IMHO the Management has been extremely conservative in the past. A new management has taken charge in the recent past and they have announced avenues for revenue growth and have also taken action in some of those avenues. For detaills, please refer to their recent Earnings Call. If those measures frcutify, the market may reward the bank with a rerating of the PE. Everything depends on the success of the initiatives annunced. Disclosure: Invested. My views are biased.

1 Like

Key points to watch out

- Expansion into other states: They have a stated position of a 50:50 branch mix between Karnataka and other states

- Efficient deployment of the recent capital raise program

- Improvements in technology infrastructure and revamped org structure (dedicated segment leader roles for Retail, MSME)

- Trajectory of historical NPAs and how its coming down

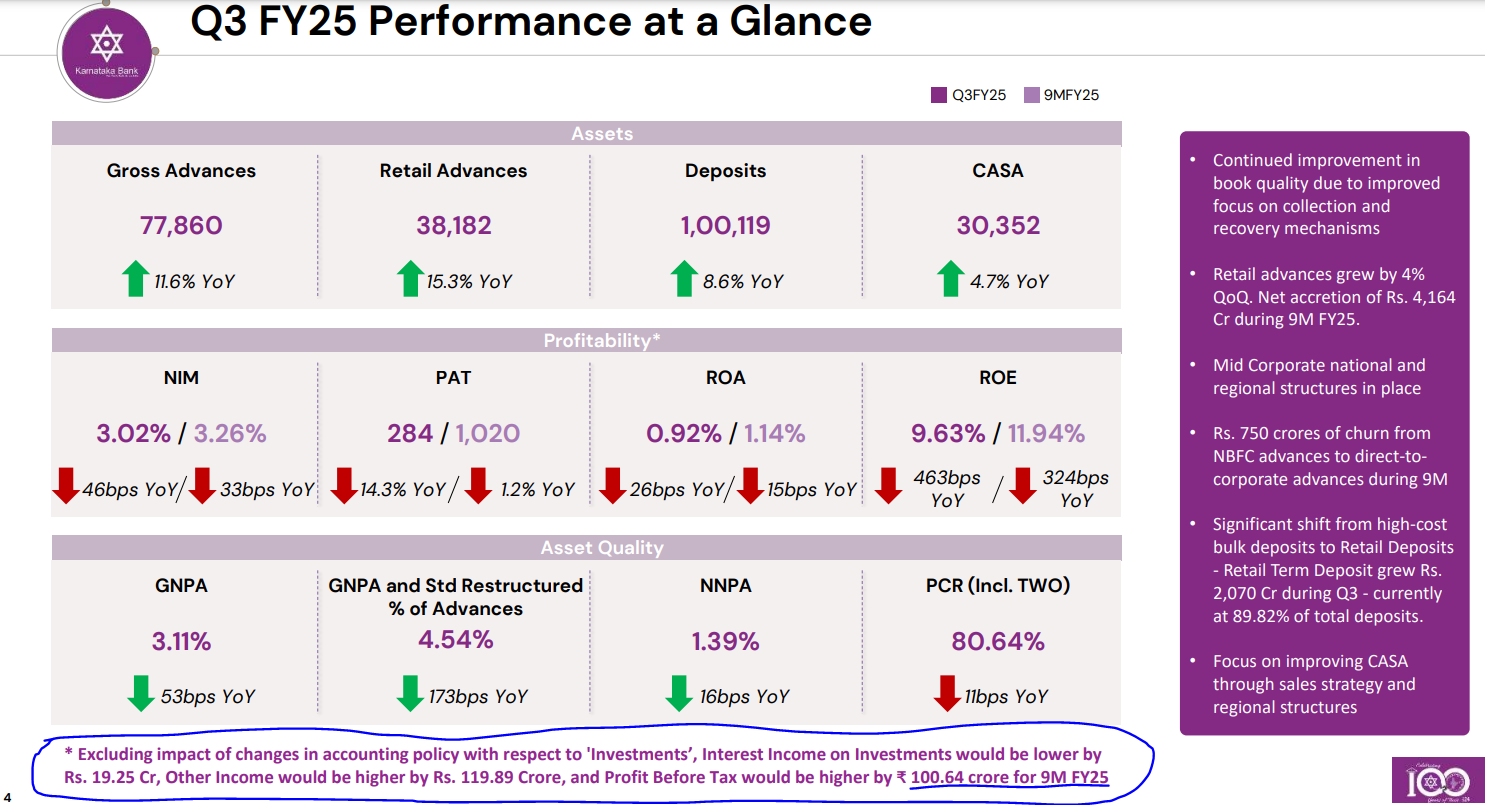

- 1,00,000 Cr advances by FY26 from current of 75,000 Cr

Disc: Invested.

2 Likes

https://d3sdkw7nvdnqts.cloudfront.net/s3fs-public/2025-01/10029159compressed.mp3

My thoughts on Q3 results/concall:

Overall, disappointing results, though they have made some progress with lower slippage ratio, GNPA and NNPA, yields remain low and CoB high. CI is higher despite Management saying it was one off last quarter

I agree that management had said the structural changes(granular focus on RAM, reducing high cost bulk deposit and low yield advances) will take time, it’s been close to 2 years since new management is in place without significant improvements in metrics that investors care about (RoA,ROE)

Also don’t like the fact that management try to conceal issues where they conveniently choose to highlight improvement in QoQ performance and then revert to YoY/9M for parameters that have deteriorated(eg CI higher in Q3)

They have said Q4 is traditionally the best quarter and hoping it turns out to be so.

Overall may change my investment thesis after reviewing Q4 results as without improvement in metrics that matter to investors this may continue to be a value trap (around 0.6 PBV, dividend yield of 3%)

Would like to hear fellow members views on the same.

Disclosure: invested (hoping that I’ve been unbiased in my views ![]() )

