I came across this on one of my screens couple of weeks back.

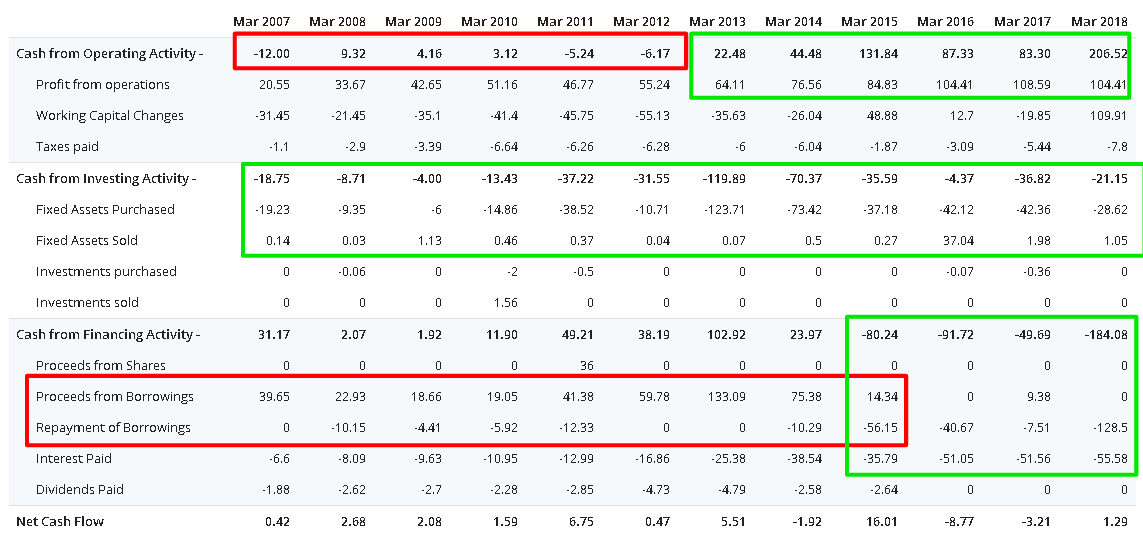

One thing which stood out for me was that the market cap (270 cr) was less than the Cumulative FCF over last 3 years (304 cr.)

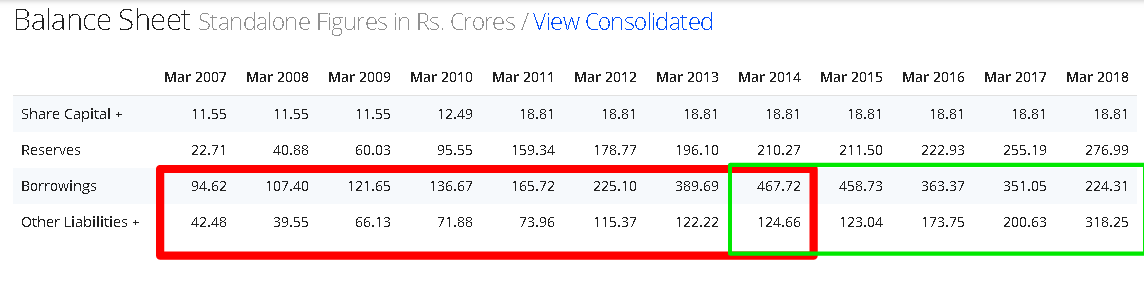

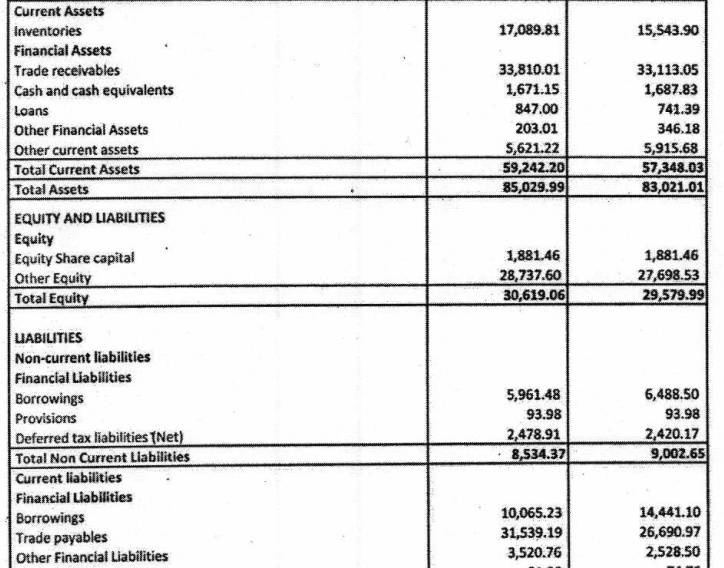

There has also been deleveraging with reducing debt levels as captured in the above Cash Flow statement and below balance sheet.

