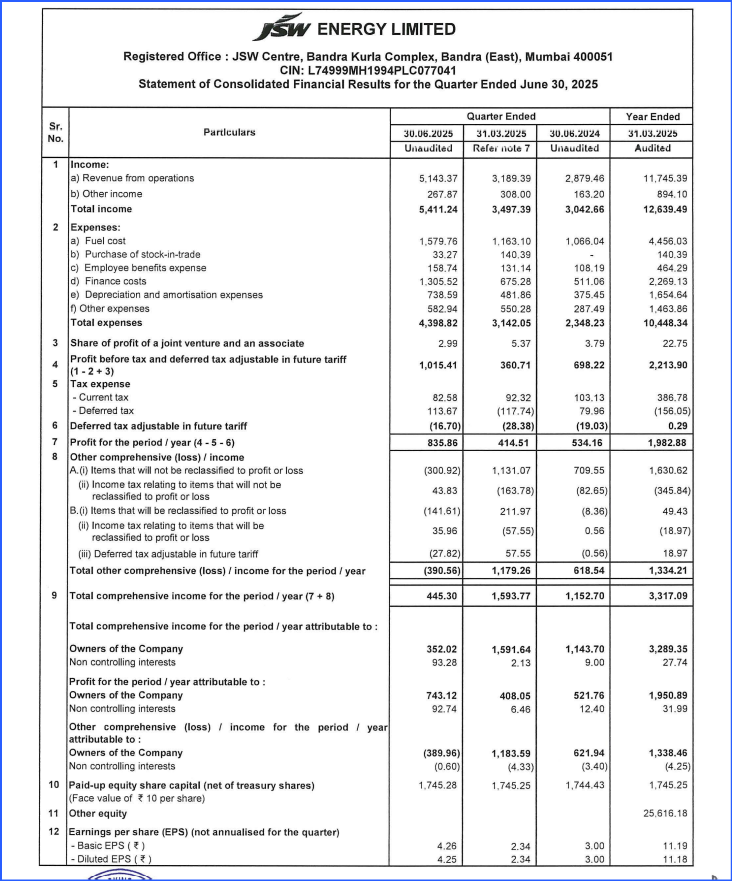

Check quarterly/annual P&L statement directly.

Jsw energy is aggressively doing capex for FY 25 and upcoming year.

Even they bought ksk mahanadi through nclt route and acquired O2 power last month.

Interesting times ahead for the company and investors.

Surprised to see this thread is so silent, when so much of things are happening in this company. With the good track record of management. They always try to over deliver on there talks.

Some upcoming projects -

Soon they will be starting 1gw of solar module for there captive use.

In couple of months there green hydrogen plant will be online.(Pilot project)

Seeing the growing demand for electricity I think JSWENERGY could be big beneficiary.

There capacity after the acquisition is expected to touch 14gw (till May) which is near to double from last year(7.2gw)

And there BESS project expected to start giving returns from upcoming summer.

Disc. DYOR.

Add more to this let’s discuss for better understanding.

3 Likes

one must go through O2 power linkedin profile they regularly update on there new orders, hirings, and commercial start of wind, solar projects.

Management of jsw energy guided that once the acquisition is completed they will get 1500cr of ebitda (which 30% of current level) in there book from very first day. And once all the projects comes online they that had given the target of 3750cr of ebitda(from fy27). These doesn’t include recently BESS orders.(Aprx 1GW).

And in my point of view parag sharma, ceo O2 power. Is very knowledgeable and will lead the company to new heights.

1 Like

Morgan stanley overweight on jsw energy with base price target of 545 , and bull case target of 1008.

Some key highlights -

Ebitda cagr of 24% over fy 24-28e (even without considering ksk mahanadi and bess)

Renewable ebitda to grow at 52%

Though debt to increase due to expansion in both organic and inorganic way, but it’s manageable as projects are fully ppa signed.

The stance is overly aggressive, as per ICRA rating rationale, The company is exposed to execution risks such as delays in land acquisition and transmission connectivity, as witnessed in the recent past for few projects, pertaining to the significant ongoing debt-funded capacity expansion of ~8.9 GW, entailing a total cost of ~Rs 55,000 crore (excluding storage projects). Net debt/OPBITDA jumped from 2x in FY22 to 4.5x now. they are foraying into everything from BESS, Hydrgoen to Pumped hydro. the current OP is around 5k and interest expense is around 2k, interest coverage post acquisition of O2 and KSK , i’m yet to go through,

As both the acquisition are in running stage so ofcourse op will increase once it is done.

