There is no sand available for construction in Andhra Pradesh as the government was finalising the sand disbursement process. This may be one of reason.

What is ebita per tonne from last three q s

Any help on this parameter

1 Like

At a joint review meeting held by Andhra Pradesh Chief Minister Y.S. Jagan Mohan Reddy on Monday at Vijayawada, he had asked the cement majors to supply cement in huge quantities for various government’s affordable housing projects.He also informed them that his State required over one million tonnes per month for various projects, including one for affordable housing and that the cement should be supplied at lower prices.

The meeting was attended by representatives of India Cements, Ramco Cements, KCP, Ultratech and JSW, among others.

4 Likes

I went through the last 3 Annual Reports with the aim to glean the qualitative aspects of the business and promoters. I am sharing my notes per business segment with the hope that it will generate some discussion and feedback to help build conviction.

KCP_AR notes_202003.xlsx (13.3 KB)

Some questions I am still searching answers to:

- Why did the company embark on Cement capacity addition (2 to 4 MTPA)? South region where company operates has surplus supply and consequently lowest capacity utilization across India (~55% vs. pan-India ~75%). Also reflected in growing volumes but declining realization over last 3 years.

- What is the remaining useful life of their limestone reserves? MD in her opening note in AR FY18 mentions “our depleting limestone reserves”. AR FY19 states that company is “initiating the process for participating in auctions with a view to securing new mining leases for its existing plants as well as for its expansions at different locations”

- What are/will be the cost implications of securing limestone mine via auction? Some hints avlb. here: Will high auction prices of limestone affect margins of cement makers? - The Hindu BusinessLine

- How severe is the KMP risk? With Mr. VL Dutt’s death in Feb 2020, are current MD and Joint MD (wife and daughter, respectively) able to steer the business to success?

- Is the company a likely acquisition target for larger players such as UltraTech, Ramco or Shree Cements?

10 yr P&L (source: screener.in)

| Item | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Trailing |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 643.22 | 658.72 | 1,016.31 | 1,136.14 | 1,060.58 | 1,187.68 | 1,296.00 | 1,230.72 | 1,475.92 | 1,660.57 | 1,481.34 |

| Expenses | 481.34 | 522.08 | 824.46 | 1,024.96 | 933.52 | 1,020.10 | 1,032.62 | 1,010.71 | 1,219.69 | 1,429.64 | 1,278.72 |

| Operating Profit | 161.88 | 136.64 | 191.85 | 111.18 | 127.06 | 167.58 | 263.38 | 220.01 | 256.23 | 230.93 | 202.62 |

| Other Income | 11.13 | 16.25 | 44.38 | 75.97 | 20.60 | 12.60 | 4.49 | 9.47 | 1.79 | 8.70 | 9.15 |

| Depreciation | 21.67 | 22.33 | 41.04 | 44.42 | 47.13 | 48.21 | 48.29 | 62.59 | 70.51 | 75.62 | 87.81 |

| Interest | 13.36 | 15.65 | 41.53 | 39.71 | 46.31 | 51.46 | 52.34 | 50.79 | 44.78 | 40.45 | 56.64 |

| Profit before tax | 137.98 | 114.91 | 153.66 | 103.02 | 54.22 | 80.51 | 167.24 | 116.10 | 142.73 | 123.56 | 67.32 |

| Tax | 32.37 | 18.91 | 26.15 | 17.98 | 4.30 | 13.05 | 49.78 | 19.48 | 31.11 | 15.29 | -2.80 |

| Net profit | 90.76 | 78.75 | 106.05 | 65.24 | 34.49 | 50.37 | 93.35 | 76.55 | 89.52 | 82.22 | 50.58 |

| EPS | 7.04 | 6.11 | 8.22 | 5.06 | 2.67 | 3.91 | 7.24 | 5.94 | 6.94 | 6.37 | 3.92 |

| Price to earning | 4.17 | 4.16 | 3.93 | 5.64 | 12.51 | 15.13 | 11.44 | 17.47 | 18.76 | 13.76 | 10.22 |

| Price | 29.36 | 25.40 | 32.35 | 28.55 | 33.45 | 59.10 | 82.80 | 103.70 | 130.20 | 87.70 | 40.10 |

3 Likes

Kcp last year (2019-20)cement capacity utilasation was 42%…This yr they are hopeful of achieving above 50%.

In next 2 yrs if the cycle of cement turns which i feel is most likely then they can do atleast 70% capacity utilisation which means approx 3mtpa of cement division so turnover of cement division alone can easily touch 1350 crore with ebit of 200 crore & np of 120 crore + all other businesses sugar engineering hotel.

I see minimum eps of 12-15 in next 2 to 3 yrs once the cement cycle turns, one needs to hold with patience to enjoy the benefit of 3x to 4x from current levels.

Also they have 74 acre of land in north chennai with bare minimum 2000 rs price per sqfeet one can value it at 700 crore only for the land.

I see not much downside but huge upside.

75 yr old company

Honest conservative management

Disc : Holding since 1 yr and also added in current fall

8 Likes

1 Like

As the coal prices have reversed to mean, cements is one sector which looks vert very interesting to me. Came in my scanner after tracking G Parikh sir’s transactions.

Added mostly on the P/B of 1 and planning to exit at P/B of 2+ ! The leverage should come in play now as freight costs are gone and the stocks should go reverse to mean with an uptick demand in the Infrastructure spend.