I have also gone through the last 10 years AR and summarized my take on the price action over the last 10 years as below:

I intend to capture my findings over the next couple of posts. There is a lot to cover and tl;dr version is as below:

About the Company

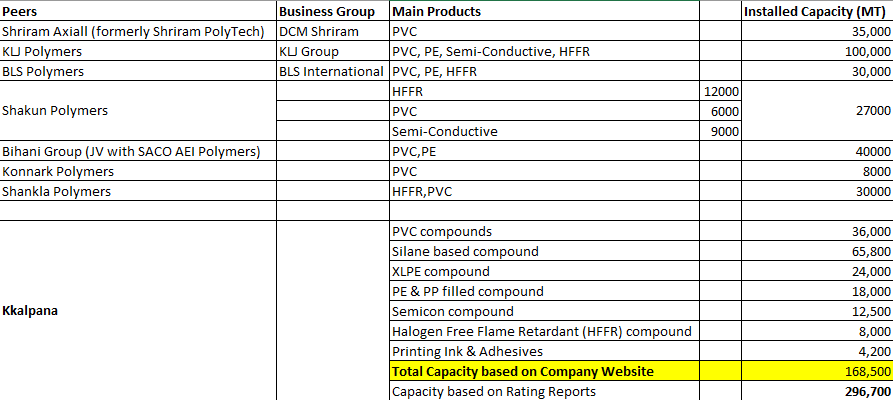

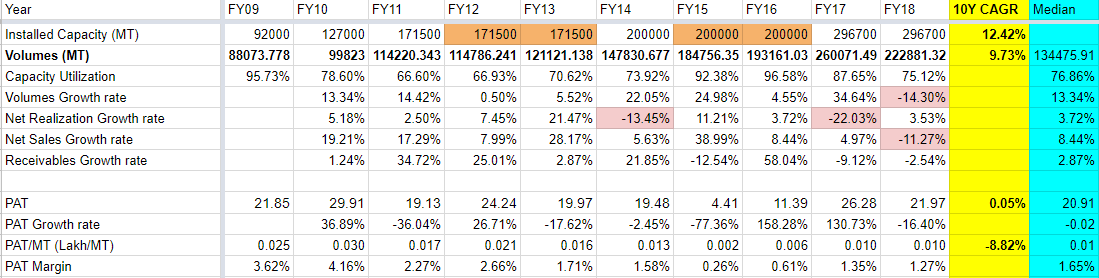

KIL, incorporated in 1985, was promoted by Late D.C. Surana and Mr. Narrindra Suranna, son of Shri D. C. Surana, in Kolkata. In 1985, the company established a unit in Daman for the manufacture of poly vinyl chloride (PVC) compounds. Sustained expansion over the next decades has resulted in diverse product portfolio consisting of PE compounds, PVC compounds, master batches, engineering plastics, reprocessed compounds. The company has seven manufacturing plants situated in West Bengal, Daman & Diu, Dadra & Nagar Haveli and Noida with an aggregate installed capacity of 2,96,700 MTPA.

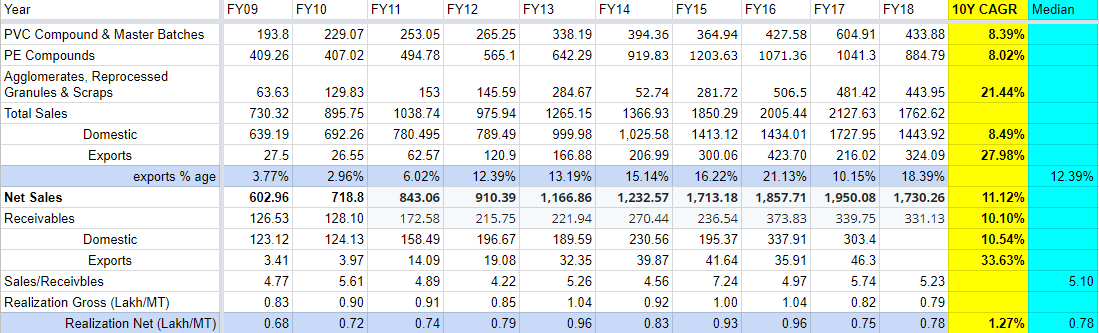

The largest amongst this is PE compounds (comprising 54% of sales) with strong market leadership in sub segments such as Sioplas (market share of 50%), XLPE (market share 33%) and Semicon (market share 25%).