Ksk op 2400 around (excluding 1.8gw which will take 2.5-3 years to come online)

O2 op around 1750 (once 2.3gw comes online, june’25)

Even if you take 8.8% as interest cost for the funds they borrow to buy both these acquisition then too they will be able to get good bottom line.

Here is the attached file for your reference in FY 2023 ksk generated 620cr of np and op of 1900cr aprx.

And during concall management said it was 2400cr for FY 24

1 Like

Currently they are having dual aggressive management O2 power+ jsw energy.

On top of them we have sajjan jindal.

Good times ahead, expanding agressively.

Small tender win for jsw energy but at good price. Company moving fast towards bess project. The game on bess could be interesting and big one.

Capacity added till March for this quarter stands at 159mw total capacity 8400mw.

(Approx 18% increase yoy)

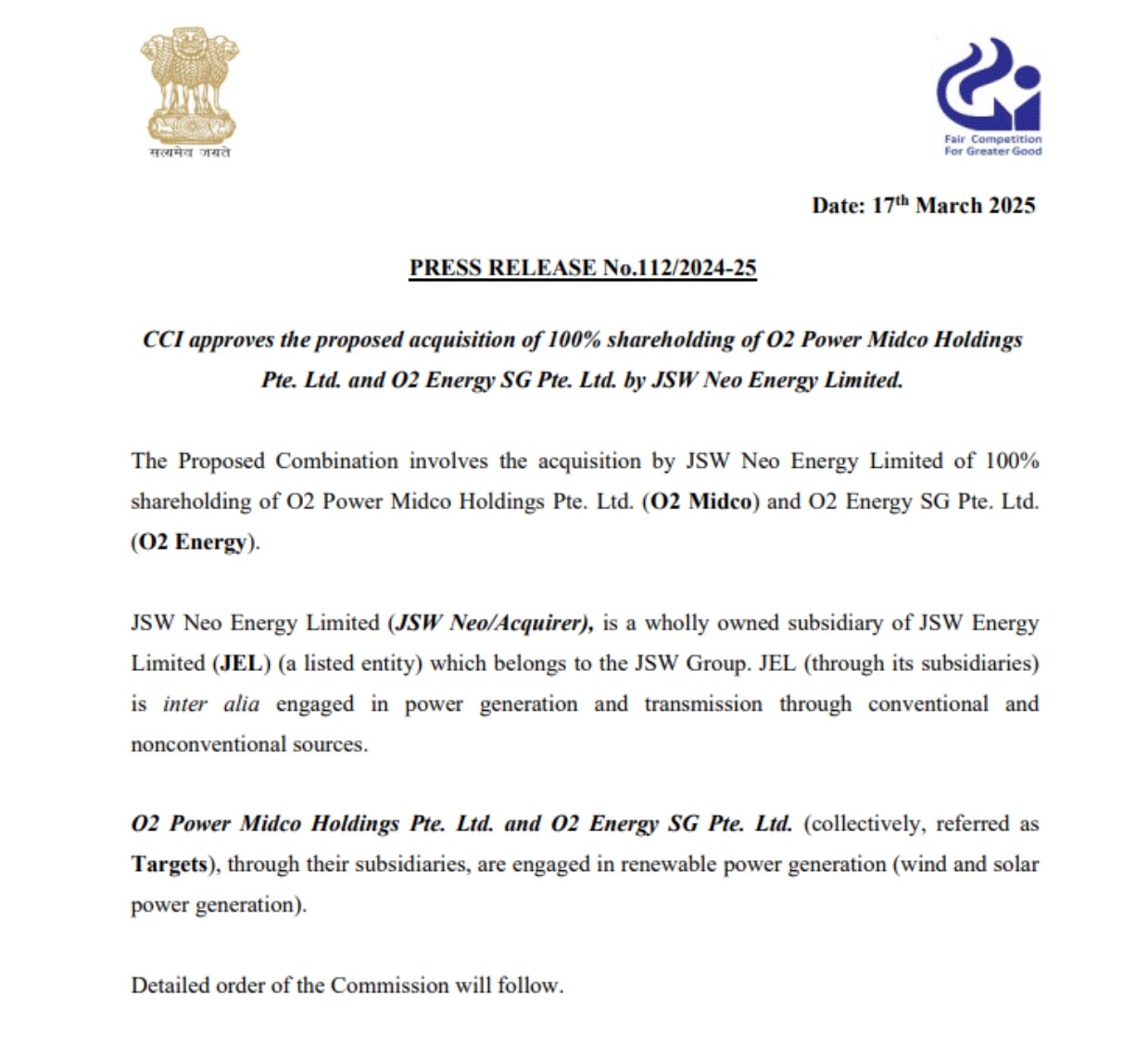

The wait is over… Got CCI approval, max it should take take a month from here to complete the acquisition.

