Adding a quick update,

I’ve started building positions in :

- Mircofinance - Credit Access Grameen, Equitas SFB; and Spandana Sphoorty

- Agro chem - UPL and Punjab Chemicals

There is undeniably a significant probability of another year of pain, but the technicals and trend in ratios over the last 5-6 years suggest that the worst of the storm might be over, and sunshine is near. Will be looking to scale this up if the chirping ensues.

As I quote Thomas Hardy in the desolate snowy winter- “So little cause for carolings, Of such ecstatic sound, Was written on terrestrial things, Afar or nigh around, That I could think there trembled through, His happy good-night air, Some blessed Hope, whereof he knew, And I was unaware.”

Do share your analysis/views or any other value stock which piqued your interest

2 Likes

I also find value in the Fusion Finance with 11k crore assets and 2k crore Mcap, NIM 11%, collection efficiency 97%, the forthcoming Rights issue is expected to give price stability of the stock and any further reduction in the slippage of assets should give the upward price momentum. Disc- invested at the higher levels and looking to subscribe the Rights issue.

2 Likes

Thank you for sharing your insight on Fusion Finance, Alok sir.

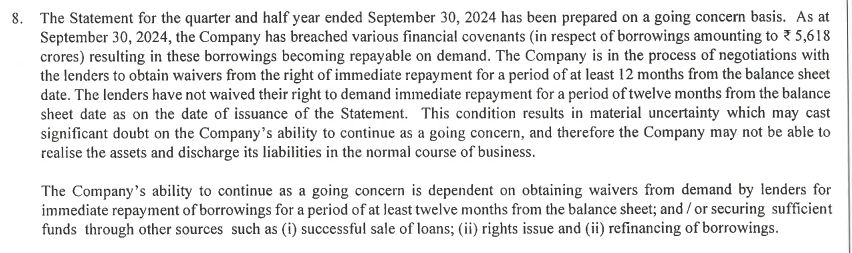

I had been analyzing it while covering microfinance sector as a whole, and my key concern was precisely the rights issue that is currently underway. Attaching a snapshot from recent qtrly audit report by Deloitte on Fusion Finance :

The rights issue is a do/die for the company, rather than a growth trigger at this point. It is very troubling that the rights issue is happening after the share is down 70% - basically raising pennies on the dollar by diluting too much stake, because there is no other survival case apparently.

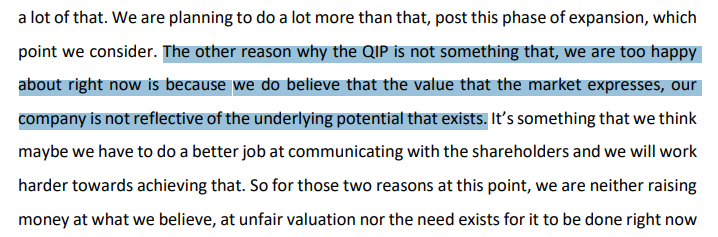

We ideally want a case where there are too many preferential issues at All time high prices like current times in Hospital sector - so companies are able to raise capex funding at low dilutions to expand in next down cycle. A key example is Narayana Hrudayala that chose not to raise equity funding at low valuations - attaching concall snap

I do believe the microfinance sector can form a bottom base soon, but feels safer to bet with established players like Arman, Equitas etc instead to avoid survival issues at least. Pls do correct me if I am wrong here, since I’m still trying to learn more about this sector.