Established strong relations with suppliers as well as customers in the industry. KIL’s customer base includes large wire and cable companies such as KEI Industries Ltd, Havells India Ltd, Apar Industries Ltd , KEC International Ltd (rated 'CRISIL AA-/Stable/A1+)_ amongst others

KIL’s top clientele comprises established players in the domestic cable industry along with export presence in more than 24 countries. CARE observes that KIL’s top clientele is well-established with repeat business accruing from such clientele (more than 80% of turnover is generated from repeat customers). While the low customer concentration is likely to insulate the company’s revenues against loss of customer(s), established relationships with renowned clientele is expected to provide stability to revenues and drive business going forward. Further, the wide spread customer segment base such as cable, footwear, white goods, pipe and packaging industry mitigates the impact of any industry-specific downturn on its revenues

The company earns around 15% of its revenue from exports to more than 24 countries, which are LC backed with majority of the payments having tenure of 60-90 days. Further, the company also imports its raw material requirements from Middle East, Japan, Malaysia, Indonesia, Thailand etc. on similar payment mechanism i.e. LC backed with majority of the payments also having tenure of 60-90 days. However the imports hold a bigger pie as 30-40% of the raw material requirement is imported; providing natural hedging to an extent. The company also regularly hedge its forex exposure, however, the timing difference between payment and export proceeds, exposes the company to volatility in foreign exchange.

The major raw materials required are PVC resin, LLDPE and LDPE contributing to almost 65% of total raw material cost. The price of LLDPE/LDPE and PVC are linked to crude oil prices which are volatile in nature. The operating profitability of the company has been lower in the range of 4-4.5% during the last three years.

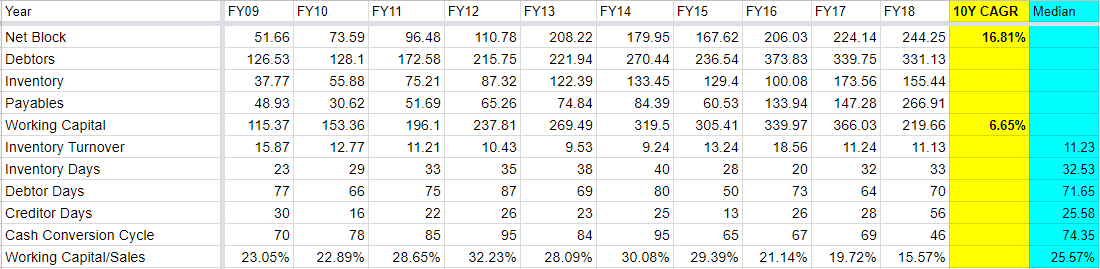

The company has manufacturing facilities in West Bengal, Daman and Silvassa which are on east and west coast of India. Strategic locations of its plants provide logistical advantages for imports of raw materials as well as exports. Proximity to suppliers and ports also benefits to keep tight control over its inventory management marked by inventory days of 20-40 over last 8 years. Volatility in raw material prices (crude oil derivatives) impact operating profitability in this industry. The discipline in the inventory management has helped company to protect from vagaries of volatility in raw material prices, mainly crude derivatives and sustain its operating profitability in the range of 4-7% over last 10 years

Company procures around 70% of its total raw material requirements from Reliance Industries Limited, Indian Oil Corporation Limited and ONGC Petro-additions Limited, leading to lower bargaining power with suppliers.

