Decent Q3

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e5ecf799-52d5-4ba7-8eb8-a731b6355ce0.pdf

Decent Q3

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e5ecf799-52d5-4ba7-8eb8-a731b6355ce0.pdf

JBM Auto leading contender to acquire controlling stake in SML Isuzu.

Recent run in stock price may be attributed to this news.

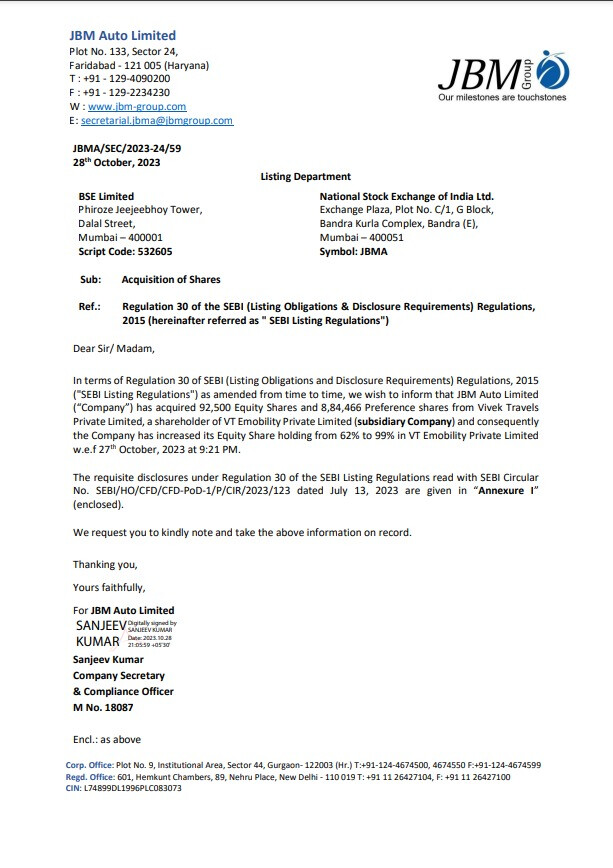

JBM Auto - Acquisition

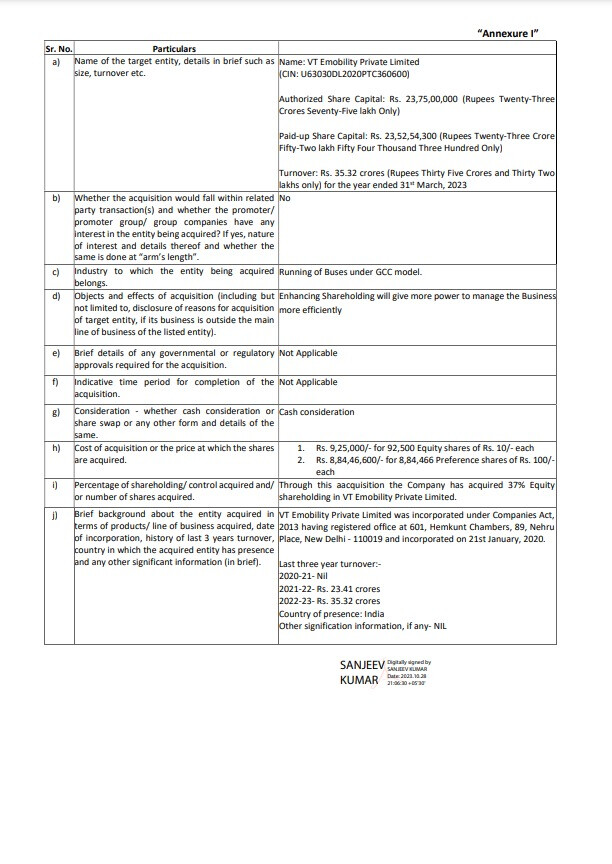

JBM Auto Limited has acquired 37% equity shareholding in VT Emobility Private Limited with the following financial details:

Brief Background of the Entity Acquired:

Last three years’ turnover:

2020-21: Nil

2021-22: Rs. 23.41 crores

2022-23: Rs. 35.32 crores

Presence: The acquired entity is present in India.

JBM in the last couple of quarters is focusing majorly on exports market as well. It is actively showcasing eBuses in Europe and MENA and according to some reports[1], Solaris in which JBM has majority stake was the largest manufacturer by sales volume. Germany has recently invested 53.4 millon euros to procure EV buses[2]

Extremely well written. I would like to answer some of the questions you have mentioned in your post.