2 Likes

My hypothesis says that in the Bull phase the worst stock does the best and in the bear phase the vice versa happen. If the microfinance as a sector is on the verge of a bull phase then most beaten down stock would do the best.As far as the Rights issue is concerned, we know that the PE fund Warbus Pincus will never exit at loss. They have already promised to subscribe the whole 800 cr issue. My assumption is that the issue price would be above the FY25 BV… In the case of the preferential issue before the rights issue the SEBI prescribed formula based price as on today is already much above the BV. In both the cases the Rights issue will be BV accretive. The brokerage firm MOSL has estimated 150cr further loss in H2FY25. If the sector revives I don’t see why this stock should trade below BV. The company is already seeing a turn around phase and has added 60% employees in H1FY25 itself. In the last month MFs were the net buyers in this stock ( edited MFs are the net sellers as per the updated data on the Trend line) and they are already holding a large chunk of it. I am closely tracking this company and also have visited one of its Branch today itself. My views may be biased,

2 Likes

Quick question on an assumption Alok sir, if Rights Issue happens at above current Market Price, does it not make sense to buy more shares from open market instead for same amount of money?

I haven’t tracked the pricing formula, but need some clarity on how the issue will work, if at all when priced higher? Thanks for sharing some good insights though, tracking employees data is a great move.

1 Like

Rights issue happening above the BV is an assumption. The promoters have kept an option open for the 160cr preferential issue and I feel that they may excercise this option if the market price significantly goes further down so that the preferential issue price would be at the lower end. I feel basically they have talked about the preferential issue just to protect the further downside of the market price. Rights issue will be partially paid so the equity dilution is expected at the higher end and the promoters would like to give comfort to the long term investors. I feel that as the promoters are strong enough they would not like the issue to happen below BV. Probably the market is expecting the more credit losses in q3 and hence there is the price pressure. I feel more clarity to emerge after Q3 results. I am basically with the promoters and hence not willing to exit it below the BV. MFI typically does better business in H2 then the H1. Let’s see how the this shape up but one thing is for sure that if you buy after the clarity then you have to pay also for the clarity.