)

4 Likes

One basic question.

I agree the stock can disappoint investor who expect this to get rerated to P/B of 1.2 to 1.5, thereby making 25%+ CAGR for next 4 yr.

But at adjusted P/B=0.64 and worst case RoE of 11%, why this stock need to be considered a value trap even if metrics remains same. Annual return of 14% CAGR (including 3% dividend yield) looks easily gettable.

Stock looks like a dhandoo investment now (Heads i win, tail i dont loose).

5 Likes

The thinking outlined by you are exactly the reasons i invested the stock in the first place ![]()

Last quarter RoE was sub 10% (exact figures available in the investor presentation)

The issue is Mr Market has been valuing the stock at average PB of 0.5 or lower and PE of sub 5 over extended period (source Screener) , now without significant improvement in the metrics and growth no reason for it to expand.

All things being the same, would be picking up even more stake at these lower levels if management was more transparent and delivering on stated goals. That clearly hasn’t happened and until it does my feeling is market won’t be excited by it.

4 Likes

The biggest issue i see here is that they are not able to garner market share and in fact they lost deposit market share. Every bank that looses deposit market share is weakest when it comes to customer preference and cant create wealth.

2 Likes

Yes. RoE of 9.64% is alarming low considering the fact that TMB and SIB made 14% this quarter. Now these 2 stocks that trades at P/B=0.8 are cheaper than karnataka bank.

2 Likes

I am not concerned by this one time Accounting affect as much as i am concerned by loss in Market Share on deposit Side. Same issue with TMB and SIB. Unless They can garner Deposit market share there is no way it can be a customer franchise.

1 Like

Can you please elaborate a bit…Deposits have grown 8.6%. What do you mean by market share on deposit side? These are 100+ yr old banks. They may not grow customer market share now. If RoE > 14% and NNPA <1.5% & stable for these small banks trading below its book, then its a reasonable investment. Any green shoot can take the stock closer to P/B=1 which can act as alpha.

