If I am not mistaken, TARIL is one of the customers of Jaybee. So, it sounds like going forward TARIL will source from Posco (acquired company)??. If so, what could be the impact to Jaybee then?

I don’t think TARIL is a major customer of Jaybee, as its name is not seen in any of Jaybee investor presentations. . I think TARIL was buying mostly from Posco Poggencamp which they decided to acquire as a backward integration. So this transaction should not impact Jaybee directly.

3 Likes

I came up with TARIL from their recent investor call (I may be wrong). Also noted from their call is few unlisted and unorganized players as their major competitors. Apart from this, Vilas Transcore’s (Listed) expansion is gearing up for supply to higher KV class transformers.

1 Like

Sir, I want to know how JBLL process crgo steel to remove impurities and maintain quality standards of crgo steel for making its products. As this processing of crgo steel is most important step to differentiate JBLL from other small player in same business. Pls give your valuable insights on this.

1 Like

They don’t manufacture steel. They just process it (mechanical processes like slitting, cutting, sizing, maybe some coating etc). So JBLL cannnot remove any impurities in steel

Please see their manufacturing process as below

1 Like

Amba enterprises is one more player in listed space but from the OPM margin they seems to be more in trading business.

I believe Jaybee will easily do 20 crs PAT in 2H which implies FY25 PAT of Rs 34crs. At current market cap of Rs 591crs the stock trades at 17.3x with minimum growth of 30% in FY26 on expanded capacities

3 Likes

Can any of the transformer mfg companies backward integrate to start producing crgo laminates themselves ?

Is the unit economics favorable here for them to do so ?

what is the % cost of a core vis a vis the cost of a transformer ?

Any specific reason for the large fall today or is it just bear market?

Jaybee and Vilas are at low-end of manufacturing procees. Market is realising it off-late as there’s nothing extra-ordinary in their products.

2 Likes

Jay bee laminations 19th March Kaptfy analyst meet notes -

Capacity -20000 MT

Approval for 420 kv to come soon , pgcil Pproval will be available post this, should be better margin & volume wise , vilas transcore direct competitor increasing capacity 3x

At 80% odd capacity utilisation monthly

Capex for 9000 mtpa is 15 cr & can do 180 cr revenue generation at margins of 12-13% ,

Fy 26 crgo 16000 mtpa, @ 300 per tonne next year should be 500cr topline , exports to be 10-15% if buisness

Fy 25 volume 12.5 MTPA

For going upto 24000 MTPA van do 4-5 cr cost by fy27

3rd generation promoter

In 2015-20, capacity was 11000mtpa, however utilisation was close to 40-50% & margins dropped, hence not expanding very aggressively, expansion is planned only when more than a quarter co sustains 80% kind of utilisation

Orderbook at any given point of time does not exist 2-3 months

Payment terms for distribution clients is 30-69 days & power 60-90 days, currently not facing any delays

2 Likes

Shilchar (One of Jaybee’s main customers) has reported blockbuster results with guidance for robust growth going forward.

Transformers & rectifiers India, though not a Jaybee customer, also reported great results with extremely strong guidance going forward.

All of this shows the robustness of demand currently in the transformers space (Jaybee’s 30% sales growth update in December backs this as well).

As one of the lessor discovered names and having had a significant correction recently, Jaybee’s share price could have both factors (Earnings growth + Multiple expansion) in play.

DISCLOSURE: INVESTED AND ADDED IN RECENT DIP.

6 Likes

Thanks sir . Great input.

Agreed, the points you mentioned on Jaybee holds true.

The valuation comfort offered by Jaybee is the biggest advantage since this is not well known name.

Looking at their products the only concern is that they don’t have very big moat. They only cut the metal according to client specification stack them together as lamination and perform testing (please add if I am missing anything). They are easily replaceable by any other player and I believe that is the reason they don’t command or will command a very high multiple.

On the other hand Shilchar gets the biggest pie in the whole value chain. They have technical knowledge how. There are very less competitors who can make idt transformers and moreover make export quality idt.

We know this industry is a long term play. We have to choose whether we want low moat business with valuation comfort or a higher most business with high valuation. If Shilchar continues the recent q4 run rate, it’s valuation is very well justified. Let’s see q4 numbers of jaybee.

At the end of day we are capital allocators, and Shilchar with its very very good return ratios is definitely very tempting for capital allocation.

Disclaimer: Invested, added recently.

2 Likes

Jaybee’s main edge is the valuation comfort, but the business model doesn’t offer much moat, it’s mostly fabrication work that can be replicated easily. That’s why the market won’t give it a high multiple

3 Likes

H2 FY 25 earnings are out and stock has tanked 20%.