3 Likes

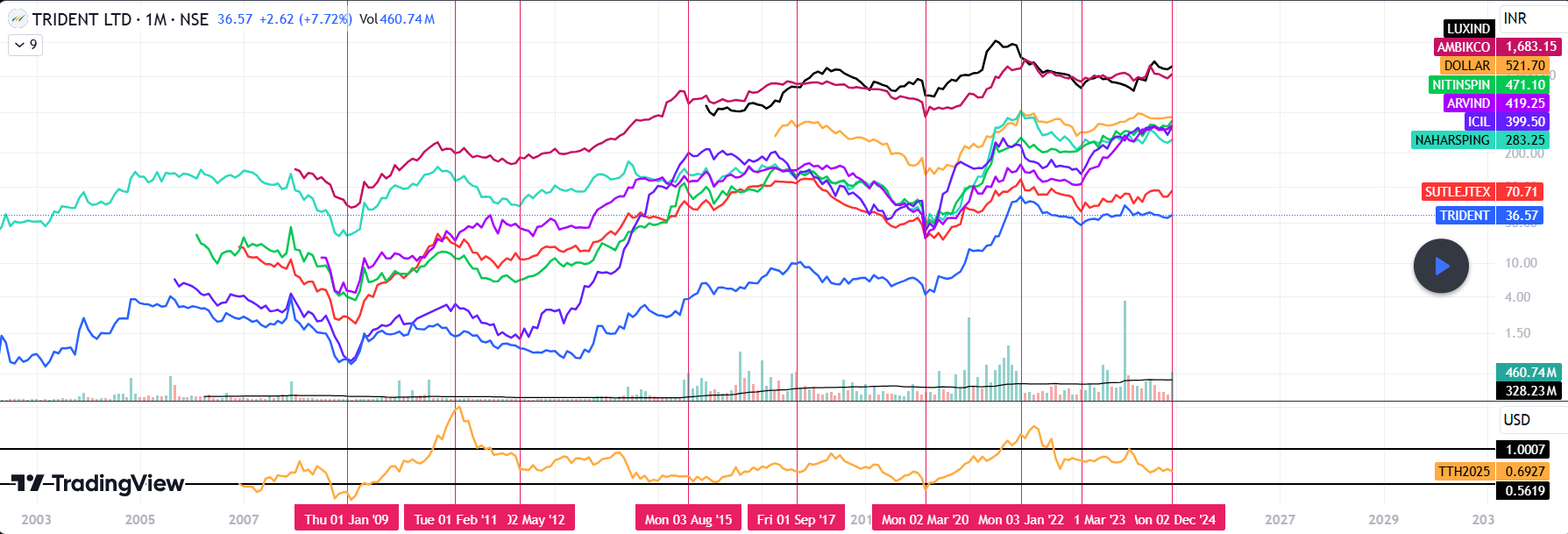

I’ve been tracking textile sector, and there seems to be amazingly strong correlation between cotton prices and textile players across the value chain. With cotton prices almost reaching their usual bounce region, and multiple players confirming their views on cotton/yarn prices stabilizing in H2, this sector seems poised for some good times.

Attaching chart for reference. The top area has prices of key players, and golden line on 2nd pane is cotton prices. Clearly the correlation is obvious here.

14/20 players I’m currently tracking have breached ATH. Looking to build positions in players who are still trading a significant drawdowns despite showing the same price action all these years, such as :

- Ambika Cotton

- Sutlej Textiles

- Nahar Spinning

- Rupa

I’m very new to this sector, and most of my understanding is built by price action in last 20 years, and recent concalls from players. Do share your insights/suggestions on what might work/go wrong, any other stocks/sectors you are tracking, or articles/links to study more on. Thanks!

2 Likes

what is your views on GHCL textile. Cheapest textile player, which recently got demerged from GHCL . Capex to increase spindles along with Green energy initiatives are under progress.

Disclaimer: Holding from demerger and bought around 70 levels around 1 year ago.

2 Likes

I don’t track GHCL textiles as such, but prima facie seems to tick all major boxes. Capex commitments of 1000 Cr, Export mix increase, Improving product mix along with margins mean reversion to 15% from 9% currently, P/B lower than 1 and vertical integration plans for future - it sounds like someone promising the whole world with a pretty pink ribbon tied around it.

It’s recent listing is the only thing that annoys me, because that limits my insights from Technicals price action perspective. Worth tracking closely, thanks for sharing Thakurvi!

1 Like

To digress a little bit, I was looking into Bitcoin price action since inception, with a friend who has been a veteran in this ( & won’t stop talking about it )

Bitcoin halfing happens every 4 years, and it halfs supply of bitcoin in circulation, which allegedly leads to increase in prices. I’ve tried to confirm this via price charts to see how true it is, and if we can get further insights on entering/exit timelines.

Dates for bitcoin halfing have been marked in chart as green vertical lines : November 2012, July 2016, May 2020 and April 2024.

Some very interesting points, noting for future reference :

- Bitcoin has seen 3 major falls - each to the tune of 75-80% drawdown

- After halfing event - for next 1.5 years there is a strong uptrend with prices going up 10x in previous cycle (from green vertical line to pink vertical line in attached chart)

- After 1.5 years generally price gives heavy drawdowns for next 1.5 years

- Next 1 year just before next halfing is usually a period of prices stabilizing with positive bias

- If the same cycle repeats, prices can go north of USD 500k in next 1 year - which sound highly unrealistic to my ears too, but the trend says otherwise.

I am not asserting that it is a safe/legit investment vehicle, but it’s interesting to note the symmetry in price actions every cycle. I’m not invested in any way in any cryptos, nor do I plan to - but it’ll be exciting to track how this plays out.

Do share your views on this!

3 Likes

I’m invested in Venkys & Hil ltd from the list for the reasons you mentioned. These stocks are in Technical Stage 1 consolidation. Buying at bottom of the stage 1 is preferable. All bad things are priced in here. Let’s see how long it takes.

Imo venkys might have some trigger next quarter. Hil ltd will take longer time. They are suffering from Paradoor aquisition.

I’ve also tried all the things in past 3 years and after my selling things have become winners. So this time I’m doing fomo buying and not selling panic.

1 Like

Indeed, hopeful about Venky and HIL doing good in coming times.