3 Likes

System Deposit Growth Vs Bank Deposit Growth. System deposit growth (Indian Banking System) is approximately 10% and they are growing at 8.6%. At 0.65 Price to book its not a very bad entry point. But if they aren’t a deposit franchise no point of all of it as they will need to borrow to lend. Borrowing for it will be higher than cost of deposit and hence further ROE reducing.

2 Likes

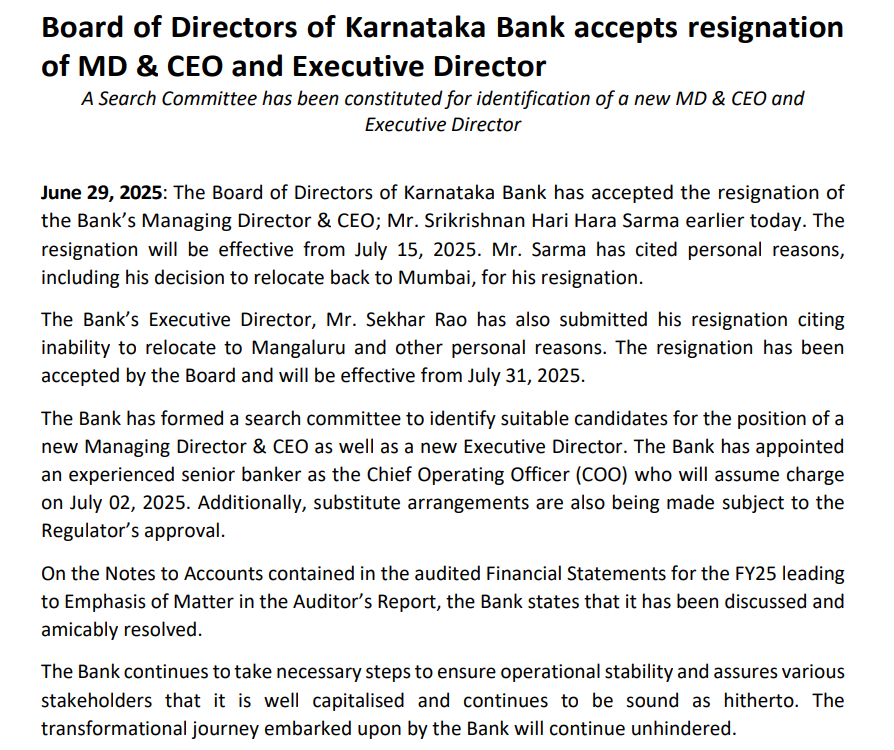

Very disappointed with the result plus the way they answered in concall, exited with minor loss, plus time cost

4 Likes

Very disappointing Q4 results which is usually seasonally the best. Management giving excuses as has become the norm and to top it all of, serious corporate governance issues raised by the auditor and board and pooh-poohed away in concall as “insignificant amount.”

Disclosure:Exited fully, thankfully at break-even price. Learnt some useful lessons along the way ![]()

7 Likes

Personal opinion: Got bored of Current CEOs concall monologues, hopefully we get somehow who leaves more time for questions during concalls.

2 Likes

Q2FY26 concall - few targets to track in upcoming quarters

The C/I ratio is expected to come down to 55% plus in the coming quarters.

The bank has restarted RLPCs (Regional Loan Processing Centers) and empowered regional heads with adequate delegated power (which was previously minimal) to speed up sanctions to grow RAM segments at 16-18%.

NIM - 3% +

1 Like

It feels like current ceo is going back to old ways of running Ktk Bank. Previous CEO, I remember, made a case for centralized decision making to speed up loan approval and as well, improve asset quality. now, current ceo wants to go back to branch managers having control. Well, only time will tell. But one thing I am hoping is that existing employees appreciate current ceo as he is obviously a cultural fit for long term employees and it turns into some real results.

1 Like

Interesting Read…

https://www.businessworld.in/article/shadows-over-karnataka-bank-585914

2 Likes

who is the major investor who might influence their decisions

Most likely it is the quant mutual fund group.

1 Like