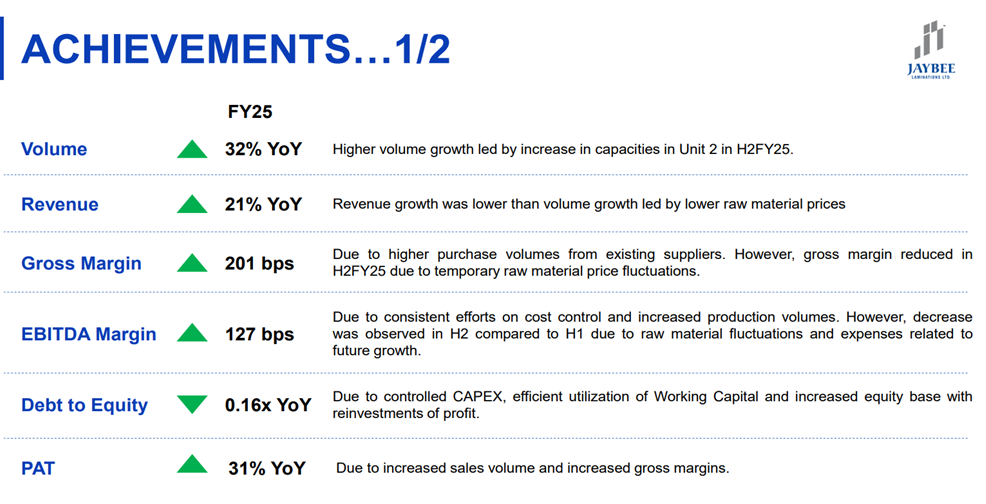

Its seems volumes are up 32% YoY but sales is up 21% only - primarily due RM fluctuations (Materials cost went from 79% in H1 '25 to 90% in H2 ’ 25) clearly indicating RM sourcing/importing challenges and limited or none pricing power company has with clients.

This combined with some of the earlier comments of limited moat in terms of technology employed - at best this appears to be - volume/sectorial tailwind earnings growth play, with current PE at 20x not realistic to expect any re-rating here? Appreciate inputs from who hold and follow.

Tracking Jaybee and Vilas.

2 Likes

Following the recent earnings release, there has been considerable chatter around Jay Bee—concerns ranging from it being a “proxy of a proxy,” to margin compression, cyclicality, and more.

To begin with, it’s important to recognize that the entire sector is inherently cyclical—not just Jay Bee. After several years of subdued performance, the industry is now witnessing a strong demand revival. Consider the performance of transformer companies:

- TARIL has seen its operating margins expand from 6% to 19%.

- Voltamp, which has historically operated with margins as low as 3% and an average of around 10%, is now delivering 20%.

Clearly, the sector is enjoying a cyclical upswing. What sets this cycle apart is the expectation of a longer-than-usual duration. However, it’s worth noting that, as in past cycles, an eventual oversupply situation could lead to margin compression across the board.

As for Jay Bee, management has already addressed the margin impact, attributing it primarily to raw material price volatility. The financials support this explanation. Despite these headwinds, the company achieved its guided EBITDA margin of 12–13% for the fiscal year. Additionally, expansion-related costs weighed on margins—employee expenses alone rose by 45% YoY and 25% QoQ.

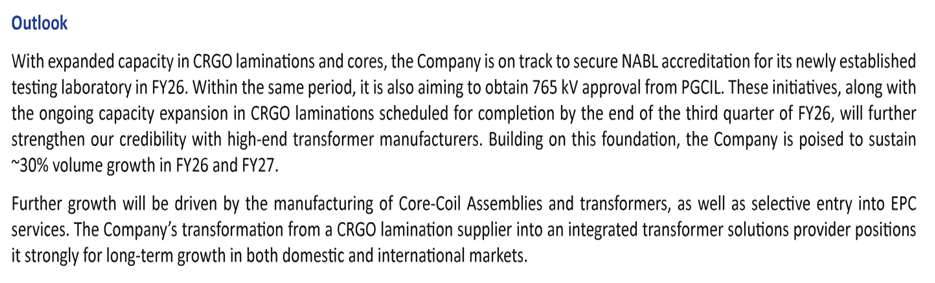

Looking ahead, Q1 FY26 may remain soft, as high-cost inventory is expected to be consumed by May or June. However, management has guided for 30% volume growth over the next two years, alongside a sustained EBITDA margin of 12%. Based on these projections, the stock is currently trading at 10/12x forward two-year P/E, which appears to be reasonable.

In businesses like this, one shouldn’t be looking for moats. Performance is largely driven by the strength and duration of the industry cycle.