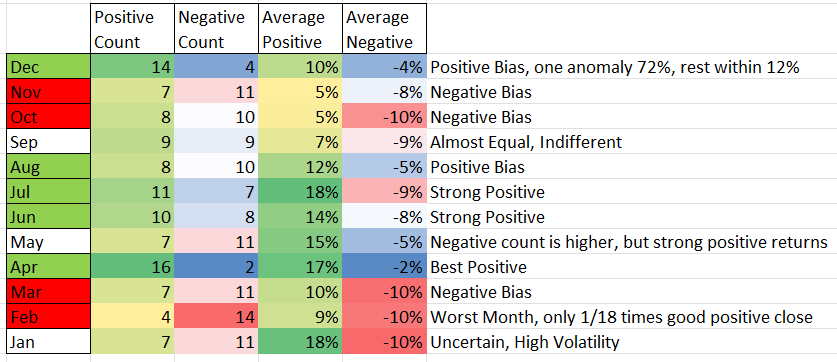

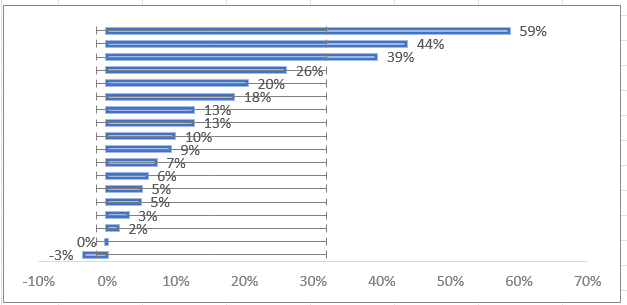

Sharing a seasonality study I recently did on HIL - MoM analysis for last 18 years

- Positive/Negative Count shows number of times share closed positive/negative in that month in last 18 years.

- Avg Positive returns shows average returns the share gives when it closes on positive side in that month. Similar for Avg Negative returns in that month, for times when share closes negative.

For April month, the returns distribution is highly bullish :

For February, it is very bearish with only one good positive close so far

Would like your inputs if this makes any sense to you/reasons for this cyclicality. Will accordingly build one for Venky too with any suggested improvements.

Did a fundamental study and here I’m attaching the notes for your reference.

Venky.pdf (1.9 MB)

Technically I see it in a stage 1 base. So if we buy at stage 1 base bottom we have absolute margin of safety.

If fundamentally things improve from here we have good upside.

From latest concall we can see some recovery in Q3 onwards.

