Had a quick look as saw some job advertisement and growth plans of the company. The past has been slow in terms of topline growth but the bottomline has done pretty well due to consistent margin expansion. At a PE of 5 and div yield of 5%, the stock may be interesting IF they can deliver good growth from here. Would be good if we can get some insights on their growth plans.

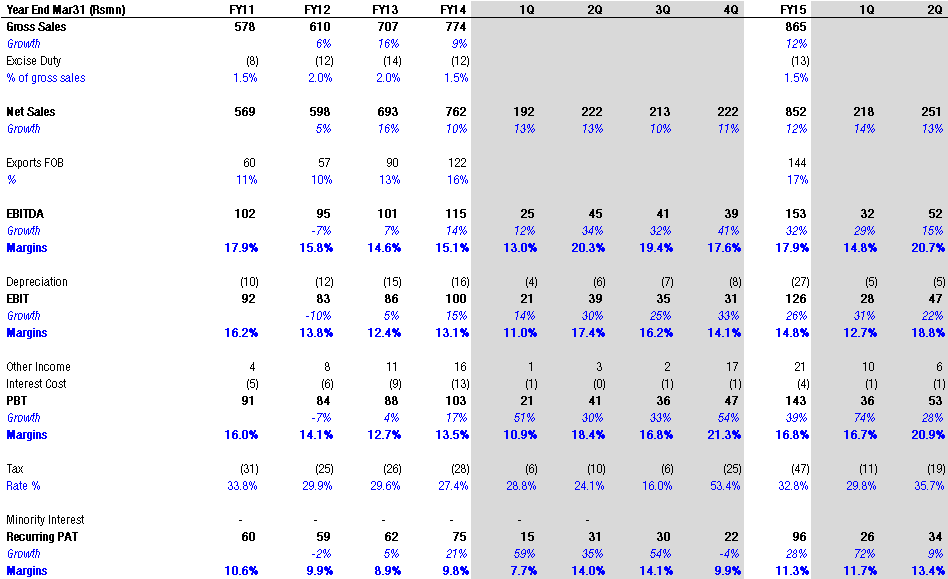

Just announced a fantastic Q4 and also closed Fy15 very well. Dividend yield was superb too as always. The company has also guided for 20% growth this year which is a positive.

Great ROIC and also completely debt free at the moment.

Also the track record of this company is great for the last 5-10 years. Very consistent player and growing steadily away from the market’s radar!

Can you please provide some management interview or conference call link which gives this 20% growth guidance. I have not seen it anywhere. Have you seen note 7 in results. Any thoughts on that

I had called the company regarding note 7 some time ago. This is an old case. The High Court has already ruled in their favour and the company seems confident that even the Supreme court should do the same. The company is tiding over this issue with the NPPA.

Annual growth rate has been impressive from 2014 to 2015. The EPS has grown in excess of 20%.

I have also spoken to many (cannot remember the number also) pharmacists in Mumbai…they all say that Jenburkt Pharmas products are very well accepted by Doctors and Patients. The company enjoys a very good name in the market.

I suggest you visit 5-10 pharmacies in your locality (if in mumbai) and ask for the quality of Jenburkts medicines.

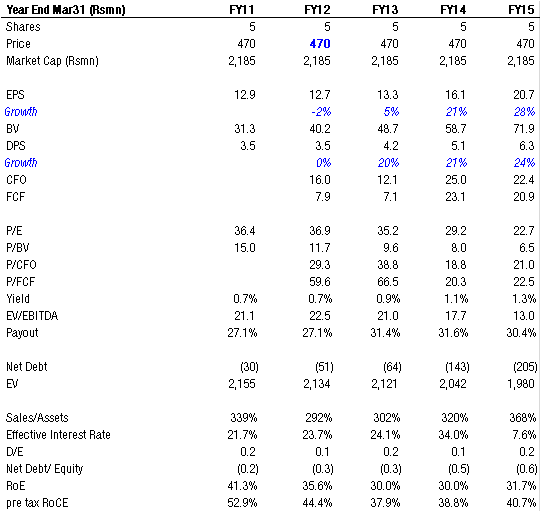

To conclude, I believe the company will continue to grow at 20% for quite a few years just as it has done in the past. They will remain debt free. Enjoy extremely high ROIC and continue to pay impressive dividend (12rs+ in FY15).