7 Likes

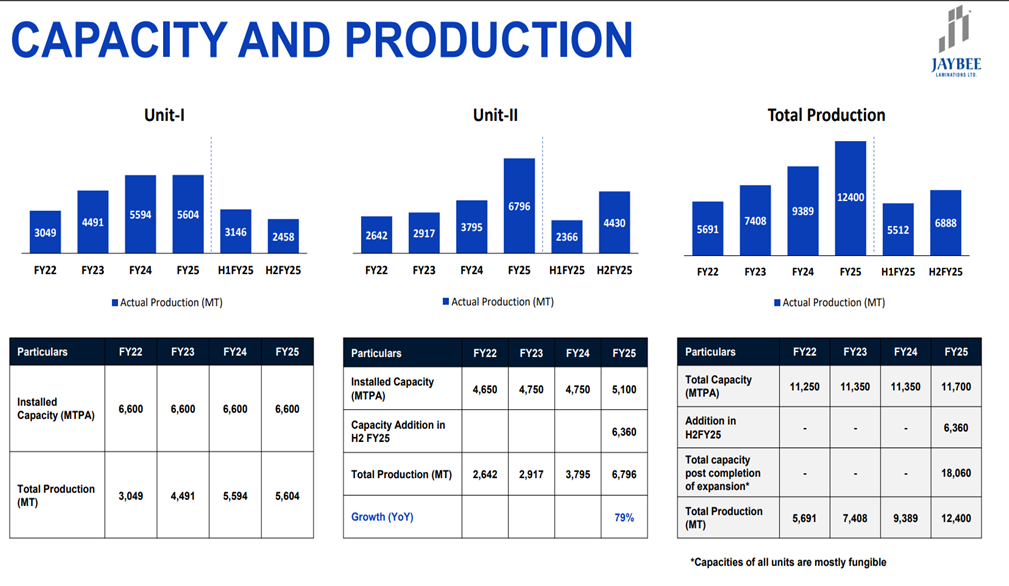

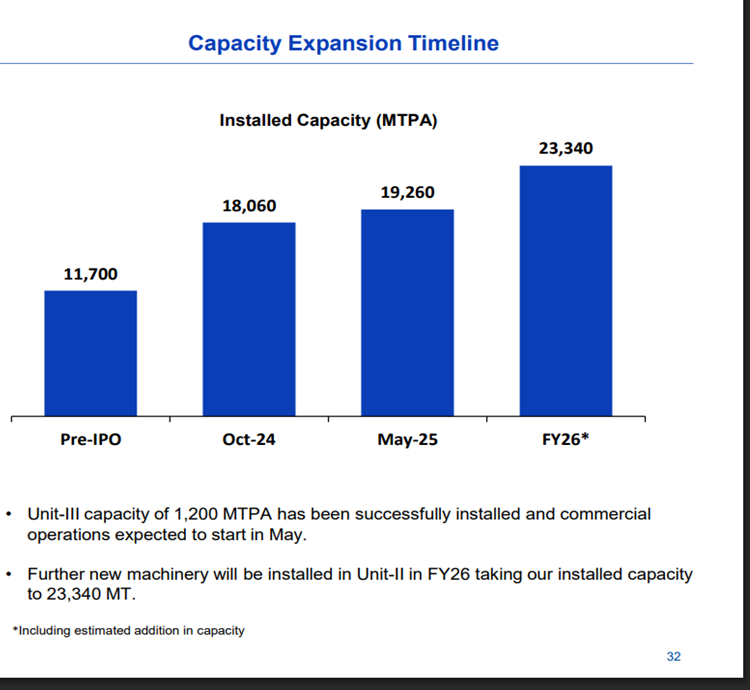

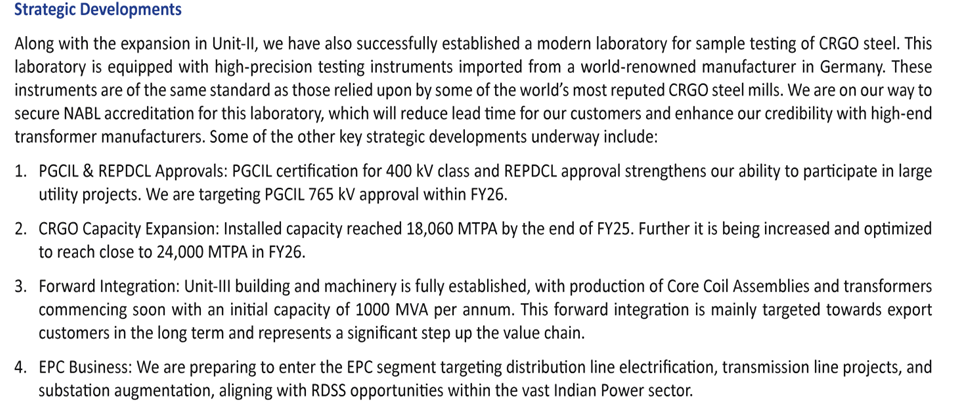

H2FY25:

• Our volumes grew 32% year-on-year, meeting our initial target of 30% supported by capacity additions at our Unit-II facility. We are committed to maintaining this momentum into FY26 with increased sales from newly installed capacities.

• In alignment with specific export demand, we are making strategic investments at Unit-III to manufacture Core Coil Assemblies and Transformers. This forward-looking initiative is poised to unlock the next phase of our growth and deepen engagement with global customers.