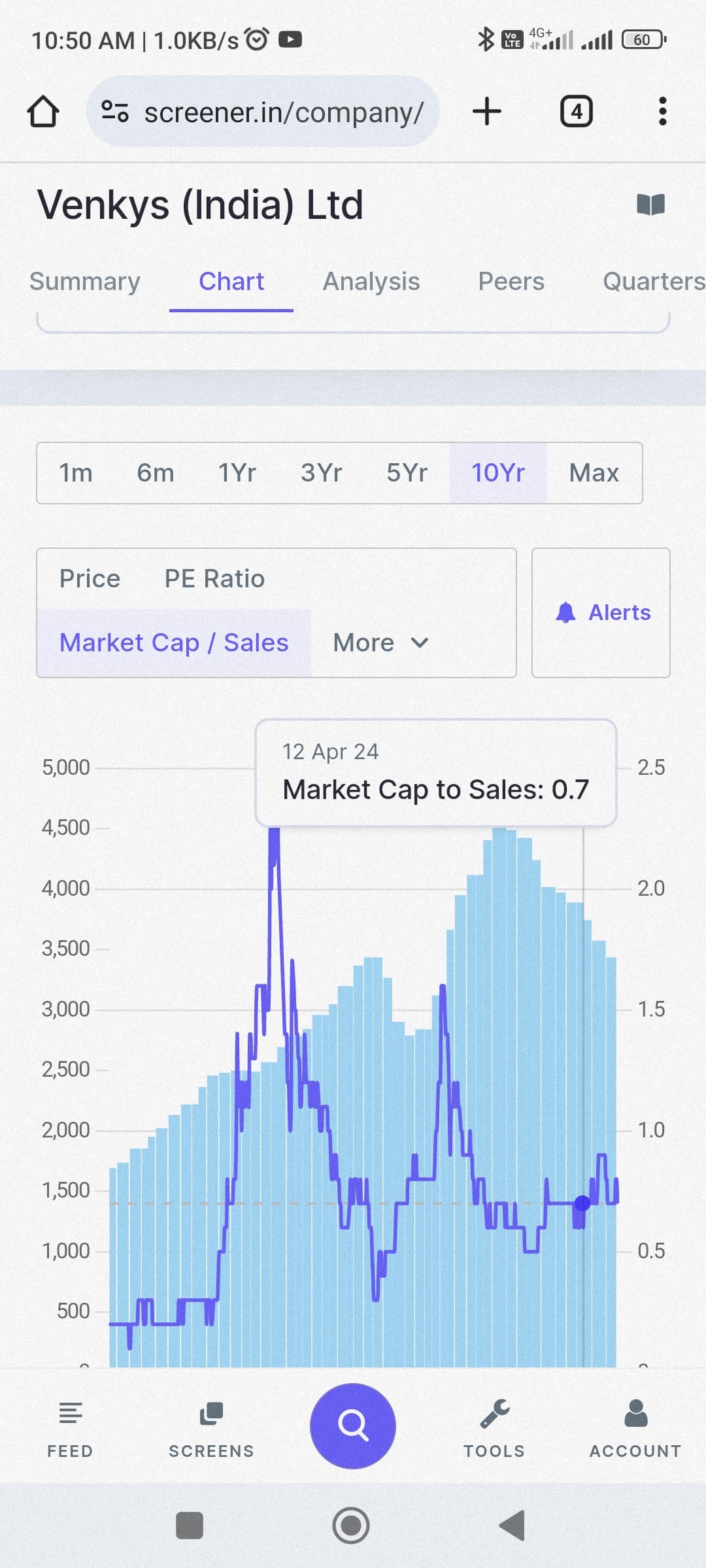

Valuation is historically cheapest. 0.7 times price to sales which is at lower limit of valuation range

So a good risk reward ratio from here. I guess from Q3 result we should get more clarity. q1 was good. Q2 is a seasonally weak quarter. Q3&q4 are good.

Antithesis is maize prices are rising which is a key Raw material for Poultry feeds. Chart of maize is in the report. But all bad things are priced in. Number of total shareholders (it’s a good indicator of retail shareholders) are reducing you can see in screener…this is a good sign of accumulation.

So these are my thesis.

- Stage 1 base bottom,

- Low valuation

- Accumulation

- Potential fundamental trigger in coming quarters in terms of earnings by margin improvement (indicated in latest concall)

