Sir,

Status of your take on this please?

Have you already bought OR still evaluating?

Kishor Barhate

Sir,

Status of your take on this please?

Have you already bought OR still evaluating?

Kishor Barhate

Thank you @Mehul1 @Nimit @krb2709 for your inputs.

@krb2709 Yes, I’m buying Add-shop E-retail & some SRG Housing finance.

Sold some Time Technoplast

You investing in this coupled by the mouth watering price makes me interested in this company again. I’ll take another look at it. A couple of questions for you about addshop.

I tried there website and their website is poor BUT it works. (Last year it wasn’t working at all)

Hi Nimit

Guess you have received the products from the company. How is the quality of the same? Will you buy again or recommend to others? Are they using a good logistics partner for the delivery? Anything to note on customer service?

Hi

My bad, I forgot about posting here.

The stuff got delivered in a week. The quality of instant coffee is OK. Add shop is just retailing it. Kwality Traders Tea Leaf Pvt Ltd is noted as manufacturer and packager.

The toothpaste is good. Manufacturer is Dada organics (promoter owned private company).

Although I didn’t pursue Add shop due to high receivables.

ADD-SHOP E-RETAIL

I though I will give detailed answer to you post, but I took so many days to understand(again) that I’m too lazy to do that. really sorry for that.

(Setting up of herbal & ayurvedic processing unit for manufacturing of cosmetic & non-cosmetic products at Village Padawala, Taluka Kotdasangani, District Rajkot (“Project”); 208.75Lakh - RHP)

They are into trading business where they are pushing sales on long credit terms. As long as they do that they will have high receivables. I don’t remember exactly but I did not find any bad debts in past Annual Reports.

I did not find anything fishy in past AR’s, if nothing is wrong, it is investable for me.

Yes receivables were equal to market cap. because market is acting irrational due limited availability of information, bad financial decisions of promoter and it being a micro-cap company.

In the next post.

Risks:

I see promoters as illiterate in finance, so this is a biggest risk.

Company is growing faster than its capacity, they need to slow down to 20-25% growth only, and now on I think they will.

Good thing is they recently onboarded Mr. Pradipkumar Harjibhai Lathiya who have 10 years of experience in finance, I dont know how good he is but I’m happy with this development.

Discl: Invested, may be biased, my research can be wrong or erronous,

Not a sebi registered, this post is only for educational purpose.

26-08-2023

Portfolio update -

Equity - 62%

Debt - 38%

| Equity | Allocation | Avg buy price | |

|---|---|---|---|

| ASRL | 16% | 35.88 | |

| TTL | 29% | 38.59 | |

| SRGHFL | 28% | 204.28 | |

| PUNJABCHEM | 27% | 772.45 |

| Debt | ||

|---|---|---|

| Vastu finserve | 22% | |

| APCRDA | 44% | |

| UPPCL | 29% | |

| Avance Financial | 6% |

Dear @kalpesh4430

Did promoters ever clarify why they sold a major part of their holding…? Thanks

Regarding Add Shop E Retail:

ADD-SHOP E-RETAIL

Promoter shareholding changes

March 2019 - 62.99%

Number of equity shares - 64,74,125

Equity capital – 6.47cr

March 2020 - 62.99%

Number of equity shares - 64,74,125

Equity capital – 6.47cr

March 2021 - 62.99%

Number of equity shares - 1,13,29,716

Equity capital – 11.33cr

Promoter shareholding - 71,45,660 same as previous year

Bonus issue of 48,55,591 shares fully paid up bonus equity shares on Friday, July 24,

2020, in the ratio of 3:4

March 2022 - 58.07%

Number of equity shares - 1,92,56,701

Equity capital – 19.26cr

Promoter sold 9.65Lakh shares.