• UNIT III Area – 3,663 sq meter Capacity – 1,200 MTPA (starting in May 2025)

•

•

• We also got approved for end user - REPDCL for supply of CRGO cut laminations in March 2025

• Addition of new Unit 3 for future growth Trial runs were started within 4 months of inception and commercial operations expected to start in May

•

•

• Gross margin reduced in H2FY25 due to temporary raw material price fluctuations. Decrease was observed in H2 compared to H1 due to raw material fluctuations and expenses related to future growth.

• Debt/Equity ratio = 0.16

• Notably, we onboarded several new customers during the year, who contributed approximately 12% of our total sales in FY25.

• Our revenue mix is increasingly driven by our core offerings - assembled cores and cut laminations. • There is a consistent decline in the share of other lower-margin products underscoring our focus on specialized, value-added solutions. • Within such value-added products, we are further aiming to increase the share of power transformer cut laminations.

•

• PGCIL Approval for 400 kV class in March 2025 led to addition of orders worth ₹17 crores within April. Further orders worth ₹15 crores are under negotiation.

• Targeted Customer Approvals by FY26 To further enhance our market access, we are actively pursuing approvals from reputed end users such as - • NTPC • Torrent Power • PGCIL (765 kV class) These approvals are expected to significantly expand our opportunities in the domestic power transformer segment.

•

• Advancement in Quality Infrastructure We have successfully established a state-of-the-art CRGO testing laboratory at Unit-II, which is now fully operational. • We aim to secure NABL accreditation by the end of H1FY26. • This in-house capability will reduce reliance on third-party labs, thereby minimizing lead times and enhancing delivery efficiency for existing customers and attracting new customers.

• New Initiatives:

In response to evolving customer needs and market dynamics, we are forward integrating into core coil assembly and special application transformers at Unit-III.

• These products will not only complement our existing offerings but also enable us to tap into new customer segments. • By leveraging existing customer relationships and infrastructure, we aim to add value across the supply chain and deepen our engagement with the power sector ecosystem.

CONCALL NOTES:

• VALUE CHAIN / PROCESS: Our products include Cut Lamination, Slit Coils, and Assembled Cores. Slit coils are produced by the first process, which is slitting. Then we produce cut laminations by the process of cutting on automatic CNC lines. It is designed as per the customer’s requirements and needs. Every order is tailor made. And then the final step is assembly, which results in assembled cores, which is a labour-intensive process.

• MARGIN FLUCTUATION REASON: H2 saw a decrease in gross margins considerably. That was primarily because of raw material price fluctuations that led to decrease correction of pricing in the market, which was also passed on to customers through the selling price, which led to decrease in gross margins. Similarly, EBITDA margins were affected because of that as well as some expenses related to the future growth.

So, we have seen in the past also such volatility in the raw material prices. However, this time, it was a slightly different kind of volatility, because it was based on some of the mills not getting licenses. So, when these mills did not get licenses in say H1 of FY '25, people like us had to buy raw material in advance and we stocked up. So, we stocked up raw material, and plus, we were on a growing spree, because we knew that H2, we would have to increase sales. We would have to acquire new customers. So, for that, we needed raw material. If we did not do that, at that time, it was a decision that we had to take. If we did not do that at that time, we would have been stuck with no raw material and no sales or say limited increase in sales, which is what we did. And that was also visible in the value of the raw material at the end of September, which was to the tune of ₹90 crores.

And why it was higher priced is because in December, all of a sudden, those mills were again introduced and licenses were given to them. So speculatively, the market became quite chaotic. and some of the customers even postponed their orders, and some customers started requesting for better prices because the raw material prices were lower. And we had inventory, which was in the month of October, November, December at a higher price. So, it was a trade-off between sales and margins at that particular time because we were increasing sales.

Now, we have almost consumed all of that raw material. So, we have inventory, which is high priced, which will be probably finished by April, May and probably just the beginning of June.

• GROWTH GUIDANCE: We are planning FY '26 and FY '27 volume growth of another 30%, similar to FY '25. Our monthly run rate has already been achieved compared to the targets that we are planning for FY '26 (Already doing 1300-1350MT monthly run rate)

• MARGIN GUIDANCE: The margin guidance is 12-13% on a long-term basis, which we have more or less achieved on a full-year basis.

Going forward, if there is volatility, we will see some swings in the margins, but we believe that on a full year basis, we will still be able to achieve the previous guidance of 12% to 13%.

• FORWARD INTEGRATION INTO CCA AND TRANSFORMERS: So, we have been recently getting enquiries from export customers for core coil assemblies and transformers that we will be producing or starting in Unit III.

We are already in the process of signing an NDA with the customer abroad. So, we are confident of that kind of business coming in from there. So, with that, once we start white labelling transformers for export customers, we have more opportunities to tap into new customers.

Can we expect any orders with respect to manufacturing of transformers in this year, or is it like a two years plan or a long-term plan? So, the customer that we’re talking to has given us a commitment of about ₹15 crores, ₹20 crores on an annual basis. So, we are expecting say on a conservative basis, we are expecting orders of at least ₹3 crores, ₹4 crores in this financial year because the machineries have already, I mean they’re already being ordered and we are hoping to set it up within the next two, three months.

