Arun,

There are various benefits of going with organized players than unorganized ones. These are the factors shifting towards FBVs

as per report from Centrum:

1). Funding on FBV vs. only chassis: When a transporter procures only chassis from a dealer, the

funding is restricted to the chassis cost. However, if he procures an FBV from the dealer, the funding

is on Chassis + body. Typically on chassis of Rs. 1mn, body building would cost Rs0.2mn. Hence the

transporter gets full funding on FBV (Rs.1.2mn) compared to Rs 1mn on chassis.

2). Reduction in lead time and higher return on Investment (ROI): Compared to local garages which

typically take 1.5-2months for the delivery of FBVs, those procured directly from OEMs could be put

to use immediately. As a result, the customer need not wait and can immediately start paying his

EMIs after procuring the FBV.

3). Warranty of 18 months on the FBVs: Against the local garages, FBVs come with an 18-month

warranty and most organized body builders have 24x7 customer helplines.

4). Excise duty benefit on the FBV higher than for chassis: In budget 2003, to encourage fabrication

by organized players, excise rules of the Government permitted only organized body builders to

offset their excise liability to the extent of the excise already paid by OEMs on the chassis sent to the

body builders for construction of the superstructure. Further, in addition, as per the Budget 2012-13,

chassis will attract 14% excise duty whereas FBV will only attract only 12%. This move will incentivize

purchase of fully built vehicles.

These indicate that unorganized players are at a disadvantage than organized players for FBVs.

Tata as % of share has been going down and H1FY13, this had come down to 41% from 51% in FY12 and 59% in FY11. This is indicated in Centrum report.

The FY12 AR indicates that OEMs themselves push FBV than chassis. Hence don’t think that the point about need for institutionalizing sales here is needed from sectors as this is driven by OEMs. This is logical as poor FBV from garage reflects on OEM quality.

**If FBV market and penetration is not growing then there would be a very little case for investment here. It is a cyclical which is free from MHCV sales for now - Tata MHCV for Dec qtr has gone down by ~50% and in that light their Dec. numbers were decent.

**

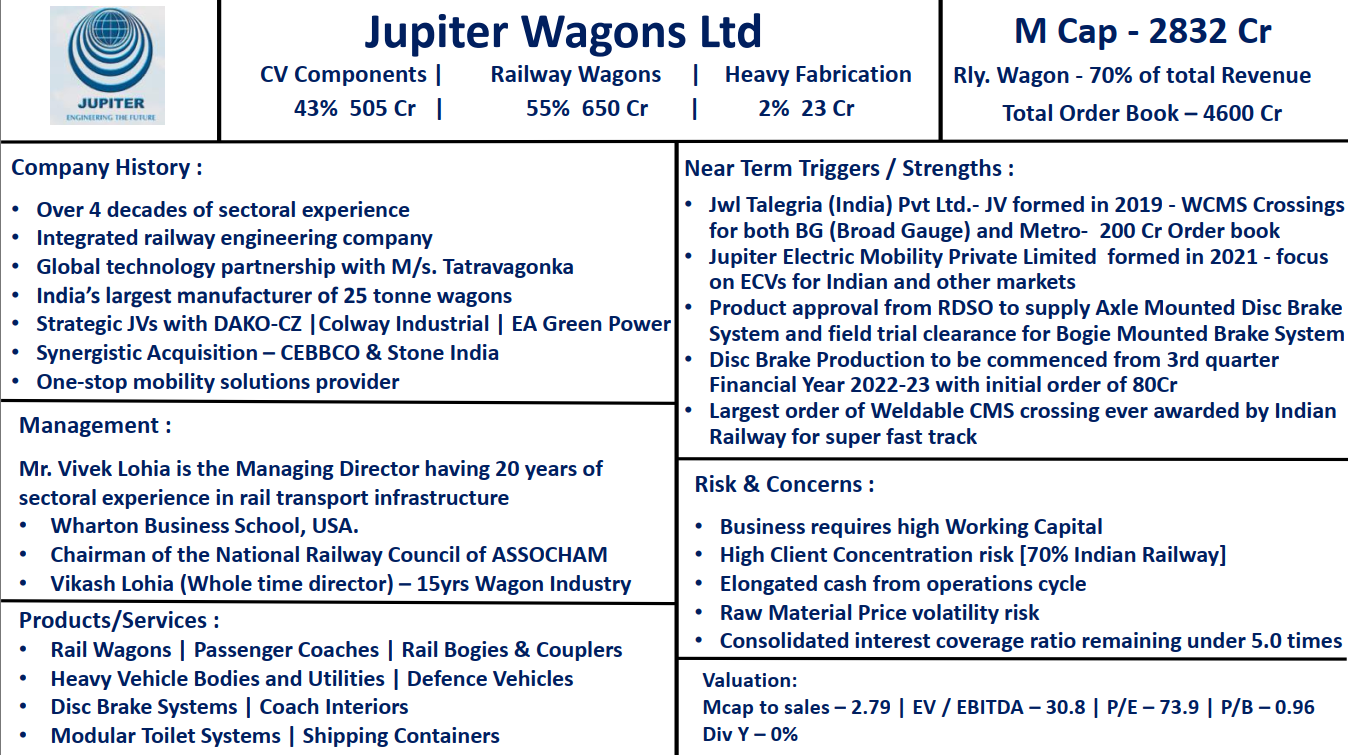

The train business is obviously not immediate and will take time to pick up. The point is that while the train business builds the capacity built can be used for FBVs as they are doing currently. They currently do have an order of 250 rakes from Stone India Intermodal which will come in a few quarters. Here also the Government has need of 25k wagons whereas they are ordering around 12-13k so there is an opportunity here.

Agree that the next couple of quarters will make things clearer.

I would compare this to a situation like polyfilms a couple of years back where there was an under supply and hence benefited the sector.