Promoter shareholding - 1,11,82,356 shares

Bonus Issued – 7,926,985 equity shares of Rs. 10 each through bonus issue vide exchange ratio 7:10

March 2023 - 36.03%

Number of equity shares –2,83,10,000 shares (Approx)

Equity capital – 28.31cr

Promoter shareholding - 1,02,00,093 shares

Promoter sold 9,81,910 shares

Bonus Issued – None.

Warrants - Issue Convertible Warrants to Non-Promoters of the Company on Preferential basis (Approx. 89,53,299 warrants issued as per my calculations)

As per my understanding promoters tried to please shareholders by issuing bonus shares in FY21 & 22, business continuously demanding more outside money as they are growing more than their means, so they had to issue warrants in FY23. As warrants were to issue to non-promoters, promoters shareholding further gone down.

Promoters sold 19.46 Lakh shares in Feb-May 2022, in that period stock was trading at 17 to 20 PE, which was a good time to sell. So basically there are two possibilities I see,

As promoter is now flooded with money, there are chances that he can take advantage of low market prices to increase shareholding, but as per today’s company update, I think more of his son want to start own business, so may be part of this money not coming back.

New shareholders ie. Thobhani family, Kebbehali Panchilingaiahumesh & Mahendra Pratapsinh Khengar now may have part in decision making of company which seems good development as promoters are not good in handling finance.

As promoter shareholding is very low, they will try to increase it or try not to decrease it further by dilution, so chances of more dilutions are less and mindless growth should also settle to comfortable 20-25% a year.

Note : Not sebi registered analyst, this information is for study purpose only.

Invested, may be biased.

To build a concentrated portfolio you need to know -

I always wondered why many people cannot invest 15-20% in single stock, after spending some time alone in silence, I found the answer to why I can do it and many can’t.

What I’m doing is “betting on stocks where losing money is difficult.”, instead of focusing more on making money.

But would not that has an opportunity cost attached to it which could become significant in a bull market kind of scenario

ADD-SHOP E-RETAIL

Promoter sold 25L shares again to same people, I don’t know what is going on? is company getting new promoters or they are just investors? is this the entry of operators?

anyone knows who are those people?

Nope, actually high downside protection also comes with high upside potential.

Goldiam International

(Bloomberg) – One of the world’s most popular types of rough diamonds has plunged into a pricing free fall, as an increasing number of Americans choose engage…

Totally understandable, me too find it tough to manage a portfolio and do a 9-5 job.

Thanks for the clarifications and your analysis on promoters holding.