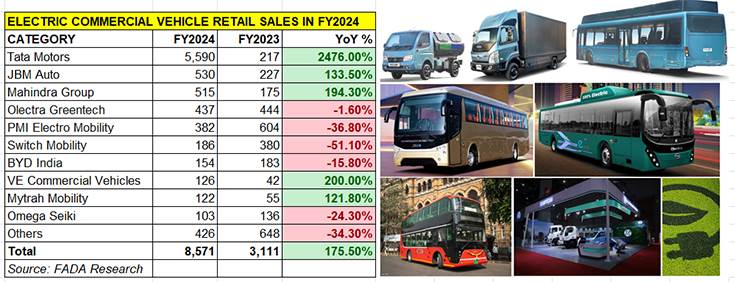

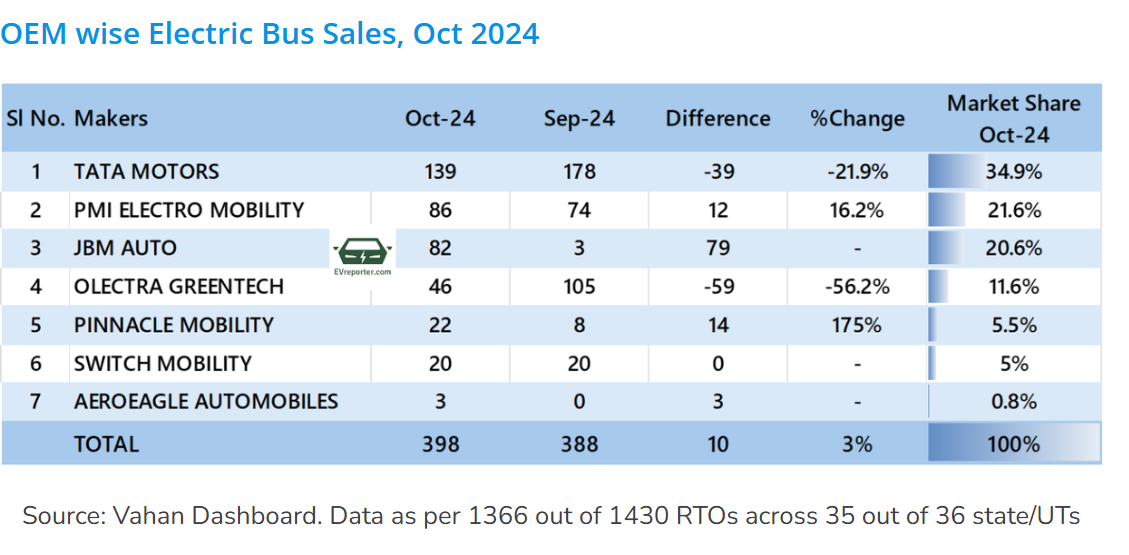

Market Share: This data can be directly obtained from Vahaan database. Attached is the data from the last fiscal year. Similarly, month on month data is also available, just search “EV sales May 2024”

Price Point: Calculating this is challenging due to the various variants available. However, according to CESL’s latest tender, the average price is around ₹1.92 crores. For more details, refer to the source : https://www.convergence.co.in/public/images/procurement/March-2024.pdf

Will try to get more information on L2 bidders and pricing on this.

I am also concerned about the lack of commentary from management, especially when you compare it to Olectra. But then again, Olectra’s management has a track record of missing their estimates by a big margin, which is also worrying.

New Order : 1,021 [One thousand twenty one] Electric Buses and development of allied electric and civil Infrastructure. Approx value - Rs. 5,500 Crore

Orderbook - “These e-buses will clock over 32 bn+ passengers e-kms. With this order, the company’s robust order book now stands at 11,000+ electric buses in various stages of execution”

More details at: https://www.bseindia.com/xml-data/corpfiling/AttachLive/80e0a622-463e-435a-b541-840bf616a80d.pdf

Related news.

Disc: Invested about 2.5% of Portfolio value at higher levels.

Markets looking bright on possible orders

Invested: 3% in JBM & 2.2% in Olectra

Today under the PM e-drive scheme, electric trucks got a subsidy (this was after consultation with the industry). Any idea if JBM plans to participate in this?

Olectra has truck manufacturing capabilites, but didn’t rollout recently due to bus backlogs

My accounting is a little wonky - but all the order’s from state governments have come to the JV - JBM Ecolife Mobility Private Limited, which used to be a wholly subsidiary. But since March, 2024 it is a JV 83% JBM Auto, and 17% Nishant Arya. In what way does an 83% ownership qualify for a JV sort of a treatment? Isn’t it still a subsidiary? And they use the equity method for accounting which means the revenues for the subsidiary don’t come up in the income statement, only the profits/loss come up as a line item in the P&L