This policy is a blessing for JAI if passed. This was the reaction of CEO when asked about the policy in dec last year.

disc: invested and forms 10% of my portfolio

This policy is a blessing for JAI if passed. This was the reaction of CEO when asked about the policy in dec last year.

disc: invested and forms 10% of my portfolio

Considering how the truck operators have been hit hard by demonetization, I can’t see the Govt going for this long-talked-about scrappage policy in the near future.

Disclosure: Invested

Religare maintains a BUY in its latest research report with an upside of 24%

A new research report from CD Equisearch with an upside target of 25%.

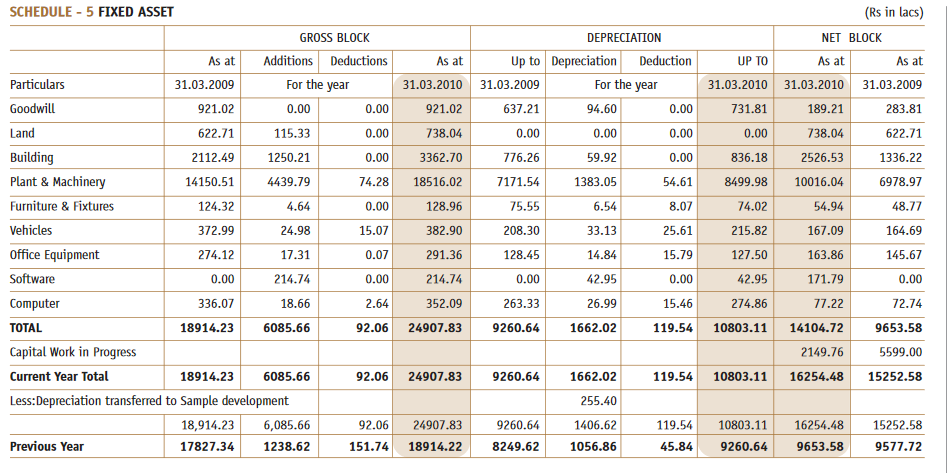

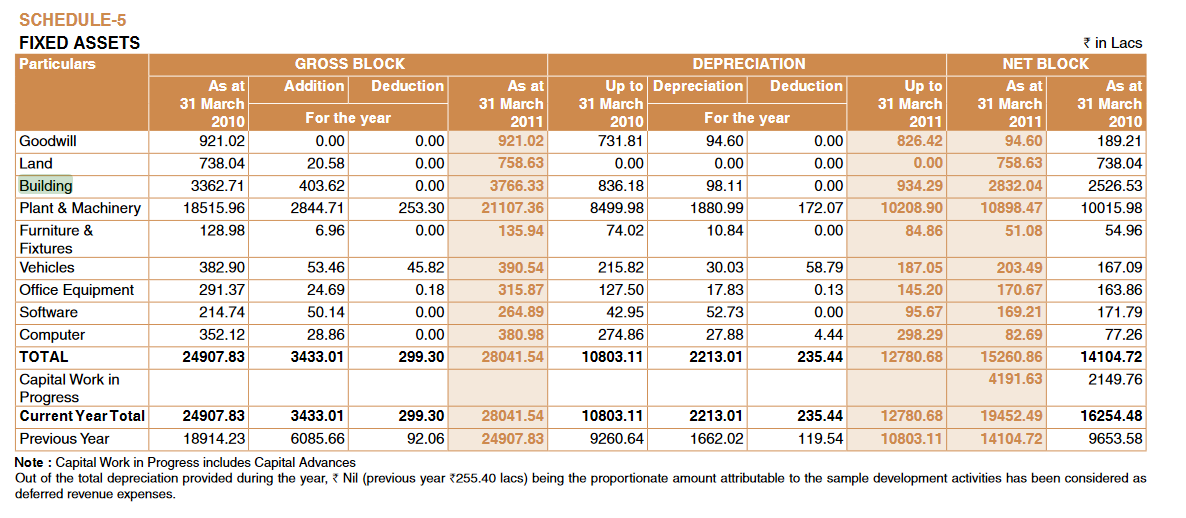

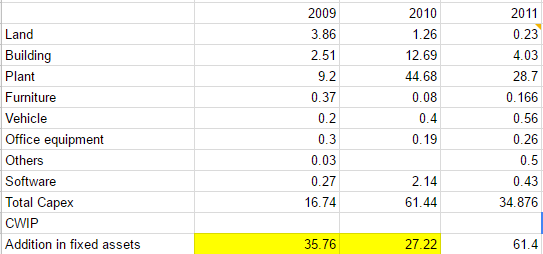

Some real concerns for me regarding the quality of the book. Year on year, the addition in fexed asset is divulging from the CFI reported on the cash flow.

From 2009 to 2011, the addition in fixed assets has grossly mismatched the cash flow for addition in fixed asset. Is there an accounting thing that I’m missing or is this a cause for worry?

Look at 2009 AR, addition of fixed assets as per CFI was 31.54cr whereas fixed asset schedule shows gross additions of 60.85 cr . Why the mismatch?

fixed asset schedule shows gross additions of 34cr, where-as CFI shows fixed asset addition of 54cr. Another discrepancy

@dsaraf All figures are correct. you are not considering the effect of capital work in progress.

WELL Thanks! This was not mentioned in the Schedule and that’s why I couldnt figure out the discrepancy.

Results are out

Muted sales growth .

27% PAT growth.

1:5 stock split declared

dividend of rs 2 declared

It is probably better to look at it QoQ because of the complete dependence on the cyclical MHCV segment. Also, the results seem to indicate the business is back to normal after DeMo.

I can understand splitting a 4-digit stock, but I simply don’t see the point of splitting a Rs.200 stock, that too 1:5.

Disclosure: Invested.

@rinkupranjan @Chandragupta @akaashbansal @atulgupta80

The suspension springs are required even for Commercial EVs, right? Any idea?

Jamna auto hot research report of 25th May from HDFC securities…Relevant

to the current discussion

http://hdfcsec.com/Share-Market-Research/Research-

Details/StockReports/3022847

With CV market under severe slowdown, not sure why analysts are projecting rosy picture for JAI for next 2 qtrs…I was reading a report of CD Research of JAI, where it mentioned that JAI failed to make reasonable dent in replacement market despite the best of the efforts

I don’t believe it’s a structural slowdown. There’s far too much public infrastructure that needs to be built out in this country to spur the growth, & also, the private capex will pick up when their utilization rates get close to 85% (from the current levels of around 65%).

The management itself has indicated a subdued 1HFY18. It’s common sense - The fire sale of BS3 CVs at the end of Q4, and the rainy season will slowdown the construction activity.

The distribution network has been improved significantly, and the onset of GST (& hence the superior quality of Jamna’s suspension springs) will help increase the market share in the replacement market.

Disclosure: Invested

In case one listens to Amara Raja concalls, management has clearly mentioned, GST is no magic, it will take 2-3 years for organized sector to capture the unorganized one’s significant market share.

Disc. Invested

Point taken on GST.

The one advantage that Jamna has is, their core OEM business has negative working capital cycle, which might allow them to offer favourable credit terms to their retail partners to try and increase their foothold in the replacement market.

Even if GST’s impact on prices of products from the unorganised sector takes time, Jamna’s economies of scale, and the efficiency that comes with not having to worry about different state taxes will help.

Does anyone know the date from which split shall take place?