me too if possible because there will be valuable insights from company.

Great development for specialized wagon business (in automobile segment) →

Railways has introduced a reform allowing special wagon designs while giving flexibility to the industry. Manufacturers can now design wagons based on specific origin-destination routes with high-capacity.

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2244597®=20&lang=1

10 Likes

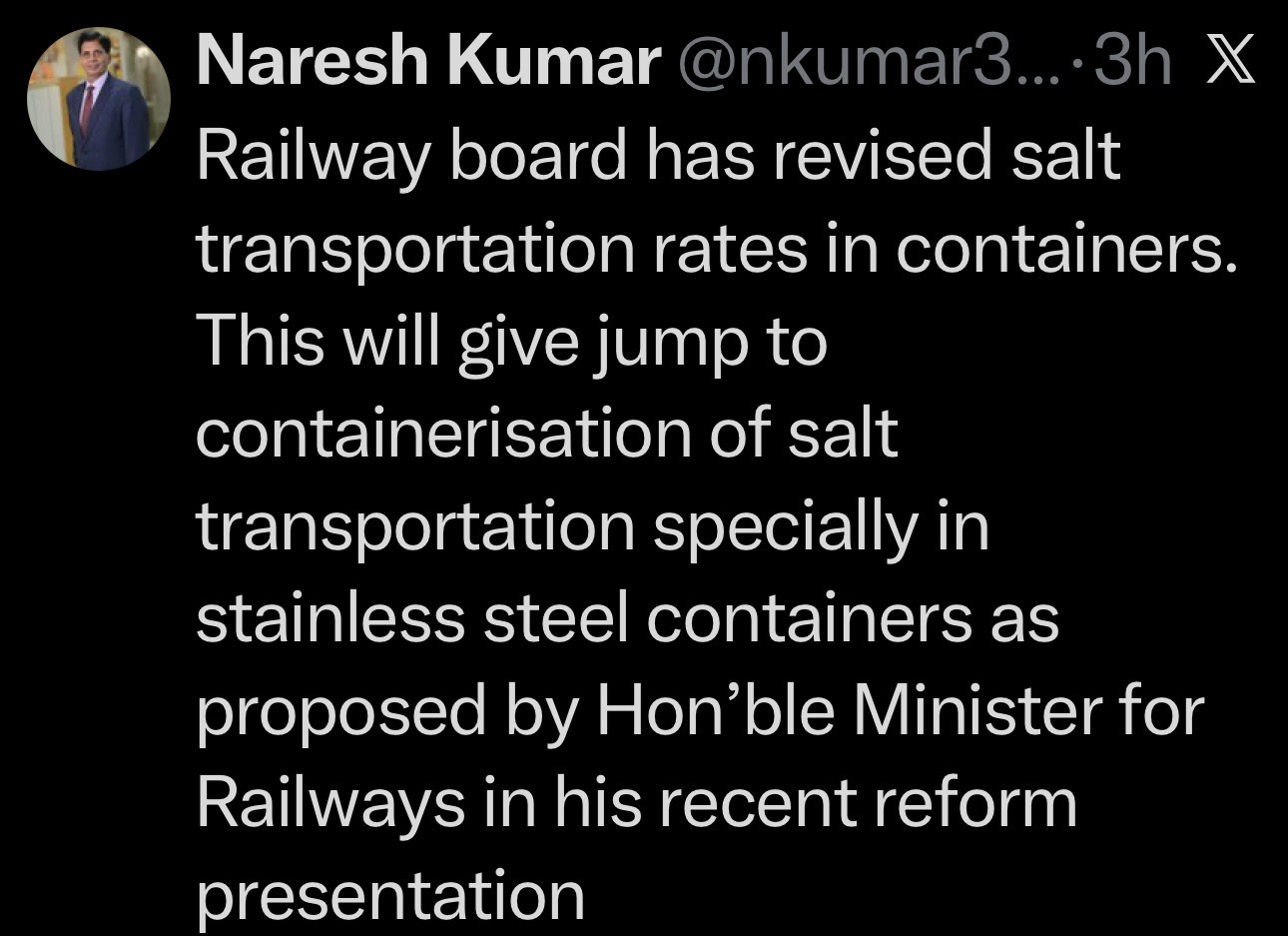

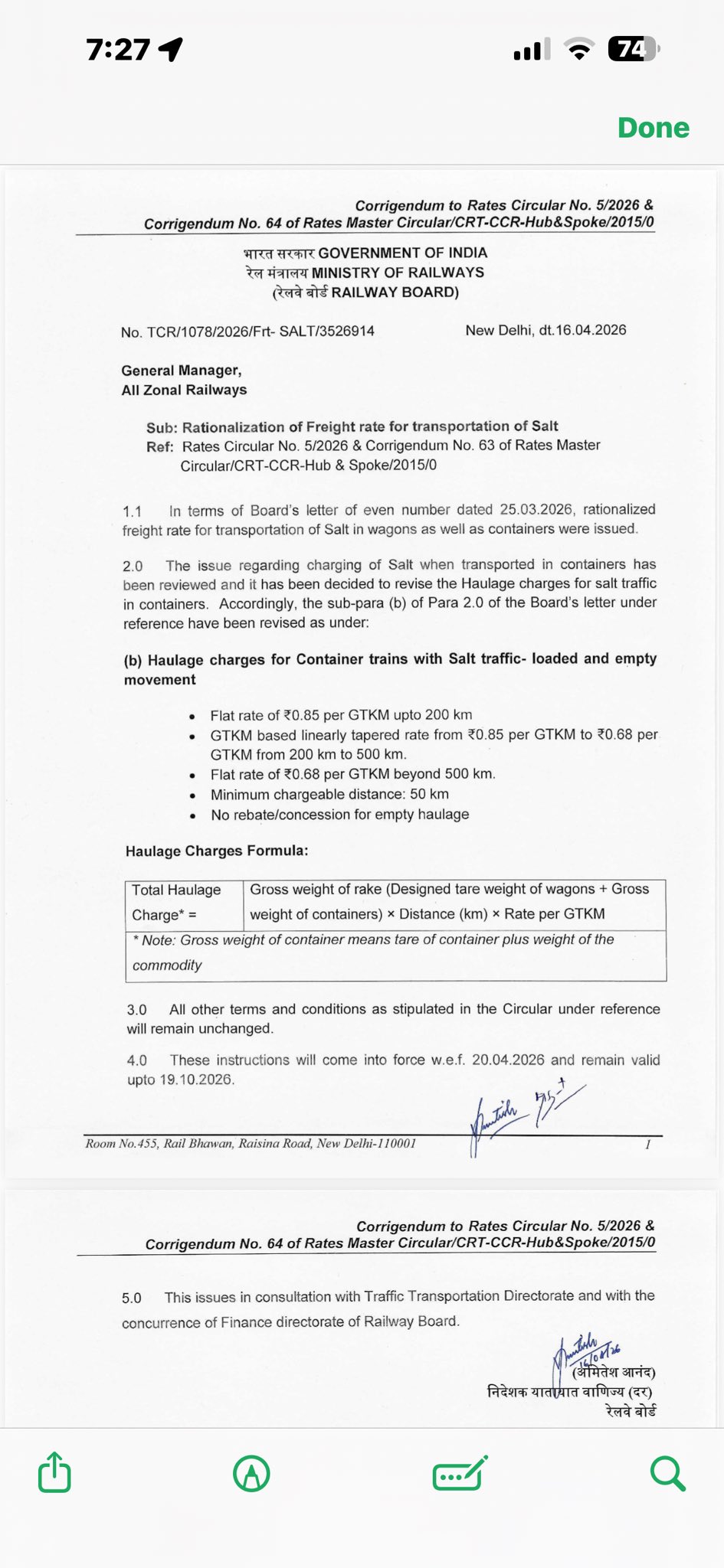

Has the rates been hiked or lowered? If lowered will it not affect bottomline of Kalyani? Or volumes will increase to compensate ?

As per my understanding, Rates have been decreased for transporters not for Kalyani.. as a result of which transportation through Containers will increase and that will benifit kalyani by receiving more Container manufacturing orders.

Correct me if I am wrong

3 Likes

Yeah I also think so…it will boost Kalyani’s topline

Well that was fast.

Rs 10,350 Crore Scheme Nears Approval:

5 Likes

Is Adani Enterprises also in the container manufacturing? If yes, small companies like Kalyani Cast Tech will get only a small pie.

Big players will come into this space for sure. But KCT being the only pure play in this space and good promoter pedigree will benefit the most. I do not see the point of investing in Adani or JSW if I wish to ride the container manufacturing business. Big players like Adani are better poised for container leasing business which requires deep pocket and high margins.

1 Like

Any idea on the H2 results? They haven’t posted any order wins. Is it going to be flattish or muted?

The opportunity from PLI is huge if you compare it with the market cap, even if able to catch a small portion . But giving a percentage would be imprudent as it adds more bias. However, I am able to see a direction in which the company is progressing.

Lloyd’s certification for corner castings is a barrier no peer currently has. Kalyani Cast Tech is one of the first movers, which gives them some advantage.

Another moat they have is the patents they hold and the culture of innovation, although this could stem from the promoter — which makes it both a moat and a risk.

Be it wagons, specialized containers, or ISO containers, each carries an independent probability of success. Any single outcome turning favourable is sufficient to re-rate the story.

The key risks I foresee, based on discussions with a friend, are that government policies—although favourable in the short to medium term—could change, especially with the general election coming up in 2029(although seemingly distant, I was unable to ignore it). Execution is also a major risk, along with the possibility of leverage or dilution.

Invested - probably biased

3 Likes

How much topline do you expect the Comany to post by 2029-2030…Any estimate?Also will they enter ISO segment after the govt scheme?

1 Like

This has been discussed earlier in the thread—RocketMan has already shared a detailed view on both topline and the ISO segment.