So how much transformer manufacturing revenue are we expecting in coming years? Mudit Aggarwal: For this year, we are not expecting much. Depends on when we start, and probably, we will get not more than six, seven months of production and depends on the availability of orders. By next year, we will definitely try to move up and aim for a number of at least ₹40 crores, ₹50 crores.

And plus, we will have to work up our way, with respect to other customers to create a goodwill, create a brand in the market as far as transformers are concerned. So, it will take some time.

It is at a better margin product, but the volumes might not be scalable to the nth degree.

• CAPACITY EXPANSION: We are already being able to achieve about 80%, 85% on a monthly basis so we are currently at a run rate of about 1,300- 1,350 metric tons, out of say a capacity of 1,500 tons on a monthly basis. So, if we are already achieving that, we are also confident of the demand. Because of which, we have already placed orders for the new machinery, which will be placed in Unit II, which will take us to a capacity of about 23,000 tons. And thereon, we might be able to expand, but currently, we just have to work up to the next two years taking up our quantities to at a growth rate of 30%. So, for example, from 12,400, we will be eyeing about 16,000 tons, and the year thereon, we will be eyeing 20,000 tons. So, for two years, we are set with these capacities.

Once we start core coil assemblies and transformers in Unit III, we won’t have the space to do 30,000 tons. We won’t have the space to additionally install, 6,000, 7,000 tons. So, we would have to look for a completely new greenfield project.

• NEW CLIENTS’ DETAILS: So essentially, we added new clients like Bharat Heavy Electricals Bhopal. So, I’ll just give you a small example. Till September last year, where we were present in mostly up to 220 kV class, we were doing business with Bharat Heavy Electricals Jhansi unit. But Bharat Heavy Electricals Bhopal does 400 and above. So, after the new capacity was installed, we participated in tenders because we were not allowed before that to participate in the tenders. We participated in the tenders and we got orders from them. So that was a big chunk. And then there were a couple of export customers also that got added. Then there was another company by the name of ECE. ECE has two units. One is in Sonipat, where we are already working. Then one is in Hyderabad. The Hyderabad unit was got added in H2. Besides that, there would be all small customers mostly in distribution segment.

• HIGHER KV ORDERS: Going forward, we already have orders of PGCIL worth ₹17 crores and another ₹15 crores are lined up. After that, we will be searching for new customers. We are already in discussion with new customers. Some of the customers have already planned their internal audit of the plant, the facility, which is planned in May. Once those are through, we might be able to get business from there as well. So, we are hopeful of, we will definitely start executing from those kinds of orders starting May. But it is hard to pinpoint on the volume or the percentage of volume that might come from there.

For FY '26, we would be targeting about ₹100 crores of 400KV orders. When all the capacities are installed, we would ideally want to do about, we would ideally want to target about ₹15 crores of business every month.

• ON HIGHER MARGINS IN HIGHER KV PRODUCTS: If we have already now started supplying 400 kV, and at some point, we’ll have this 765 kV also, how much incremental margin can these produce over our traditional EBITDA margins that we are currently looking at 12% odd, because your 12% to 14%, does that also factor in the extra margin that these higher kV classes can produce? Mudit Aggarwal: Yes. That the blended margin includes 400 kV class orders. Let me first, tell you that the 765 kV class, it definitely opens doors for us, but there is more demand in 400 kV class compared to 765 kV. 765 kV orders are very limited in the market. So, 400 kV class was the main aim that we got. Secondly, the margins are generally I would say in terms of percentage, it would be about 2% to 3% higher on a general basis. But there could be difference in supply and demand gaps with respect to certain grades. For example, a certain grade is not available and that particular grade has to be approved by PGCIL also. If somebody does not have that grade, we are able to command a premium. So based on that, the margins can go up to even 3%, 4%.

• ON TRANSFORMER COMPANIES BACKWARD INTEGRATING AND JAYBEE’S ADVANTAGES: So, we have seen in the past that a lot of transformer manufacturers have tried or successfully done backward integration. For example, BHEL is already backward integrated, but still it buys a large chunk of cut laminations from the outside market. Then some of the players who did backward integrated, they discontinued the CRGO manufacturing operation because they were not able to deal with the inventory, the timelines and the inflexibility of selecting different grades based on their designs.

Then the third aspect comes where power transformer manufacturers have to in a power transformer, if say the core required is say of 100 tons, then there will be additional scrap or say, WIP generated to the tune of 25 to 30 tons. That cannot be used in a power transformer. That has to be used in distribution transformers. And we have a variety of customers where we are able to churn that inventory quickly, which is where we sort of got on a back foot in the last half year also our WIP had actually substantially increased, because we focused on power so much that all of that WIP that additional 25%, 30% of WIP started piling up, and we did not have enough distribution customers. So, it’s a matter of optimization that we want to do, and that is where our skill lies. So once that optimization is complete, I think then we will be able to very gladly and healthily say that we have achieved the required growth.