On my costing of 130rs/share, my dividend yield is now almost 6%.

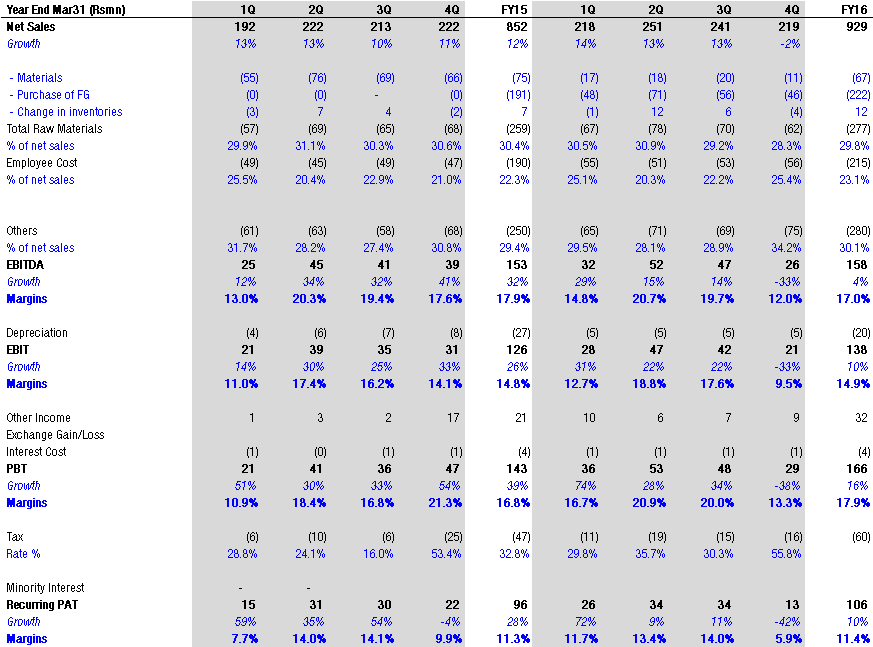

Also, Q4 revenues were up 12% YoY and Profit before tax (PBT) was up an incredible +55% YoY.

Its difficult and extremely rare to find an 175cr market cap company with zero debt, extremely high ROIC, great track record of last 5 years, superb dividend payout & a superb growth outlook.

Has anyone looked at Jenburkt recently. Reminds me a lot of Anuh Pharma. But with higher EBITDA margins

— Market Cap Rs211crs

— RoEs of 30%+ for the last 5 years

— Net cash company)

— Pays out 30% of profits out as dividends

— Trading at FY15 P/E of 23x. 1HFY16 PAT is up 29% YoY

—83% of business is domestic and 17% is exports.

I have used a couple of its products namely powergesic gels and tablets and one derma product. Very effective products.

Yes, this is an excellent company with a strong domestic franchise. Valuations are very attractive. Growth is steady. Debt free. Asset light. Prudent management. No dilution ever. Margins increasing each year.

I would say Jenburkt has a huge runway ahead. Probably will see 4 digits in a couple of years.

Interestingly, I started looking at this stock some time back when it was close to Rs350. I liked everything except what you pointed out (@Marathondreams) . I looked at BSE Stock Share Price | Get Quote | BSE and wondered why promoter stake is reducing. So I stayed away from the stock.

Stock moved from Rs350 levels to Rs450+ levels and results post that were also quite good. This time around I looked at a longer time frame to see what happened to promoter holdings. See below it has been increasing steadily over longer term. I realized there is one individual promoter Ketan H Bhuta who has been selling whereas other promoters have been buying. This gave me the courage to buy. Of course I would have loved it if no one was selling.

Hi

Was going throuhh the financials, while other things look good including profit margin growth, divident payout etc, but the Sales growth over last 5 years has been 10-12% average. Just wanted to understand for a small cap like Jenburkt, should the growthe be higher ?

Does anyone know what happened in the 4Q results. YoY sales declined marginally which led to PAT decline of 42% YoY? Is 4Q a one off or is there a problem?