As per management, there is one-off adjustment that has been made to WACC Which was calculated higher in past. This adjustment was included in the revenue of Q4 results. This leads to the reduction in revenue

2 Likes

This proposal of 5.25 lakh crore capex plan for railways is apart from the railway budgetary allocation of Rs 2.6 lakh crore for 2023-24.

(1) Is this narrative the reason market is giving a thumbs up to all railway stocks including IRFC??

well, this may be partially true. But there may be other reasons too, i guess !

(2) Business is monopoly in nature ,enough cash generating machines

(3) A year back , these stocks were languishing at very low level at very low p/e ratio …even now 8-10 P/E ratio is not very high to lose money when compared with high P/E Market in general. And most PSU companies have clean balance sheet-! Mr market seems to have realised this

(4) The Govt has realised that the only way to get rural vote is to generate employment opportunity for the rural mass which could be through huge capex, Make in India theme such as defence etc which in turn would also propel economic growth - Govt in turn also get revenues out of dividend and divestment in these PSU through OFS (once stock price goes up) .win- win situation for the govt and the country in general

(5) As regards to IRFC , the business is unique in nature.

Indian Railway Finance Corp borrows funds from the financial markets to finance the acquisition/creation of assets which are then leased out to the Indian Railways to mainly RVNL IRCON or any other entity under the Ministry of Railways. These are long term lease of 30-40 years and at the end of the lease period , the railways buys our the asset at written down value. Railway is not likely to default on interest payment.

Last week, state-owned RITES inked a memorandum of understanding (MoU) with IRFC to explore avenues of mutual collaboration in the railway eco-system and the transport infrastructure sector.

As part of the MoU, RITES will offer consultancy & advisory services and assist in ascertaining the financial & technical viability of projects, while IRFC will provide financial services to projects/ institutions that have got backward and or forward linkages with the Railways.

Discl: IRFC forms a part of my basket of Railway stocks created a year back for long term horizon of 3-5 years

… It is not buy or sell recommendation. Please do your own assessment before investing.

PSU stocks carry risk of frequent change govt policy. If there is a change in Govt , the entire capex story may not continue.

PSU stocks quarterly performance may or may not be consistent "qoq"or even “yoy”

8 Likes

IRFC 28% rise within 2 days

It may not be advisable to board a running train at this high speed.

In spite of the fact that the Govt has already declared its intention of divesting 11% through an OFS, the share is still rising and MCap has gone up now it is more than Shri Ram finance and M & M finance and many others.

The OFS may now be executed any time as the Govt would like to avail this high stock price.

And depending upon the OFS price , we may get an opportunity for entry. Market would give an opportunity.

discl: Holding stock from lower level as a part of my railway basket . please do your own assessment before putting you money

5 Likes

IRFC reaches a new high with MCap exceeding 1, 10, 000 Crore.

It is now the 2nd highest NBFC as regards to Mcap after Bajaj Finance.

It has over taken biggies like Chola, Shriram, Muthoot , L&T finance , M& M finance ,

Poonawalla etc

It is Euphoric now - it is frothy for a NBFC like IRFC. One should exercise caution for fresh entry. one can wait for OFS.

Booked profit as it has already given me 3x returns.

Discl : It is not a buy or sell recommendation. please do your own assessment before investment

Corrections are healthy - Experts see no change in PSU fundamentals

While I booked some profit before the correction set in in some of the stocks , but in the process of adding few of them back again in decline where it still enjoys good valuation and fundamentals with revenue visibility for next 4-5 years with order book.

Discl: Not a buy or sell recommendation in any PSU stocks as it carries inherent risk of frequent govt policy changes. please apply due diligence before investment

9 Likes

For those who are curious to understand fundamentally what has been driving the IRFC Stock and whether there is steam left, this Case Study by Professor Bakshi is a work of ART, just like a wow !! ![]()

Enjoy friends

10 Likes

Can we get the relevant and current fy figures mentioned in the case study?

Yes from Screener.in

1 Like

IS this just pure price action euphoria?

-

no increase in loan growth, decline in EPS growth during H1

-

Future, most of the Railway Capex budget is being funded by Central Govt as par of union budget (This means hardly any growth for company- this can be seen from last few quarters)

-

Valuations trading at 3x of historical averages

Experts, what is the future for IRFC?