Why the transformer manufacturers outsource such a critical process or critical component is because like I said, many have tried backward integrating, but CRGO has many grades. The inventory is in very a lot of different forms. It has, big coils. It has small coils. It has laminations. It has sheets. It has a lot of different things into it with respect to the inventory. So the inventory management and the grades that you have, the grades that you carry in raw material actually matter quite a lot, which is where some of the transformer manufacturers would ideally say, I don’t want this headache. You take this headache, and you manufacture this for me and which is why to when we go to the power segment, the criticality increases so much that the customer has stickiness for certain suppliers of CRGO cores.

• CRGO STEEL PRICE FLUCTUATION: So, my average purchase price in say starting of the year was about ₹190 to ₹200 per kg. And it went up to about ₹255 say any October, November. Eventually, it started going down, and today, it is at around ₹230. ₹235. So, there has been a big fluctuation.

• ON IF THERE CAN BE OVERSUPPLY SITUATION IN NEAR TERM: All the industry players in laminations have doubled their capacity. Whether it’s you who’s tripled, Vilas Transcore is doubling, or there is Mangal, which is basically tripling. Are we entering a phase where margins actually go back to pre-COVID numbers, which were like 5%, 7% EBITDA margin in a very short span?

I think, pre-COVID numbers were low or say margins were low primarily, because of the rigidity in supply chain of the entire transformer industry. I mean, at least I can say from my own experience of say 12, 13 years and we’ve seen different cycles, but the cycles have not affected those margins as much as the customer demand has affected it. So, the customer demand was not there.

So, I mean, your guess is as good as mine. We can be going into an oversupply situation. I cannot say that for sure. On the risk of not being misquoted, I would just like to say that we are going on a stable basis. We want to cut that path, and we would eventually try to reduce the debt, because we know that, if there is a cyclicality in the business in that sense where the supply is greater than demand, the only thing that protects us is being stable and cautious in our approach. We have seen those cycles, and we will continue to do that.

Had we not been confident of achieving the run rate that we are at, we would have not gone for buying new machines that is going to take us to say 23,000 tons. But once that is through, and we are confidently able to view or say, have that vision that FY '27, we are achieving 20,000 tons, it is very difficult to say that we will go for a further capacity expansion as of now, which is why because that risk of oversupply and demand, a difference in demand, definitely stays there. Nobody knows that even that kind of risk is also valid for transformer manufacturers for all that we know. Because transformer manufacturers are also expanding capacities. Some of them are doing 3X, 4X capacities. So eventually, transformer industries might also see that kind of a slump. But what we want to do is we want to focus or diversify into export customers. Those are small transformers, completely different from the segment that we supply cores in, but the core still goes in that. So, we are confident of making those transformers. And maybe if we have a portfolio of these kind of products, we’ll be able to sail through any risks and problems that we might face in the future.

And with respect to a question already asked, so do we see any demand slowdown? Because I said because there might be a situation of oversupply ahead. So, do we expect a continued demand ahead? Mudit Aggarwal: Demand seems to be strong at the moment. We don’t see any issues with the demand part, which is why we are quite confident of achieving the quantity target.

• UNORGANIZED VS ORGANIZED, POWER VS DISTRIBUTOR TRANSFORMERS: So, at least from my experience, we’ve seen that the industry has always been in a mostly unorganised state, and it has to be looked at through different segments. So, distribution, power, specifically. Distribution segment will continue to have N number of CRGO manufacturers. The business is such that, it is very easy to enter and put up a capacity and start procuring raw material and start supplying to transformer manufacturer.

The key lies in consistency of supply and quality. So, basically, the customers who require consistent quality and are short of time, basically, the ones who are working on in volumes, we try to approach those customers, at least as far as distribution is concerned.

With respect to power transformers, again, that segment the number of players is little. They are lesser than the distribution segment. They are about six, seven players, and that will continue to be there. It is not like the six, seven players are gonna go away. They might reduce or go up. As long as one of us is going bust that nobody knows when that will happen or to whom it will happen. But if that happens, only then the others can get a better market share.

In power transformer, that moment, I mean, there would always be limited set of six, seven players to just to conclude, right? And that’s where it’s a more quality conscious kind of a market in some sense. Is that understanding, correct? Mudit Aggarwal: Yes. So, basically, there are some requirements with respect to the plant and so, for example, I just gave you the example of the lab. The PGCIL approval that we got is contingent on a condition that we have to get NABL accreditation for the lab in the next six months, which is why we have a deadline of September to get NABL accreditation, which is required for PGCIL 400 kV class certification to be kept in order. It’s not like they will strip us off the certification. But then those things are the key facts that many of the other manufacturers or the ones who are in distribution would not like to go through.

• So, once we are able to commit the history, the supply of these PGCIL orders in 400 kV class, then we will be able to apply for 765 kV, and then that will not be a very big challenge for us.