4 Likes

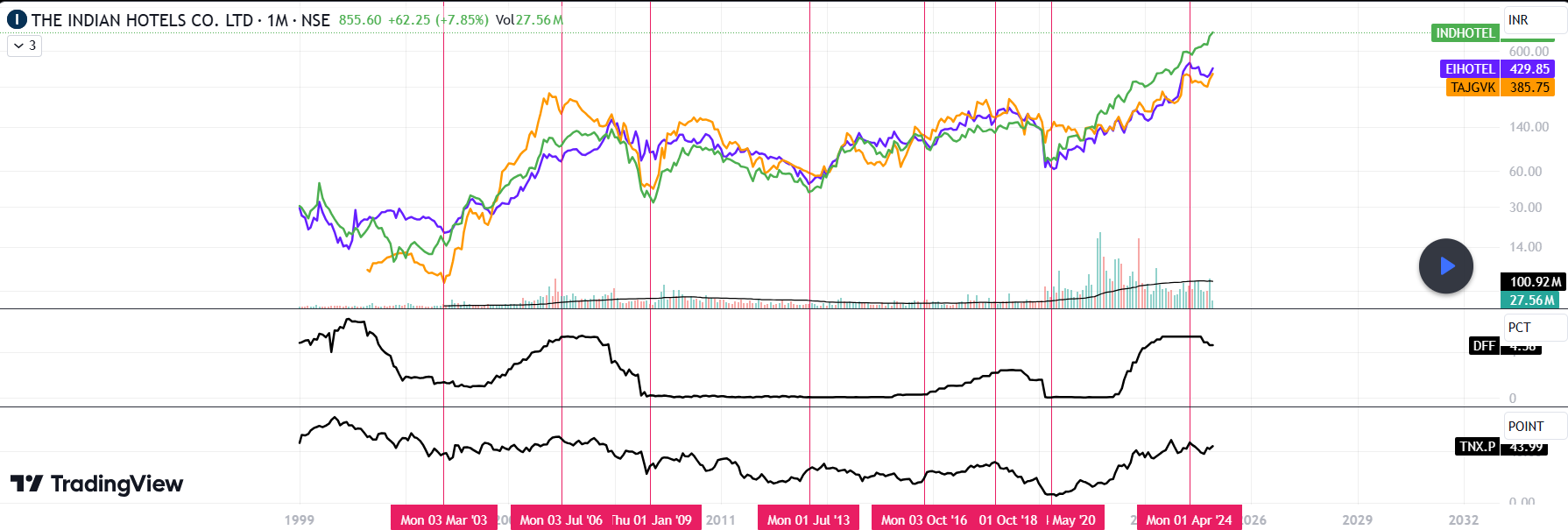

In the below chart, I’ve plotted prices of 3 Hotel stocks - IND Hotels, TAJGVK and EIH. The below 2 panes in black are US Federal rate and 10Y Treasury Bond Yield.

Prima facie, hotel industry seems to show good correlation with Interest rates in US. It might be due to the recessionary events ensuing interest rate decreases, and with current all time high occupancy rates and earnings, it’d be interesting to see if the cycle reverses again.

Do share your take on hotel industry, and any reasons that might add more meaning to this cycle.

Hi everyone,

It has been a long while, and to maintain continuity in chronicling my thoughts - I’ll try to enlist what sectors and names I’m tracking in the current market drawdown ( a part of me believes 20k is where we might bottom, if not from current levels - being very cautious in terms of sizing bets )

The older names still stand alive, albeit after quite some bleeding -

-

BOPET sector - Polyplex, Cosmo First - seems to be continuing its primary wave of upward ascent after a temporary (and tiring) cooldown in last few weeks.

-

Natural Gas distributors - IGL, MGL - after recent part reinstatement of cheaper gas supply by gov to these players, likely that their margins will benefit along with anticipated price increases.

-

Microfinance banks - Arman, Credit Access Grameen, Equitas - With the revised risk weights to 100% and slowly improving PAR ratios indicating early green shoots, a part of me believes the worst is behind us.

-

Caustic soda - Primo Chemicals, Lords Chloro Alkali - a commodity bet on mean reversion for prices of Caustic Soda

-

Agrochemicals - UPL, Punjab Chemicals, Rallis India - betting on reversion of chemicals cycle especially with rising consumer demand from agriculture segment driven by good monsoons

-

Pharma - Hikal, Aarti Drugs - With reversing API prices, expecting these players to benefit and turnaround in coming times. Hikal has been holding up well so far, quarterly results might provide some more clarity.

-

Other plays - KRBL, Oriental Aromatics, Zydus Wellness, Honda India Power, Hester Bioscience. Some of these are new names that fell at attractive levels in the ongoing market turmoil, and made sense to accumulate some.

-

Exited - Vaibhav Global, Venky, HIL, no longer actively tracking sugar and cotton sector for now. There just seemed better risk reward bets with more conviction to rotate capital.

I’m also looking at few other names such as RHI Magnesita, Insecticides India, Bayer cropscience, All cargo logistics etc and would love to know any insights on them.