The next is O2 power.

Interesting to see how the plan roll out…

1 Like

JSW energy news:

1 Like

JSW Energy Gets CCI Nod for O2 Power Acquisition! !

Another acquisition will be completed soon.

Total operational capacity as on 31st March could be around 12000mw.

After this I am looking for the wind and hydro projects which will get operational soon.

Till June they said to touch 14000mw, hope they come near to that.

Jsw energy is fully ready to get benefitted from hotter summer.

Even the DAM is increasing with demand. From this quarter the result should starts picking (Q4’25)

3 Likes

The total capacity as on March 31,2025 stands at 10.8 gw against 7.2 gw at end of 2024. Almost 50% rise. And soon O2 power acquisition going to complete may be in next few weeks. That will inch capacity towards 13-14gw+ till June 2025

Energy generation sector would not be affected by trump tariff in direct way.

For short term many trigger are there such as gdp growth, hot summers, and as AC demand is increasing generation companies stock is going to be benefited.

As per iex in March trading volume saw 29% increase so that is clear a uptrend in usage of electricity.

The power demand for March increased by 7% yoy

With jsw energy focusing on increasing capacity organically and inorganic way must keep on radar for short to long term.

3 Likes

O2 power acquisition completed almost a quarter earlier than expected.

Total generation capacity stands at 12.2gw.

This will inch towards 13gw till June 2025.

Looking at the summer weather data and heat wave news on daily basis from different cities across the india, as per me this could be a perfect short - mid term bet.

3 Likes

Co looks to be in a hurry with big acquisitions( o2, mytrah, ksk ) and big announcements ( wb thermal project, UP pumped storage, module manfg and even wind blade mangg ) apart from regular organic solar + wind projects…

Can they execute so much together???

1 Like

Most of acquisitions are already generating cash flows (which are going to be improved with some more capex) from which they can easily service debt and increase profitability.

3 Likes

The first quarter with acquisition is playing well. Beyond expectations

Many more to come.

Expecting Fy 2026 to end at ebitda of 10000cr and eps of more than 18.

Cards playing out well

3 Likes

JSW Energy will deliver record-breaking Q2 results with all-time highs in revenue, EBITDA, and PAT. Supported by its robust business prospects in renewables, hydro, and thermal expansion, the company is poised to cross the near-term 550–600 hurdle and achieve new lifetime highs in FY26.

Available at 27-28 pe multiple on forward TTM basis.

Plus soon there green hydrogen and green ammonia business to get commissioned.

Expecting there capacity to grow at CAGR of 22-24% till 2030.

In the current scenario, JSW Energy stands out as a safe bet. With tariff certainty in place and around 92–93% of its revenue locked under long-term PPAs, the company enjoys strong cash flow visibility and financial stability.

4 Likes

It’s result day expecting 40-45% growth on PAT level.

Posting my full estimates for study purpose -

Expected fig. (Q2 2026)

Revenue 5800 cr

Ebitda margin 55-58%

Ebitda 3240 cr

Other income 200cr (expecting more as jsw Steel moved around 8-9% in previous qtr but let’s take on conservative side)

Depreciation 750cr

Interest 1320 cr

Pbt 1370 cr

Tax 270 cr

Pat 1100 cr

Let’s see what’s in result just my point of view on result

Post result

The expectation was little higher but due to barmer plant which went into maintenance the earning got little less than my expectations,

But the margin surprised on higher -59%

Interest and depreciation came 100 and 50 cr higher respectively.

The Ebitda near to 3180cr is ![]()

Cash profit 1512cr (higher 27%).

In Q3 Company will start green hydrogen and ammonia plant(expecting in November)

Battery assembly plant is also expected to started in month of Nov-dec 25

And above all they are targeting 15 GW at the end of FY 26.

There CWIP is near to 12kcr

Net debt /equity 2.1

Net debt / ebitda 4.5 (excl. Cwip debt)

Overall a great business with less volatile earning.

1 Like

JSW Energy is definitely going to rally from these levels.

Thesis is really simple

Capex is front loaded. Investments have gone 6x in the last 4 years

Revenue has not moved similarly.