Excerpt from FY18 AR: Revenue from five customers is INR 194.72 (P.Y 233.86) crores which is more than 10% of the total revenue of the Company

Pros:

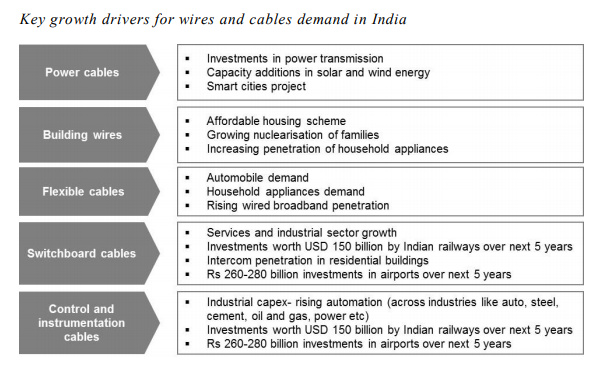

- Irrespective of which government comes in, the focus will be on transmission and evacuation infrastructure of the RE plants which are expected to be commissioned over next 3 years implying potential tailwinds for solar/wind cables at the minimum.

- Both Apar and KEI have posted good numbers with respect to the cables segment.

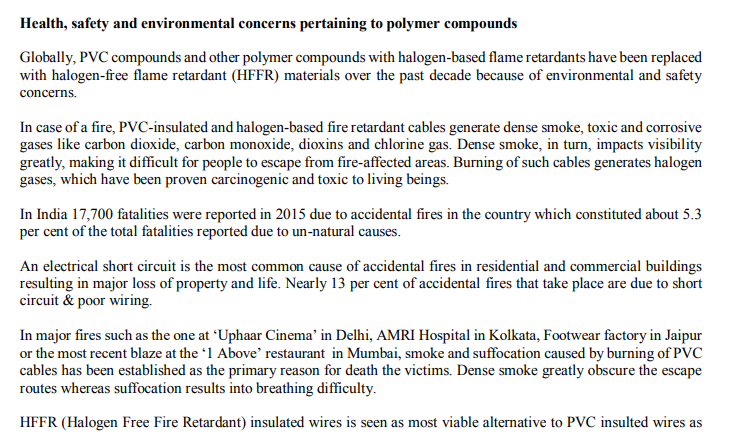

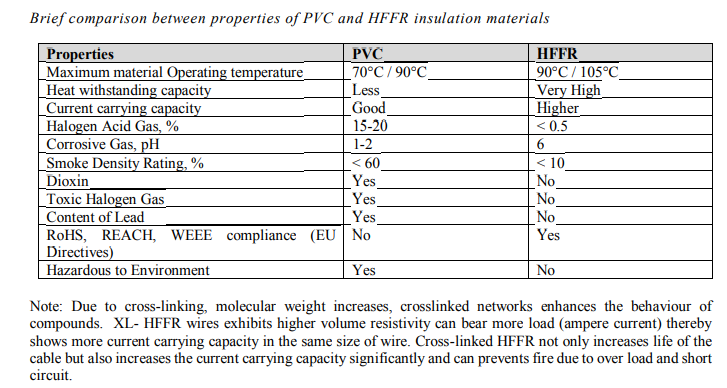

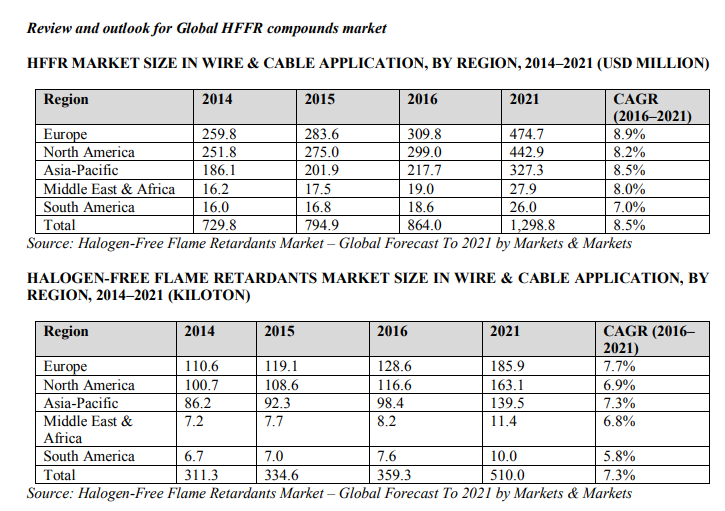

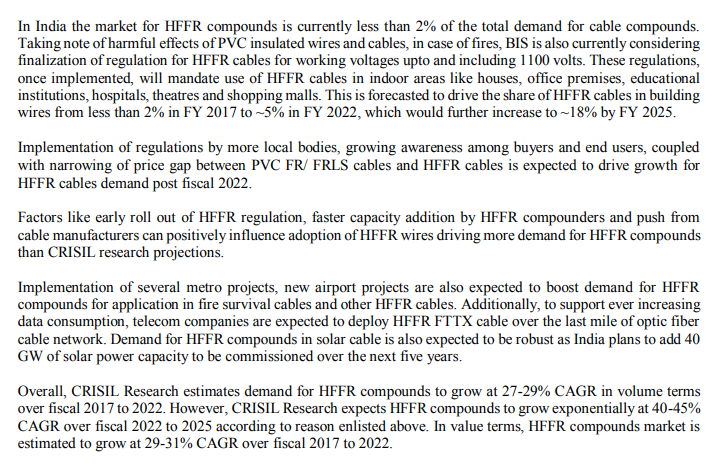