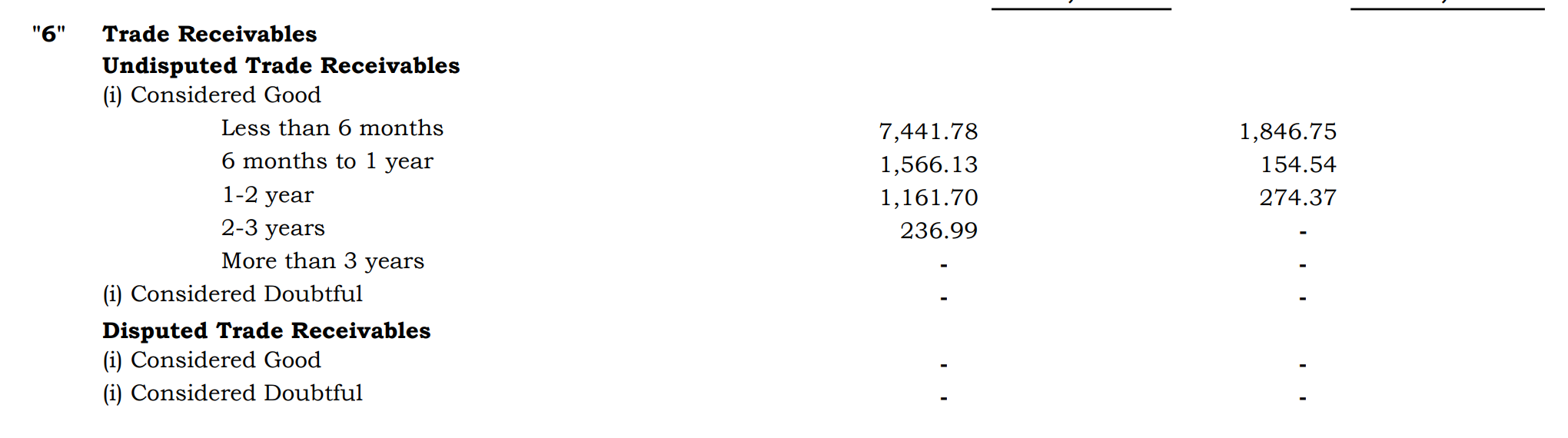

I still think their trade receivable profile isn’t promising.

Previous years trade receivables are getting carried forward.

(1-2 year old 2022 amount is 2.74 cr. 2023’s 2-3 year old amount is 2.37 cr)

(similar flow from 6m-1yr to 1yr-2yr …)

Apart from this, today, over 46,000 families are involved in this self-employment generating activity of

spreading health to everyone and more than 80,000 Authorized Distributors who have a presence in

more than 25 states throughout the country

And yet somehow they have 0 doubtful and 0 receivables written off.

They do MLM (46000 families), if they are selling their products to individuals at credit then they should definitely have doubtful receivables. If not, then they shouldn’t have this high receivables.

The third possibility is that most of their business comes from 80k distributors to whom they sell their products at credit.

And on the other hand, Add shop buys 146cr worth stuff from Dada organics (Pandya sir’s Proprietorship) in 2023. Trade payables stands at 35.6cr, entirely payable to Dada organics (pg 110 AR’23). => 110cr cash generated by Dada organics in AR’23.

PS: I don’t want to sound like a conspiracy theorist but err on the side of caution!

The valuations are attractive but the bet is risky.

Conclusion for me has been to stay away from the company until there is clarity on promoter selling, massive stock purchase by non promoters, new CFO and again a super high receivable which sucks away all the cash from the company and gives it to Dada organics.

I hope things get clear soon.

disc - holds tracking position.

ADD-SHOP E-RETAIL

No. It’s not like that, I’m not in 9-5 job, i’m full time investor ![]()

Yes, so what I did was I simply reduced book value by 15cr, it is still looking a great valuation.

Correct.

Yes, they do have related parties with significant transactions, this is definitely a flag.

I wrote to management just before AGM to get clarity, they took these points in AGM.

And 35cr is payable to Dada organics, which means company is enjoying good credit from Dada organics.

I couldn’t find AGM recording, but as far as I remember I will put here…

Dear CS,

Following are the questions I would like to ask,

Promoters have sold large shareholding, and all promoters family members also resigned recently, is promoter selling & exiting from company?

Ans: Promoter is not exiting the business, shares sold because promoters had to pay personal loans. Mr. Pandya also clarified that his family had only 25% of rightful shareholding, over & above that did not belong to them

Few investors have bought large shareholding recently from promoters, are we getting new promoters?

Ans: No

Why are our receivable days so high?

Ans: 80% of sales is to the farmers, where 6-7 months receivable is normal industry trend.

I would like to know the revenue break-up between Agri related products & FMCG products?

Ans: 80-85% comes from Agri & balance from FMCG.

I would wait for 2-3 more quarters to see if the things going in the right direction & if management taking right decisions.

My take is more of the accuracy in book keeping. 0 doubtful & 0 receivables are written off whereas with their distribution model one would expect at least a small number.

Again, with a purchase of 146 cr from Dada organics add shop is having only 35.6 cr credit from Dada and Dada made 110 cr cash but Add shop has 100cr stuck in receivables.

Thank you for adding more information about the company and answering the open questions. This is definitely in my tracking list and I will take a position once receivables improve.

Hello Kalpesh just wanted to know, are your views still favourable about asrl ?