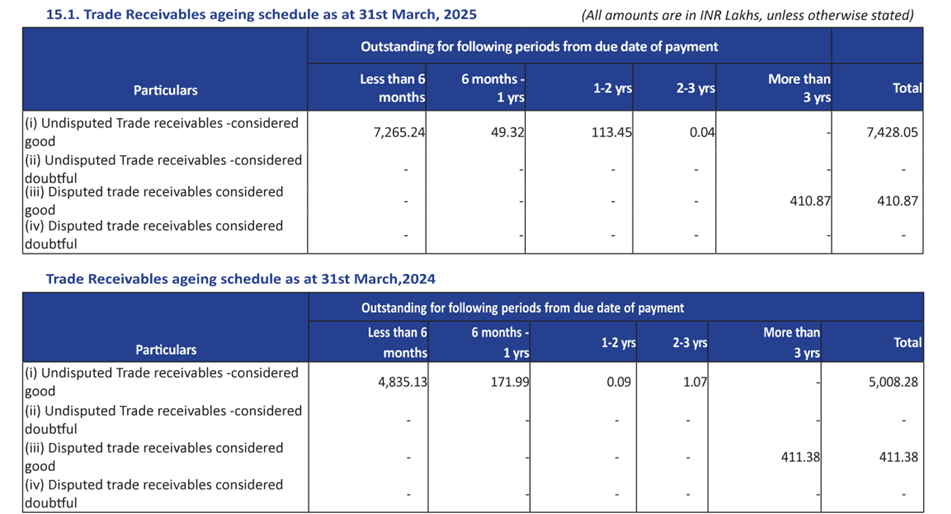

• INVENTORIES AND TRADE RECIEVABLES: So, inventory has actually come off. In September, like I said, we were carrying an inventory of three to four months to the tune of ₹90 crores, and it is reduced to ₹76 crores and we are further in the process of reducing it. See, we were in an uncharted territory with the new expansion and the new segments that we were targeting. We did not have the idea of or say the projection of which grades would be required in what quantities. We buy all grades, but there is a certain projection that we do based on past experience, past ordering cycles that the customers have. But for the new customers or the new segments, we were a little in the uncharted territories. So, we had to sort of stock up. And plus, moreover, there was a little bit of chaos in the raw material market also. So, we actually stocked up, and now we are reducing it. And now we are going towards that optimum level of 60, 65 days. And if you look at it from both inventories and receivables from a perspective of monthly or, say a quarterly sale basis, we are pretty much in the 60, 70 days range. So, for example, in the Q4, our total sale was about ₹113 crores, so ₹78 crores were the receivables. Yeah, so that translates to about 70 days.

Inventories will get optimized. Receivables will not reduce, primarily because, that is the kind of cycle that we have to do.

And then one more thing I want to point out here is that receivables are some of them, some of the receivables to the tune of about ₹30 crores are protected by the use of a letter of credit. So, we use an LC discounting facility where those receivables are already protected. And the other receivables, we are protecting through the process of credit insurance.

• **Given that the inventories are pending, raw material inventories to be consumed in April, May, you’re still confident of a 12%, 14% margin for the next year? I mean FY '26? **

On a yearly basis, yes. And previously, also I guided on a long-term basis, which is mostly yearly basis. If you see our EBITDA margins, it has been constantly increasing. On a half year basis, you might see a decrease. But we knew that, if you’re able to do a 15% margin, so we had some scope of making those, taking those risks where we could experiment and go for higher sales, aggressive sales, which is why we were able to get PGCIL approval in the first place. If we did not go for those aggressive sales where the margins were lower or, say, the pricing set by us not attractive to the customers, we would have not gotten PGCIL approval within the targeted timeline of March.

• When I said that assembled cores will command us premium is because of export market. Because in the export market, the assumption is that, they don’t have enough labour and it is a labour-intensive process. And if they don’t have enough labour, they would want the cores in the form of assembled cores.

• Why are we not able to pass on the entire pricing? Mudit Aggarwal: Because the movement, or say the volatility in the raw material prices came all of a sudden. And our bookings were already in place with the suppliers. Some of them were import bookings, which had material coming in pipeline, and some of it was already contracted with the suppliers. So, we could not, you know, go back to the supplier and say we want to cancel this order and negotiate on a new price, which is why the pricing was not we were not able to pass it on. We generally are able to pass on the pricing, if the volatility in the pricing or say movements of up and down are to the tune of more than two to three months or say even more than three months actually. Because we are carrying inventory of at least two months, right? And in this particular case, we were carrying inventory of three to four months, which is what actually hit us back.

• BIS LICENSES OF MILLS: Like I said, that the mills that we were talking about, their licenses expire very soon, and we still don’t know whether they will be renewed by BIS or not. So, we are still in a position where we don’t know whether these mills will come back or they will vanish away. So based on that realisations might go up or go down. However, with respect to our own margins, we will try to protect them by a better management of inventory now that we know what kind of orders are expected in the higher segments.