Sitting on 3x, is it better to exit?

3 Likes

All the proposed funding for Huge capex in Railways will have direct positive impact on IRFC.

So the market will sense this in the near term.

1 Like

OFS in PSU’s to meet Divestment target 2023-24- there are many possible candidates during Feb- March 2023-24 as listed in the article - IRFC could be one of them- for the Govt , it is mouth watering valuation

For the current fiscal year 2023-24, the Union Budget has scaled down the disinvestment revenue target in the revised estimates to Rs 30,000 crore from Rs 51,000 crore.

It has been a good practice on part of the Govt to release this info in advance so that small investors remain alert for trading ,/ buying /selling. i also watched in TV from DIPAM officials some of these names as possible candidates for OFS.

Discl: Exited IRFC long back with profit booking

1 Like

Discussion Topic: Evaluating the Future of IRFC Amid Stagnant Profits and Limited Growth Prospects

Hello IRFC Community,

I’ve been closely following IRFC’s quarterly results, and it seems that profits have been stagnant over the last two years. Additionally, during the last earnings call, management mentioned that the government has already allocated most of the Railway capex in the budget for the next 2-3 years, reducing the need for extra-budgetary resources. This could potentially limit IRFC’s growth in funding railway projects.

Given this context, I’m concerned that there might not be much room for EPS growth in the near future. The market price seems to reflect an optimistic outlook, but with the current lack of growth catalysts, I’m wondering if the stock might be overvalued at this point.

My Questions to the Community:

-

Stagnant Profits and EPS: What are your thoughts on the stagnation in IRFC’s profits and EPS over the last couple of years? Do you see any potential triggers that could drive growth in the near future, or do you agree that the stock might be overvalued given the current outlook?

-

Impact of Limited Government Capex: With the government already allocating most of the Railway capex in the budget, reducing the need for IRFC’s extra-budgetary funding, how do you think this will impact IRFC’s business model and profitability in the next few years?

-

Long-Term Viability: Despite the current challenges, do you believe IRFC has a viable long-term strategy to adapt and grow, or should investors be cautious given the potential limitations in funding and growth?

Looking forward to hearing your insights and opinions on whether IRFC can navigate these challenges or if the current valuation might be too high given the stagnation in growth.

Thank you!

3 Likes

You have raised a very pertinent question. I will refrain from speaking on valuation. You have correctly pointed out that growth prospects are limited in near term but long term prospect is intact. IRFC AUM will not grow consistently, most of its growth will be concentrated in a few years (black swan type event throwing govenment fiances off). In a period of 10 years majority of growth will come in 2-3 years.

Indian railways will continue to remain the only affordable means of transport for large section of the population of the country and demand will only rise drastically in the future as disposible income of people rise. Moreover, in my view the goverment will not be able to generate surplus from indian railways operation in passenger segment; at most it will break even. Spending on rail infrastructure is planned at around INR 38 lakhs crores over coming decades. Funding sources have been identified for some (eg. dedicated freight corridors) but not for others. All these are detailed in the government’s national rail plan, relevant chapters being 20 and 21 (pdf link https://static.investindia.gov.in/s3fs-public/2024-08/national_rail_plan_2030.pdf). Now all these are projection and actuals can be substantially higher or lower. But one thing is clear that demand on indian railways is going to increase substantially and infrastructure needs to be upgraded significantly. And its going to cost a lot for the governement. And in my view as governement tries to rationalise GST/IT rates (can not earn substantially while keeping the rates high, there will be demand to lower rates) and achive its fiscal deficit target, it will have less room to fund the infrastructure projects from budgetory allocation. And one black swan event (like COVID) which through the finances off will result in substantial allocation to IRFC for funding requirements.

1 Like

Today, I listened to the IRFC concall, and a key takeaway was that the company has shifted its focus away from relying on Extra Budgetary Resources (EBR). Instead, they are now concentrating on forward and backward linkages within the railway ecosystem. The management highlighted that these linkages could provide margins up to four times higher than their current low-margin business with Indian Railways.

Their strategy seems to prioritize profitability over revenue growth in the coming years. However, it remains unclear how much time it will take for IRFC to build a substantial business outside its core operations with Indian Railways and what kind of support the government might extend in this new direction. