As evident from the results, the cash-cows Agri Segments and Performance Polymers have yet again given a strong quarterly performance.

However, the main aims of merging with the cash-burner retail business viz. tax shield from retail losses and lower finance costs (use of cash from other two) is still not visible.

Despite making a loss of 6.89 Crs at the PBT level, the company has incurred tax expense to the tune of 3.15 Cr taking it net loss to 10.04 Cr. However excluding this tax expense. net loss of 6.89 Cr (Q1FY13) vis-a-vis 11.92 Cr (Q1Fy12) looks much better.

The finance costs for the quarter at 6.58 Cr is significantly higher than 5.53 Cr (Q4FY12) and 4.18 Cr (Q1Fy12). The benefits of merger should come through in these two fronts the earliest.

Also, in the retail space, most retailers are showing a slow-n-steady approach rather than going aggressive. Retail results at the EBIT level, shows a significant improvement as compared to Mar-12 and Jun-11 Quarters.

Since the current valuations are very poor, it is highly unlikely that company will come forward to raise equity funding at these levels.

What can be the possible valuation of the company considering the following case ?

Agri-business and Performance Polymers : Business-As-Usual

Retial : Slump Sale.

We need this valuation to effectively gauge the margin of safety and downside from current levels.

I think the most shareholder friendly thing the management can do is to demerge the retail division into a seperate entity. Or better still, find a worthy suitor and sell the damned thing off.

this would effectively put up the main cash generating businesses in a seperate entity whose valuations can eclipse that of the whole consolidated entity.

And Mahesh, regarding the management not pursuing aggressive retail expansion strategy, I think it might be a good move. While aggressively pursuing retail expansion, wont it be throwing good money (earned by the main bread winners) after bad money (losses from retail ventures)?

After all one never knows when retail ventures will start generating profits and cash.

Only Performance Polymers business, especially the Industrial Products business (Food Polymer & Latex) has turned out an exceptional performance and not the Agri-and Consumer Products (Jivanjor) segments…Agri segment steady performance that you are seeing is because of pre-sell ahead of kharif season and if situation doesn’t improve on ground it will have severe impact on SSP sales in coming qrtrs…However, thats an external matter and not in the hands of the company…Consumer Products business (Jivanjor) has actually degrown YoY by 11.9 %…Its only Industrial Products business (Food POlymer & Latex) that has saved the day for the company by growing 36 % YoY.

Yes…the benefits are still not visible because there has been no initiative from the management to pursue the aims of the merger…The lower loss that you are seeing YoY is not atall any sign of improvement…If Retail business scale remains stagnant on a YoY basis in FYY13 then you will see losses expanding… Also, goodwill amortisation expense worth INR 12 cr. will be charged at the end of the year…

The aim as stated by the management at the time of merger of using cash of other businesses for growing retail business was right to an extent but actual aim was to raise euity funds and increase leverage capacity to increase the Retail scale significantly so that profitability can be attained at the earliest. Unless the funds are raised the costs will mount…

**

**

A slow-&-steady approach should in no way become a stand-still approach otherwise it will kill the business itself… Take example of any serious retailer like Hypercity, Big Bazaar, AB, Bharti, etc…, noboby has stopped expanding…what they have done is they have started expanding at a slower pace than they planned earlier…In contrast, what Jubilant is doing ??? Has stopped expanding totally from June’2011 when its 5th store got operational…Management had clearly laid out plans in interaction with PWC to open 2 stores in FY12 and 3 stores in FY13…FY12 is through and only 1 store was opened instead of 2 and Q1FY13 has passed and still no store is opened…This is not atall a good sign…

Rgdg. your observation that Retail segment has shown marked improvement at EBIT level over Mar’12 and June’11 qrtr…I think you are missing the fact that Mar’12 qrtr. Retail EBIT included 12.37 cr. goodwill amortisation expense subtracting which the actual l-t-l loss comes to 20.4 cr. for Mar’12 qrtr…Yes the company has improved EBIT margins in the qrtr. by 278 basis points YoY but this is not atall any significant improvemtn we can take heart of as such fluctuations in margins are normal when you have EBIT loss margins at 20 % +.

**

**

Agreed… company might not come out with equity funding at parent level because of low valuations but it can definetly invite a strong PE funding at subsidiary-level

As indicated by me in Q1FY13 analysis, the downsides look maximum till Rs. 135 based on current scenario but the upsides look impossible…If Q2FY13 also passes without doing anything, downsides could expand…The SOTP valuations are already carried out by me in my 2011-research-note, however, unless immediate fund-raising is done for raising the scale of Retail business, it will also bring down applied valuations of Agri, CP and IP businesses as on a consolidated level company will be in a mess…Hope management does take some steps in interest of minority shareholders.

Hitesh… Retail business is already there in a 100 % owned subsidiary…and if they wanted to dispose that off they would have not gone for merger formalities and sold it off previously itself… Where the hitch is there that I am unable to figure out somewhere something is terribly wrong in the management as otherwise why such step-child behaviour is done with this company ??

No Hitesh…not expanding at the current scale is not atall a good option because its a value-retail business and not the premium-retail business…Also, its presence is local and not national…If locally, which is its stronghold, it allows competition to flourish without itself expanding scale then the national level expansion will be impossible and it will loose from everywhere…if this approach continues then the entire current scale will get eaten up and company at the consolidated level will be in a big trouble like the many we have seen in Retail segment…You see Hitesh, company’s business model is good and the local focus is also good and with this model and focus it can achieve profitability very fast atleast at EBITDA level…However, one more year like this and the company will loose the entire opportunity…

Your contention that Retail ventures, especially value retail, are not profitable is a general impression we have because of the biggies that we have seen… however if you study the Indian cos. closely and go deep down there, you will find that its a great business only the things need to be put right…We have many exs. like D’Mart, Viveks, Namadhari, etc.

Great analysis as always. Given your SOTP valuation of 385 Cr, and completely ignoring retail business, we have 260 Cr.

Now the current market cap of 166 Cr gives considerable margin of safety, even if the company rolls off retail and continue the other business.

What is urgently required at this point, is the management guidance regarding retail expansion. Many retailers are postponing fund raising till FDI in retail is announced, at which point they will get better valuations (god knows when that will happen!)

Given the management pedigree of the group, their other retail foray (dominos) and strong promoter holding, I am somewhat hopeful that things might turn better in the subsequent quarters.

Jubilant FoodWorks held a conference call for discussing the performance for the quarter ended March 2016.

Highlights of the call

The net sales increased by 14% to Rs 617.86 crore driven by growth in customer base on the back of wider outreach for Company’s Domino’s Pizza and Dunkin’ Donuts networks, incremental share of orders from the online platform aided growth, gains from new product launches which served to draw in new set of customers and building momentum in SSG for Domino’s Pizza on an expanded base of restaurants. The net profit has decreased by 6.5% to Rs 29.47 crore due to pace of expansion in profitability was moderated owing to SSG that stood below potential due to un-favorable macro conditions. Earnings during the period also reflect the influence of higher tax on account of investment allowance benefit of only one year as against that of two years in the corresponding period last year, along with higher depreciation witnessed on the back of commissioning of new commissaries, last year.

Same store sales growth (SSG) (YoY) for Q4 FY16 was 2.9% against 2% in Q3 FY16, 3.2% in Q2 FY16, 4.6% in Q1 FY16 and 6.6% in Q4 FY15.

36 new stores were opened in the quarter. The total number stores as on 31st March 2016 is 1026, which was at 876 as on 31st March 2016, present in 235 cities.

Average OLO contribution to delivery sales in Q4 FY16 was around 41% against 29% in Q4FY15. Mobile Ordering sales contribution to overall OLO was around 38%. Currently, there are over ~3.9 mn downloads of the Domino’s Pizza mobile ordering app across various smartphones.

The new launches from Domino was Double Cheese Crunch Pizza and Custard Bliss

The company has 71 Dunkin’ Donuts restaurants in India as on 31st March 2016 in 23 cities. The Company opened 4 new restaurants in the quarter.

The Company has over the last few months taken a strategic decision and decommissioned 3 Dunkin’s Donuts.

These restaurants were part of the initial iterative stage where the brand was establishing its spot in the industry and thereby experimenting with various restaurant formats/models. The Company being prudent in its operations and guided by stringent ROI norms deemed it appropriate to take such a proactive step. The Company remains committed to expansion in a highly profitable manner and at a steady pace

The new launches from Dunkin’ Donut was Big Joy Burger, Range of Donuts and Range of New Coffees

Dunkin’ Donut delivery business – Deliver model is followed all over India. Very confident of Dunkin’ Donut store model.

Dunkin’ Donut contribution to total revenue was 8-10% revenue and 5% at EBDITA. Dunkin’ Donut impact on overall margin is 200 bps in FY16

Mgmt clarified it does not use potassium iodate/bromate in any of its products and carries out regular tests to ensure all its products are compliance assured.

Demand scenario - Sentiment has not change much. By and large demand in both big and small cities is growing at similar pace. New stores’ SSG is lower than that witnessed by old stores

The mgmt said that delivery side business is growing faster than dinning business.

There has been no decline in order size. Orders have reduced QoQ, typically Q3 is better in number of orders. Orders declined in FY16 YoY slightly impacted by price hikes taken during the year.

Promotional activity - Barring 3 week offer, promotions offers were same as seen in Q3FY16. Since the 3-week offerdid not see great response, the company is unlikely to dole out such offers again.

Had 3 weeks 50% off offers, which impacted gross margin Gng fwd, will have gross margin similar in line with Q3 FY16.

The company has tied up with Wipro to help reduce energy consumption as it improves cost efficiencies. It is the only company in the food space to implement six sigma cost saving practices across the company.

Staff costs was not negatively impacted by hiring of delivery persons by online players

Tax rate for FY17 - 31-32%

Capex for FY17 – Rs 250 crore.

On same store basis, margin have not declined. 150 new restaurants which were added were less profitable and Dunkin’ Donut impacted the margin. 724 Domino Pizza restaurant margin are intact.

Long term loan and advances were up because mostly of security deposit for new restaurants

The mgmt said that gng fwd, at best 3-4% one small price hike in FY17.

For FY17, target of around 130 - 140 new Domino’s Pizza and around 20 new Dunkin’ Donuts. Half Domino Pizza restaurant will open in top 10 cities. The mgmt said that it is very particular about payback period of restaurant of 3 yrs or so.

India accounting standard impact: It will have 2 negative impacts: security deposit for premises; and ESOPs to be valued at fair value. A positive impact will be lease rentals will not be required to be accounted for on straight line basis

Promoter stake - No basic change in strategy of promoters; will continue to maintain stake at 40’s level and committed to remain invested over longer term.

Looks like you are adding Jubliant Foodworks Conference call details in Jubliant Industries thread.

May be you can add this detail in Jubliant Foodworks thread.

@hitesh2710@crazymama@Prdnt_investor@Mahesh

Jubilant industries brand “Jivanjor” is being sold equally and displayed more by dealers in Hyderabad. After giving better margins to dealers and lower price to customers , it’s just floating at breakeven.

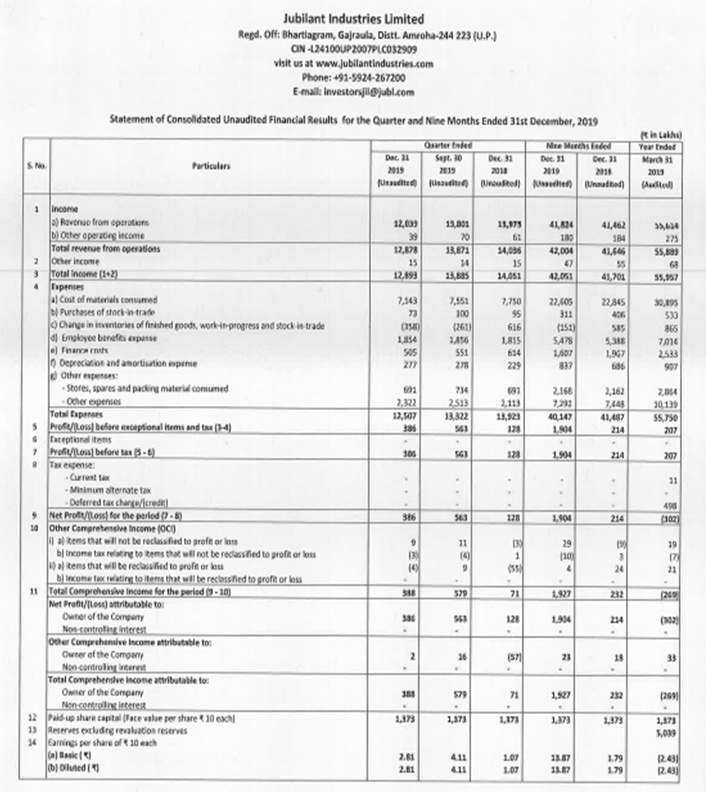

Q1 FY20 earning are awesome. Few months back a new CEO is recruited. Consolidated earnings are declared every Qtr now. Promoters infused capital for debt repayment and increased stake.

Sales and margins are growing well from last two Quarters.

Even in remotely located streets distribution is there. Shops are flooded with Tins of Jivanjor.

Dealers said both fevicol and jivajor are moving well. They go as the carpenters ask. Some dealers even introduced me to carpenters and asked me to take feedback from them.

Below are the images of plywood shop around my locality

Excellent results from Jubilant Ind. Half year eps is 11. Promoters hold 72%. Turning around in big way. When it made a ATH in Feb 2, 2017, Jubilant Ind was actually not doing well, actually making LOSS, but as Porinju bought it went to 414! Now the real performance starts after selling the retail loss making biz. And again my same reasoning. Mcap is way below sales, Promo stake is at 72%( which i consider excellent), excellent Group( Bhartia), and making profit and at half year eps, quoting at 10 P/E. And on top of that, all segment they are in, Co comes in with excellent quality which would remain as the management is excellent.

I hold.

This stock has been discussed in by experts since 2011. In 2015 also Porinju bought it and it made an ATH of 414 and that too when the Co was making LOSS.

Now in 2020, after 9 yrs of when it was first discussed, this comes in the category " NO Brainer" BUY…Do the math.

@ayushmit@Donald

Jubilant industries Adhesive brand “Jivanjor” is gaining traction in my locality (Hyderabad)

Out of nearly 10 plywood shops in my locality, only 2 shops are pure fevicol. Other 8 shops sell both Jivanjor & Fevicol.

Out of 10 shops , 4 shops changed their Shop’s Name Board to Jivanjor Branding.

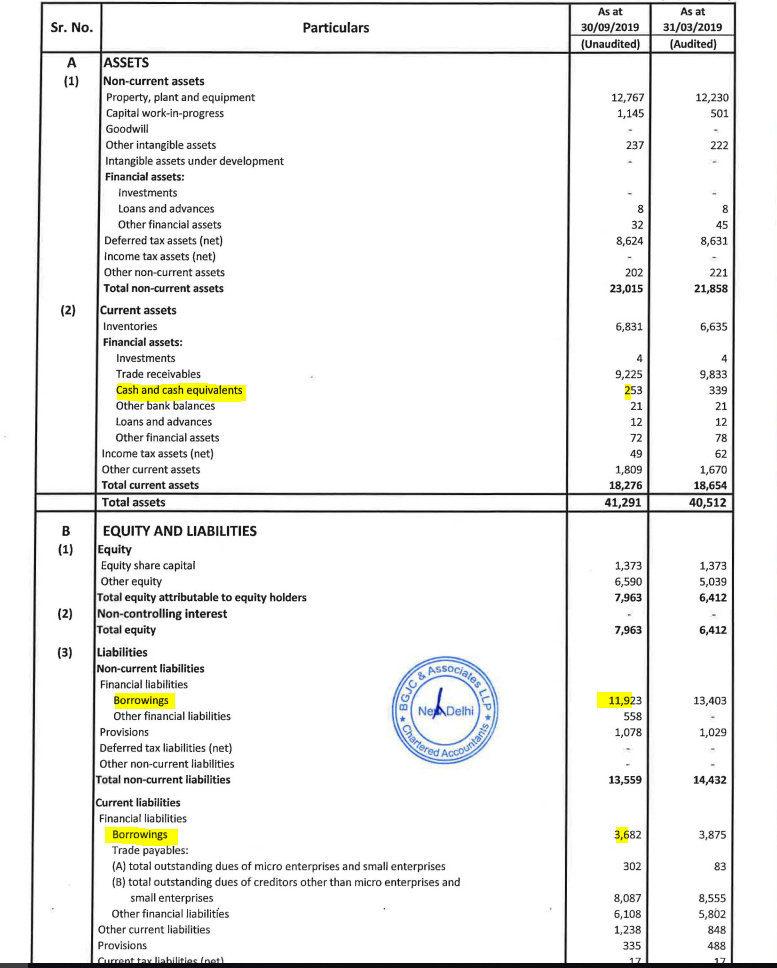

Balance Sheet changes like debt reduction is interesting

Hi, I have also observed decent presence of Jivanjor. Though i feel its more of a push model wherein carpenters and shopkeepers get incentive while Fevicol has a strong pull. Anyways, it would be good if we can know about absolute sales/numbers of Jivanjor?

Absolute numbers of adhesive division are available in your site in product segments. Yearly 370-410cr from performance polymers.

They are starting a closed down agro chem division in May, 2020.

If debt reduction continues, their 5 cr per Qtr interest will fall to PBT. They reduced debt from 262 cr to 156 cr in sep Qtr.

Twitter handle active for jivanjor from November, and Branding is going well after recent CEO change. Promoter infused funds and increased stake to 72% from 68% and helped in debt repayment

Are you sure they have debt? I think they are debt Free.I again opened the last qr results and not seen any Interest Cost in anywhere. Jubilant Ind is a Debt Free Co and no pledge shares from Promoters. They increased the stake from 68% to 72% @ 135. Which says, promoters were confident of the future growth of the Co. I hold a good quantity as I feel that it is the cheapest stock while looking at all parameters. I have written in past and writing again, Jubilant Ind is a non brainer stock. If Jubilant Ind can make an ATH of 414 when it was making LOSS, why it can’t touch 400 again when it has started showing profit.

Please Check March & september results for Balancesheet details. Even otherwise also they pay 5 cr interest per Qtr. Check for “Finance Cost” in any Qtr Results

Promoters increased stake from 72.58% to 74.98% in Mar 2020 qr!

Any takers! Holding a very good quantity!

Anyone want to FLAG my message? Anyone ? Please do flag it.

Thank you!