Thanks for reading so far, will keep updating this space how this deeply cyclical value biased experiment works out.

8 Likes

Alok ji,

What do you make of the Q4 of Fusion.

I was expecting slightly better numbers, given the amount of provisioning that happened in Q3.

Infact in concall Q3 , management had even stated they reversed all intrest for all npa for the impact of entire FY-25( q4 hit was also taken in Q3) with that regard.

Still now given the numbers coming for q4, seems new slipages have happened

Management hasn’t communicated yet about concall date, so clarity is still missing.

Book value has drastically erroded. for fusion.

It’s now not looking cheap at all in terms of price to book.

Your take, since you track this stock?

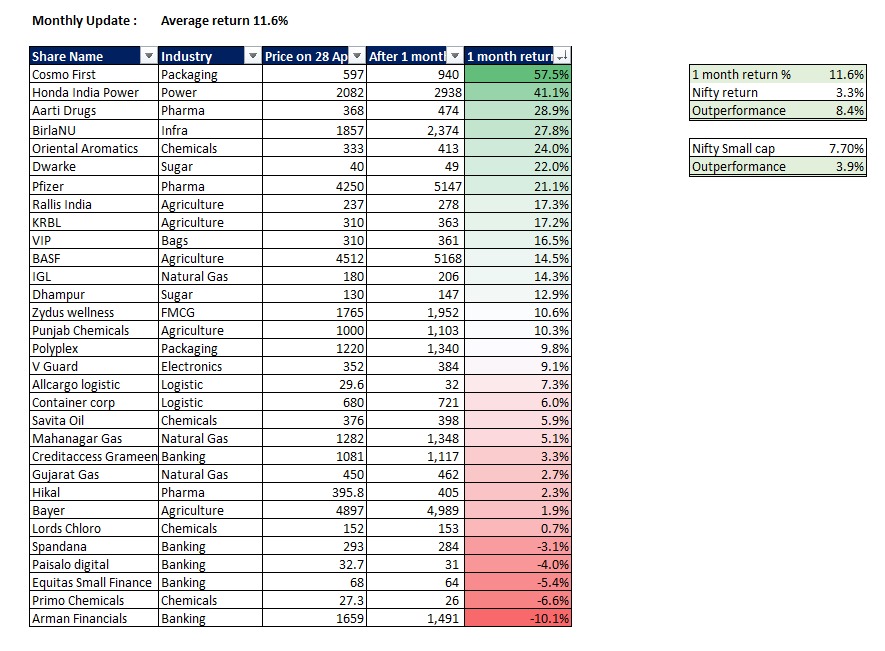

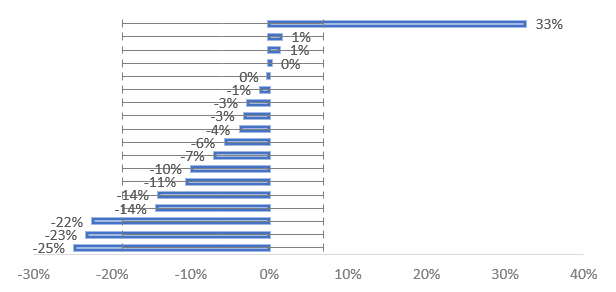

Sharing a monthly update to the value tilt portfolio :

Average 11.6% return in May. Beating Nifty by 8.4% and Nifty small cap by 3.9%.

BOPET, Power and Infra were the top 3 leading sectors. Agriculture and Pharma did better than average. Microfinance banking gave negative returns primarily due to cooldown from previous month outperformance.

1 Like

Venky India - Seasonal downturns led to massive devaluation for chicken centric shares and as a fellow chicken aficionado, I know every chicken has its day. Management seems quite confident of H2 and I am not chickening out of this.

What are your future projections of this stock over 5 years

1 Like

Hi Garv,

Thanks for asking this question. As you can see my previous posts, I’ve already exited Venky some weeks back. I’m not very hopeful of a short term recovery either.

1 Like