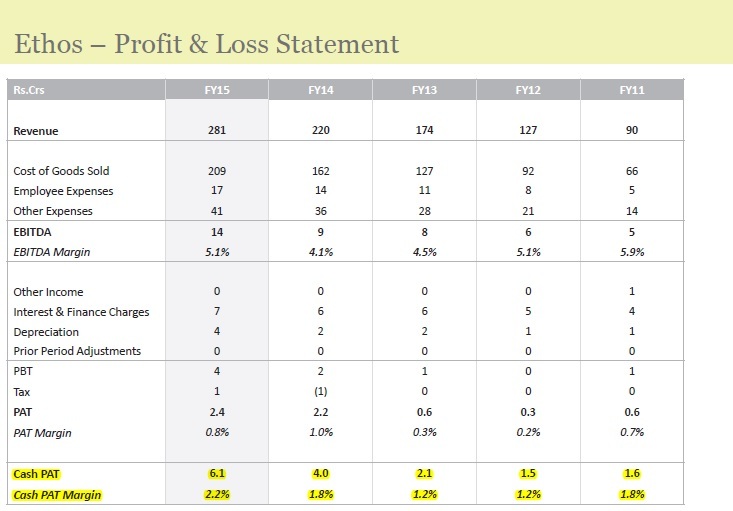

Looking at Ethos P&L - There is a line item for Cash PAT!

What is Cash Profit after Tax? How is it calculated? Cash PAT was 6.1 crores and PAT is 2.4 crores?

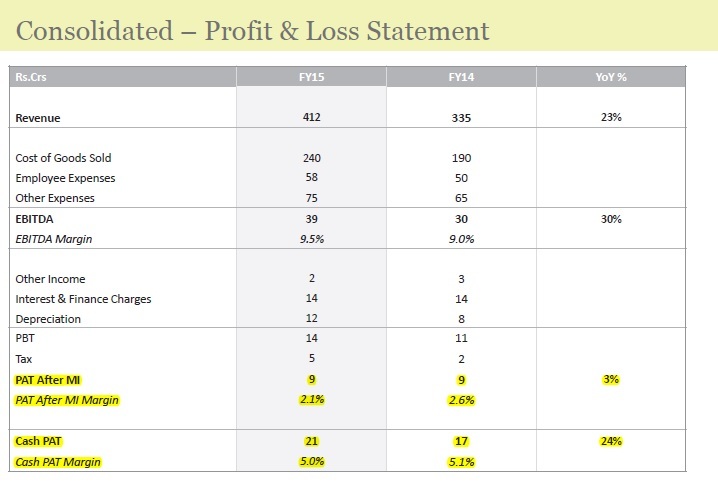

- Looking at Consolidated P&L - There is a line item for PAT after MI and Cash PAT!

Can anyone explain what is the difference between PAT and PAT MI? How is Cash PAT being calculated?

"

Ok - so moving to a couple of things discussed earlier in the thread.

-

Future Outlook of luxury watches -

With India’s every growing upper middle class and HNIs, Ethos should be best positioned (offline/online model) to capture their share of wallet every time they look to buy an expensive watch. Owing to the current market size (I dare say which will grow handsomely in the next few years), growth in luxury watch sales over the next few years should not be much of a concern. Whether KDDL is best positioned to capture this is the bigger question that needs to be answered? -

The threat of smart watches - my opinion

Simple question - Which phone do the elite or ultra rich generally use? Which phone does their entire family use? Most affluent HNIs would be using the iPhone and upgrading it every year / 2 years. (Offtrack but important to stress the point - Our PM used an iPhone to take his selfie with the Chinese PM). My thinking is there will be a mad rush for people to get their hands on the 1st iWatch as a status symbol.

And then… there will be disappointment. It usually takes a couple of iterations (years) before Apple starts getting the product right based on new technology, innovations and customer feedback.

But sooner rather than later - a lot of these people will be buying an Apple watch as it would make their lives easier with the same eco-system and usefulness of these devices.

Just yesterday, Google presented a host of new stuff for Android Wear and the future looks very exciting for smart watches. However, that time is still a few years away according to me.

So if the rich start buying the smart watches, where does it leave KDDL? The smart watches would ideally be their day-to-day/fitness tracking/swimming/fun events watch where they don’t need to be wearing a luxury watch worth > Rs 1-2 lacs. They will always be showing off their Rolex/Omegas/Cartiers at major functions/parties.

But it would start eating away at the wallet share for KDDL. If they’re going to upgrade to a new iWatch every year as well, they may not buy those <50k watches they used to buy earlier.

Don’t know but smart watches may just divide the market into 2 distinct segments

- Smart watches ( <60 k) As these devices may be a lot more useful for the middle class going forward. How much will that hurt KDDL? How much market share will they lose?

- Luxury watches (> 1 Lakh)

It may take some time, 1/2/3 years but smart watches are here to stay and there’s no denying that!

However, my take is there is still a tremendous scope for growth in the luxury segment watches in India which can be compared with jewellery for women (diamonds, gold) and these may never go out of fashion.

1 Main Question - How much share of the luxury watch pie can KDDL garner over the next 5 years? Assuming honest management and effective operations.

- Initiated tracking position .7% of portfolio (Looking to add a lot more)

to one of my friend! Also, the repair costs are quite high. But I guess, once business matures, these problems can be resolved.

to one of my friend! Also, the repair costs are quite high. But I guess, once business matures, these problems can be resolved.