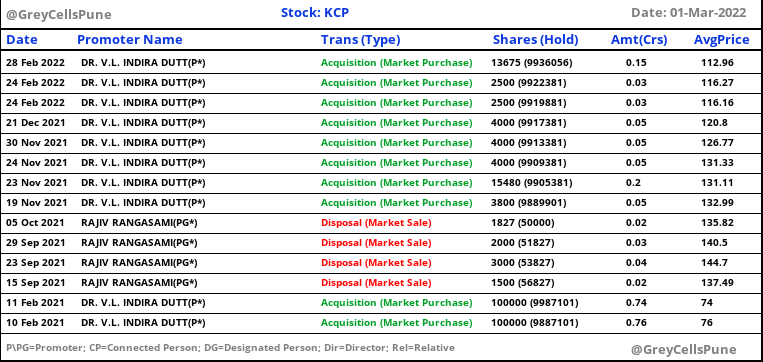

Promoter buying is happening every month !

2 Likes

How does KCP look now?

1 Like

https://www.bseindia.com/xml-data/corpfiling/AttachLive/45d9288c-e054-44f2-bc66-8fca3d0abb2c.pdf Recent announcement by Co.

The company’s Heavy Engineering division has recently made a filing which shows they have been working with ISRO from past 3 decades and I am not very optimistic on this as its a B2G.

They should spin it off as per my views along with the Hotel business as both are non-core.

Coming to the core Cement business, they are mostly based out in AP and TS and both the states should experience heavy Infra development which may result in benefiting it. I have positioned myself with enough MoS to cover the downside risk. Let’s see if they start receiving more orders which may cater to the defence as well then it may become a candy to the market.

Disc : Invested and Biased.

4 Likes

KCP is planning to double cement capacity in AP. With Chandra Babu Naidu now at a good bargaining position in NDA, this should benefit infra sector in capital of AP and thereby KCP. Stock is not expensive, is seeing accumulation on charts. Disc: Invested today

hello

Cement : margins quite low reduction in energy prices would help , yes expansion to

AP is a good trigger in Long term , also it would be interesting to understand completion for Railway Siding Project along with Input Material Handling

Equipment and System & Cement Grinding Hydraulic Roller Press at Muktyala, NTR District, Andhra Pradesh.

Sugar : Business based in Vietnam seems stable unsure of growth here : only cash cow segment for the company

Engineering : Very miniscule Business - Loss making : would love to see more action on scaling up here : Asset turnover ratio is Poor

Hotel : Profitable - do not see any expansion here

All Business put together Churned Cash 100 cr +

Invested for tracking Qty & would closely observe developments on AP

Thanks for sharing ur views. They released a business update few weeks back on engineering business. Plans to focus on supplies to space mission.

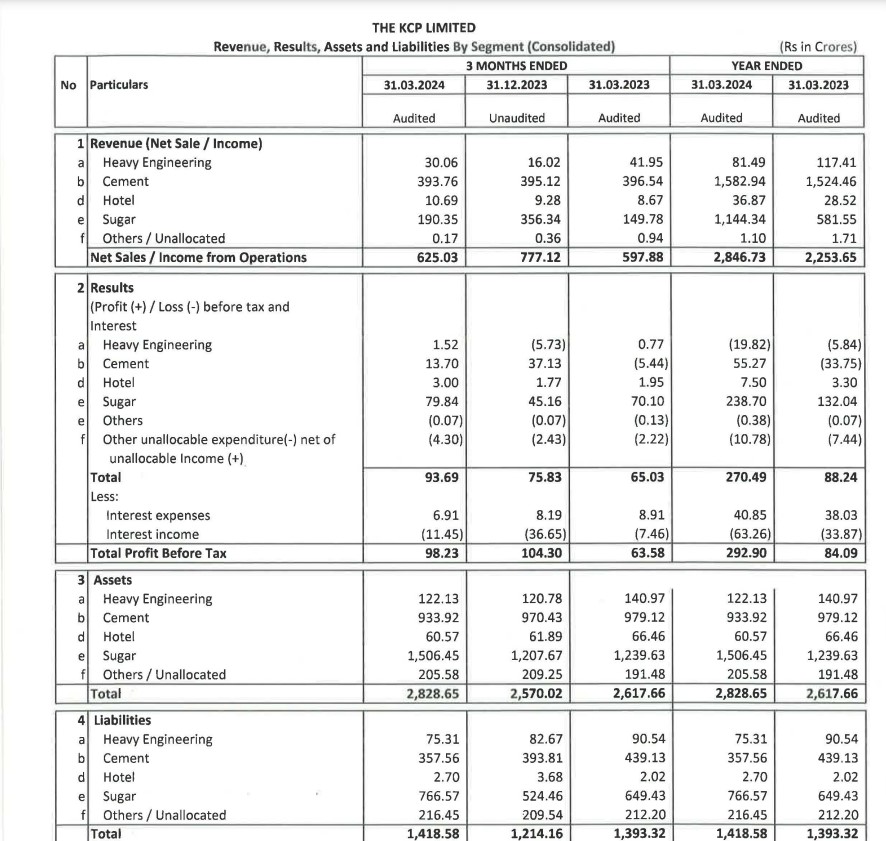

Cement margins are poor. Need to understand the reasons. Pls share if someone knows the same

1 Like

Mcap currently is 2700 crs & cash in books in 700 crs approx. Whenever cement margins revive, EPS will look more attractive, currently on TTM basis it is trading at 12 PE.