Project Finance 101: If IRR > ROC → value accretion

Add the extra EPS squeezed from Accounting 101 which is Depreciation benefits.

Mgmt has emphasised on it’s Hurdle Rate discipline of selecting projects with mid to high teen IRR

The rally will catch a lot of investors by surprise.

1 Like

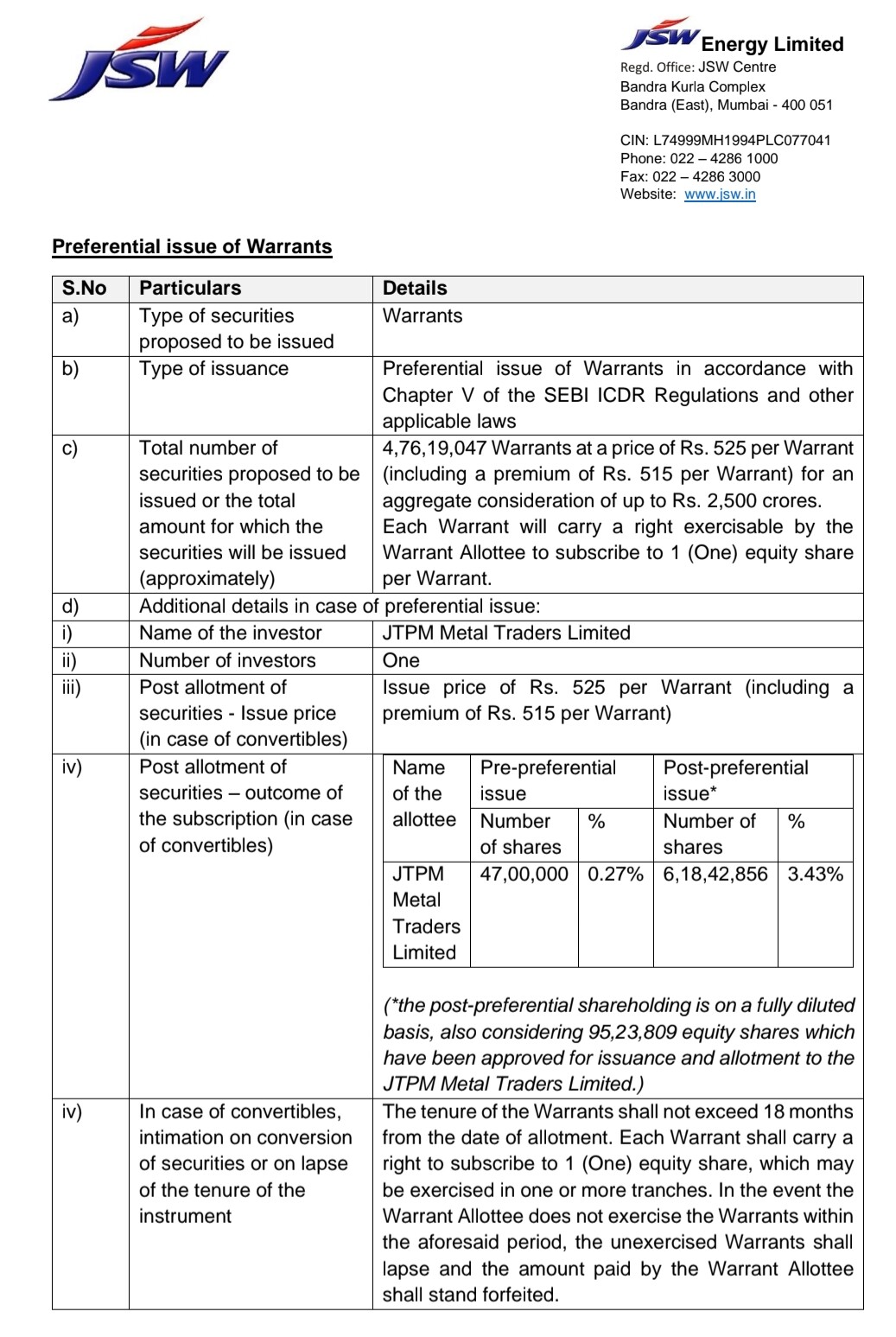

Promoter infusing 3000 cr at 525.

Plus they are going to raise upto 10k cr through qip or private placement.

The management is aggressively looking for good opportunities in market and looking to complete there 3.0 target of 30gw and 40gwh battery storage by 2030.

Keep and eye the re rating after infusion of capital by promoter plus a qip could be taken as a positive sign.

1 Like