My notes from the conference call today. Sorry if there is any duplication.

Situation:

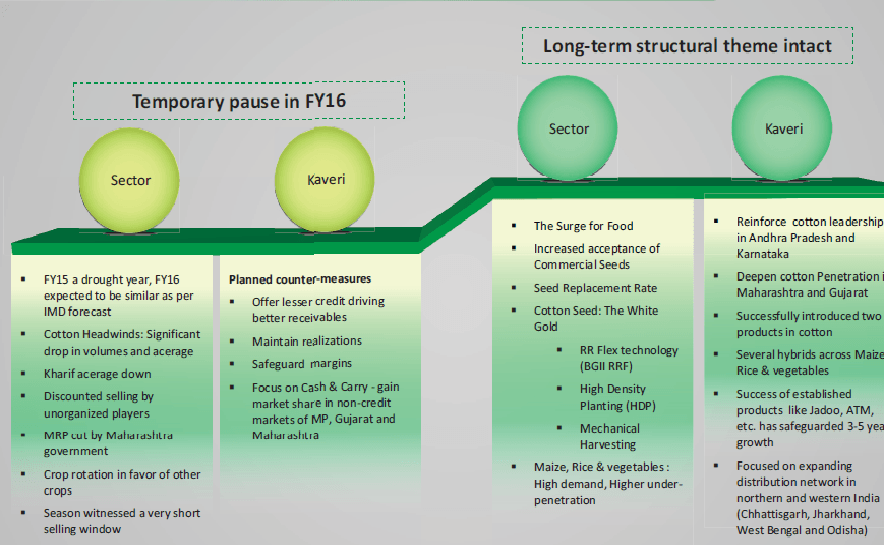

Two back to back draught years.

Revenue decrease because of decrease in acreage, discount selling, MRP limit, crop shifting to pulses, soya etc.

Volumes moderated due to low acreages.

Market share 15-16%

Cash and cash equivalents 350 crores (30th June 2015)

Managed well in terms of receivables as two back to back draught years have high impact on receivables. Strategic decision not to supply to credit markets (Telengana) and rather focus on cash markets. As a result volumes are down in credit market. Couldn’t place the stock in advance at distributor/dealer level.

Demand of brand is very good. Acceptance in farming community is very good.

Most of the cotton areas are affected by drought, decided not to go with credit markets. 6-8% acreage reduction, 18-20% volumes reduction

5-6 L packets volume loss in MH as company did not participate during peak season.

Cotton Sales this quarter:

Volume: 54 L packets

Value: 480 crs

Total sales:

Last year 85L packets . Total market 5.3-5.4 crs

This year estimate 60-62L packets

Credit market Telengana, 7-8 lakhs packets this quarter as compared to 16L packets last year quarter.

High growth of ATM in Maharashtra from 3.5 L last year to 7 L this year.

Corn:

Strong 25-30% market share in Andhra

Grown in MH where our presence is low

20% down by sales in Andhra

Overall market is down more than 35%

Hybrid paddy: Grown more than 20-25% market share. Chattisgarh/U.P.

Sales Q1 FY16 Q1 FY15

Maize 65 crs 71 crs

Overall paddy 74 crs 68 crs

Hybrid paddy 45 crs 38 crs

Net inventory 1.1 cr left out and fresh inventory.

Next year sales target 90 L packets.

Production cost – no increase as compared to last year.

No decline in inventory YoY.

Increase in market share:

Adibabad, Warangal, Maharashtra, Gujarat (growth more than 70%)

Guntur – shifted to chilly this year

Riasima 40-45% acreage down

Royalty payment:

States INR

Maharashtra 20

Andhra and Telengana 50

Other states 90

North India states 180

Total effect 64 crs (including taxes). Deduction due to lower royalty, not in balance sheet no contingency. Royalty payments in the month of June-August

What if worst of both scenario

- Forced to pay royalty to Monsanto

- Forced to settle at low MRP

Very low probability however risk remains

Realizations:

Overall realization INR 880-900

Net realization INR 790-800

Likely to gain market share next year

Maharashtra MRP INR 830, other states MRP INR 930

North India, billing close to INR 1000 (due to high royalty)

Different packing next year for MH

Market situation:

Branded players are affected who have not supplied to credit markets. Unorganized players gained market share in credit market however they may have big issues with recovery if drought situation persists longer. Nuziveedu actively participated in credit market this year.

Maharashtra, MP : branded players have gained

Cotton acreages:

Cash markets (Maharashtra, Karnataka, Riasima) – Down

Credit market (Telengana) – Up

Strategy:

Focus on increasing the realizations

No higher discount to distributors/dealers this year

Focus more on credit market next year. Comfortable on competing credit next year.

International markets entry

Indonesia for Maize & Rice

Africa for Maize & Cotton

May take 2-3 years