- Introduction of stricter BIS regulations related to HFFR - Halogen Free Fire Retardant which is more REACH and RoHS compliant.

- Increasing focus on HV and EHV power cables.

Negatives:

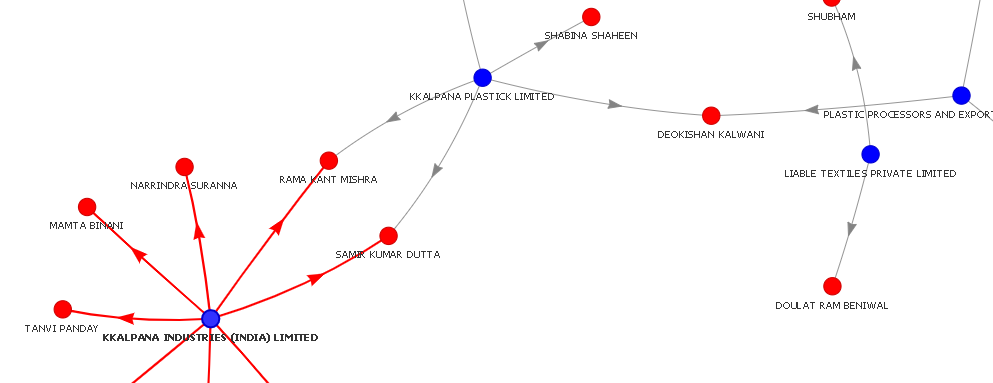

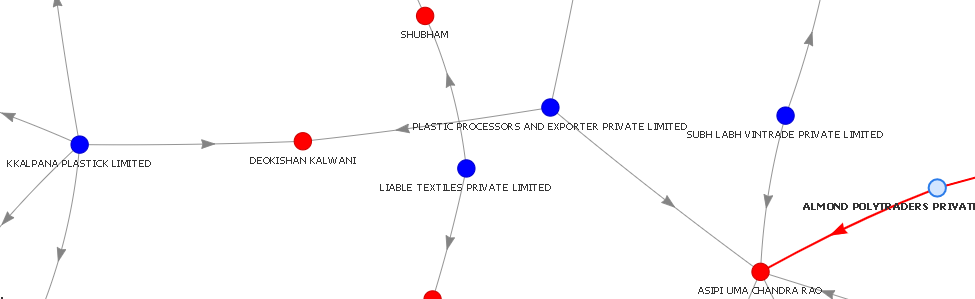

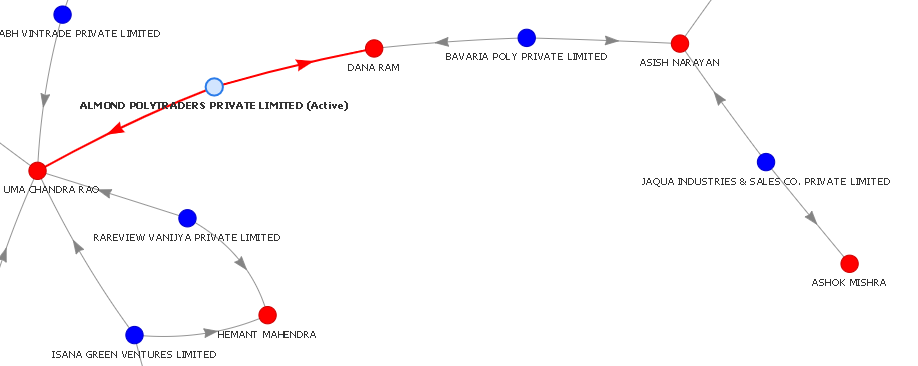

- Over and above the promoter holding, there is additional 13% held by entities indirectly linked to Promoter (Will be uploading the tofler network snaps in later posts). This gives rise to a non-significant likelihood of possible pump and dump in future though they do not seem to have engaged in frequent bulk/block deals and seem to be genuine long term holdings which get swapped every few years.

