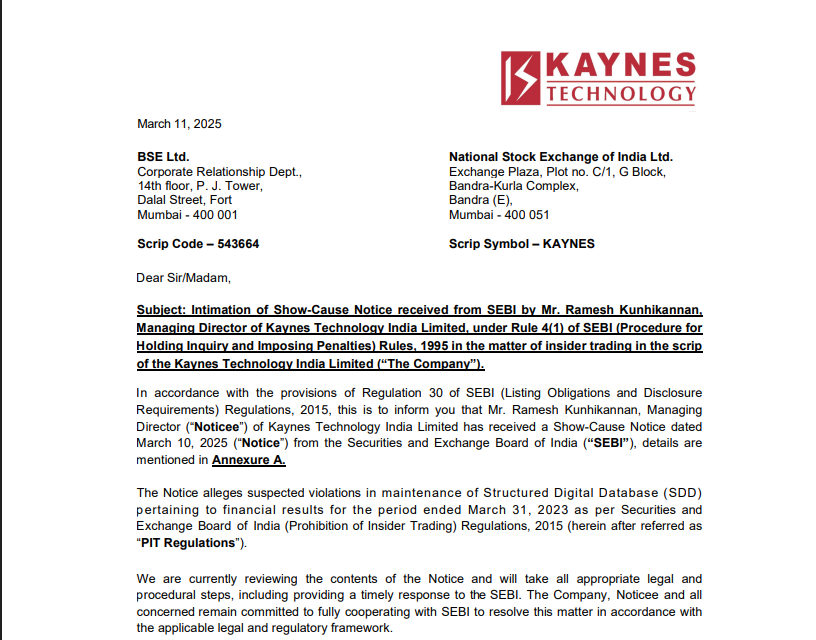

SEBI has issued a Show-Cause Notice (SCN) to Mr. Ramesh Kunhikannan, the Managing Director of Kaynes Technology, regarding alleged violations of insider trading regulations.

The notice does not confirm wrongdoing yet, but seeks an explanation from the MD before SEBI decides on further action.

•Clear strategy to become an integrated global ESDM player.

•Expanding into HDI PCBs and OSAT (semiconductor packaging) — huge opportunity given India’s focus on electronics localization.|

•Consistent focus on high-margin ODM and IoT products.

•Revenue expected to compound 20–25% CAGR over the next 3 years.

Disclaimer: Invested

Kaynes results were good. At 60% growth guidance, with mgmt affirming revenues to come from semiconductors (osat) in fy27, seems like a structural growth story for the years to come. Finance and depreciation costs to remain elevated as they have to build capacities for global customers to believe in their ability to execute. Receivable days were higher due to high receivables from one of their acquisitions. Valuation remains high but seems cheap if we consider 40-50% growth for next 2-3 years. Negative cash flows remain a concern, due to high inventory and receivables pileup.

Bhai - I was invested from lower levels and had done an exit after Q3. Something strange happened here:

I guess a week before the management came on TV and said that they will surprise on the upside while the price was falling. In Q3 they missed their guidance and said some projects saw delays. As the delays were not anticipated when they came on TV, a general assumption is that the delayed work will push in Q4. Management revised FY25 revenue downwards.

Q4 results were normal Q4 seen for this company but with margin expansion - it did not have any additional revenue to meet even the lower end of the revised guidance. So they fell short on their overall FY25 guidance.

For FY26, they maintained the same growth % number, however now with a lower base - so effectively they reduced their guidance for FY25 and beyond with a twist they said margins will see an upside. Generally when the results are to come good, price will start telling the story in advance. Since they declared their results, stock price is on a downward trajectory - and in between came surprise when management sold stake - surprisingly the buyers seems to have bought in small quantities - else their names would have been reported along with the seller names.

I would stay cautious on this counter till management delivers what they project.

1600 crores QIP has been successfully placed at Rs.5569.5 and gave discount of only 1%, it appears there was strong appetite for the shares across well known DIIs (hopefully for the long term).

After reviewing the management’s interview regarding the resignation, the responses appear unconvincing. While the interviewers did an excellent job of trying to get more details, the management’s answers were often not specific, relying on unnecessary details that felt like fillers.

This situation invites further discussion. Do others share this view of the management’s response, or does anyone have any additional information or “scuttlebutt” to provide context on this departure?

disc: I hold a small position, trying to make a decision given the development.

I listened to the interview.

My take is , the company is expanding futuristic semicon business and requires new expertise to lead the business vertical. They appear to be creating few more CEO position to head each vertical and this must be diluting Mr Rajesh position in the company and consequently he wud hv put in his papers. As Sampath pointed out and I am also agreeing with him that Rajesh might not be the sole person responsible for the stupendous and phenomenal growth, the company had so far.

Their future success depends upon how their Semicon business is going to perform,

I am with the company from IPO stage and On and Off due to valuation scare. But I must admit that their success is consistent and above the Industry peers.

Discl: Invested and wish to monitor their future performance to take a call.

H1 Cash flows statement says something different!

Debtors & inventory build-up is significant and the company has not given a comparison against the H1 FY25, this time. Receivables /debtors is 1100 crs against sales of 900 crs.

Focus on Gallium Nitride (GaN) technology for advanced electronics.

R&D team of 200+ engineers driving new product development and innovation.

Industry Outlook (Opportunities & Tailwinds)

Global ESDM industry expected to grow at ~5.2% CAGR (CY23–CY27).

PCB market in India projected to grow from USD 6.3B (2024) to USD 24.7B (2033) – CAGR 15.6%.

Strong policy tailwinds via PLI scheme, Make in India, and semiconductor mission.

Growing demand from EVs, 5G, consumer electronics, and industrial automation.

Current Challenges

Working capital stretch (NWC days up from 108 to 116).

Inventory buildup and higher receivables as company scales up capacity.

Execution risks linked to rapid expansion in OSAT/PCB and global operations.

Industry-wide competition and need for continual technology upgradation.

Dependence on global semiconductor supply chains, though localization efforts are underway.

Key Takeaways

Strong financial momentum with double-digit growth in all metrics.

Moving from EMS player → Fully integrated ESDM & semiconductor ecosystem player.

Large capex in OSAT and PCB verticals to enable future scalability.

Well-diversified across customers, verticals, and geographies.

Positioned to benefit from India’s ESDM and semiconductor growth wave.

The allegations against Motilal Oswal are very serious. I have not invested in Motilal Oswal, nor am I connected with it in any way. I have bought some shares of Kaynes Technology on the 27th of Nov, 2025. At that time I was not aware of the reports.

The above disclaimer is necessary because I find it diffcult to believe that a reputed company like Motilal Oswal would indulge in such sculduggery. As the video suggests there were allegations earlier involving Kalyan too, Motilal Oswal (the company) would have to be really brazen to indulge in such an act. More so, whenever we have heard of such mischief, it has been indulged in by recommending the stock in the open and trying to secretly sell it.

Such a thing is hardly possible for a company like Motilal Oswal, as any bulk deals are reported the same day.

Incidentally, ICICIDirect also came up with a report, the very next day after Motilal Oswal. Would it seem possible that two such large institutions would act in cahoots, knowing it would be so easy to put two+two together.

I have not read the reports, but I strongly believe that without knowing I may have made a great investment because the share had got slapped down just after good results.