So, as you have mentioned that, we are still not sure whether the BIS license will be renewed. So, do we expect any increase in inventory or are we planning to stock up the inventory in case the BIS license does not get renewed? Mudit Aggarwal: So, we have sufficient inventory as of now for the next three months. We already have bookings and pipelines fixed. After that, we will again have to rely on the existing suppliers who are say not under the purview of getting or expiring BIS licenses. So, we have good relations with them. Last year also, we were able to secure good quantities from the existing suppliers. So, I think supply should not be a challenge. The only thing is when to buy, when to procure, and in what pricing level to procure.

• Our ordering with the suppliers is either on a three-monthly basis or on a monthly basis, depending on the supplier’s interest. Mostly they’re on a one to three months basis. Then we are also buying on spot basis. So, whatever we buy on spot basis, that kind of offsets the inventory gain or inventory loss. So, we try to keep a certain proportion of buying on a spot basis. That is how we move. Having said that, for power transformers, it is very difficult to buy on spot basis and expecting orders to come. We need to plan ahead, which is why we had more bookings in the last half year. I hope that clarifies that part.

THINGS TO TRACK:

• OPERATING MARGINS: The most important variable to track. Will it go back to 12-13% range as guided by management?

• VOLUME GROWTH AND CAPACITY EXPANSION PROGRESS

• HIGHER KV SALES AND ITS IMPACT ON MARGINS: Will it lead to increase in margins?

• BIS LICENSE SITUATION OF SUPPLIERS

• CCA AND TRANSFORMER PRODUCT PROGRESS

• CASH FLOWS

• MONITOR OVERSUPPLY SITUATION: A medium-term risk. Keep track of transformers company sales or any slowdown in volume growth of Jaybee.

2 Likes

Was there any details provided on the CFO levels? It seems like everything is stuck at receivables and inventory leading to huge negative CFO.

1 Like

ARFY25:

•

•

•

•

•

•

• We expect both inventory and receivables to stabilize at 60-70 days in the long run.

•

•

•

•

•

• Number of employees – 405 (vs 277 in FY24)

•

• Provision for doubtful debts – 25 lacs vs 0 in FY24

•

•

(4.1 cr Disputed trade receivables, more than 3 yrs ageing schedule)

•

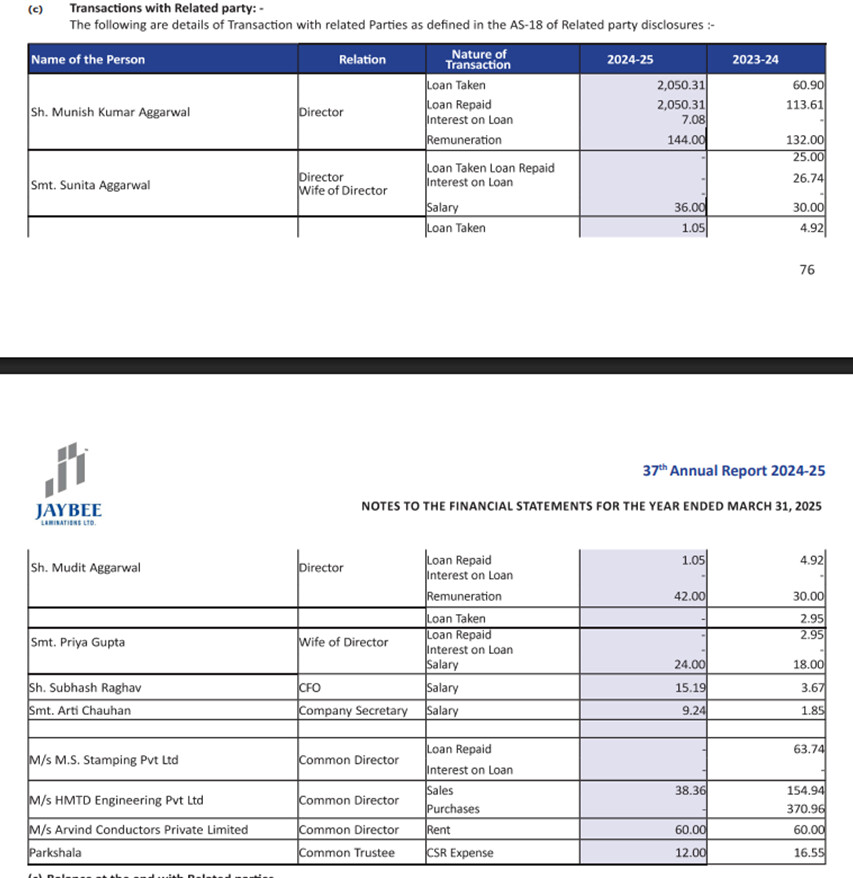

(Remuneration of 3 promoters – 2.12cr (PAT 25cr), Remuneration including director’s wife is 2.36cr)

THREE MINOR REDFLAGS -

- 4.1 cr of disputed receivables more than 3yrs old

- 7.5cr investment in property

- Remuneration of promoters is 8.4% of PAT, which is on the higher side (11% is the ceiling)

DISCLOSURE - INVESTED.

3 Likes