- All 3 previous acquisitions were made through share swap and thus the equity dilution alluded to by @ayushmit back in 2013.

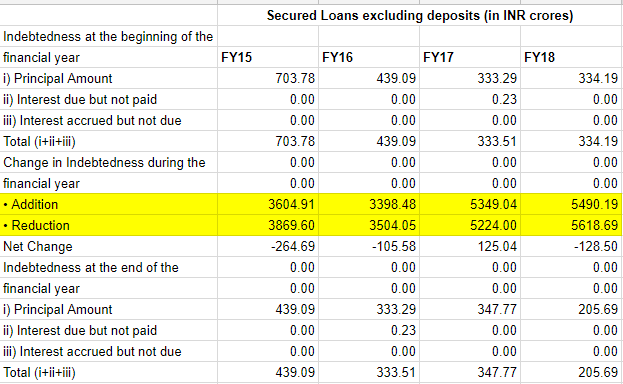

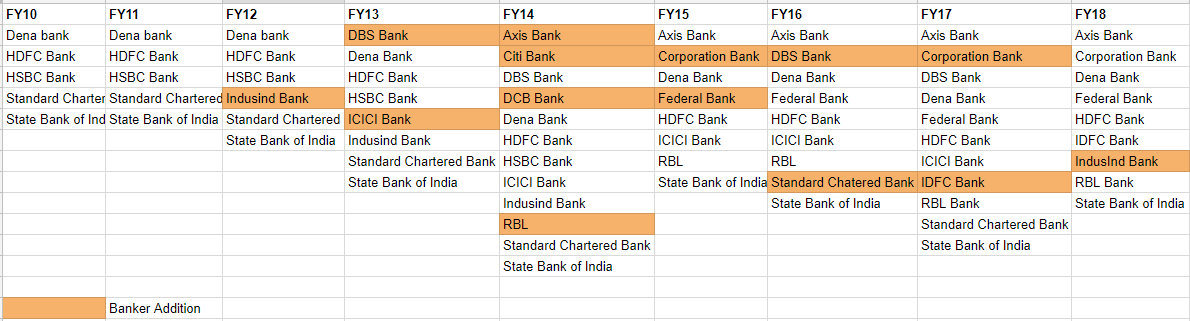

- Too many banker changes over the last 10 years. In addition, if one notices the “indebtedness statements” over last 4 years.They are making debt additions and reductions 10 times the actual debt levels. Would appreciate a more informed opinion if this is not unusual. This sticks out and have not come across this much of a difference between the rated debt limits and actual debt taken (almost an order of magnitude difference - 5000 cr. vs 850 cr. rated limit)

- Tax Evasion case against Kalpena Industries in Jan 2012 - No mention of it in FY12 or following AR’s. Kalpena Industries Limited vs The Union Of India And Anr on 1 March, 2018

- On August 8, 2017, SEBI had classified a list of 331 ‘suspected shell companies’ on the basis of MCA’s recommendation, which included KIL, and restricted their trading on the stock exchange. Consequently, KIL appealed in the Special Appellate Tribunal (SAT) against the impugned order and got it stayed. The trading on stock exchanges resumed from August 14, 2017 post the stay on order. KIL is furnishing all clarifications being sought by SEBI in this matter. Any negative verdict of investigation by SEBI in the above order against KIL will be a key monitorable.

Following Corporate Movie was published on Youtube on Feb 2018

Next Posts will be segregated based on following:

- Competition and Industry Commentary

- Get into the details of the negatives highlighted above.

- KKalpana specific number analysis in terms of realizations, volumes, exports, etc…

Hopefully I should be able to have all this up over the next 1/2 weeks.

Disclosure: Took a very small tracking position, mainly to motivate myself to do the research. Hope to get differing opinions and insights. Not a SEBI Registered adviser. Do your own due diligence. It is likely that I may close out my position once I am done with the research and end up with any negative conclusions.

However, something didn’t seem working and all and I got out somewhere in midway. In hindsight, I was lucky to have got out as despite so many years, the stock is probably at the same price.

However, something didn’t seem working and all and I got out somewhere in midway. In hindsight, I was lucky to have got out as despite so many years, the stock is probably at the same price.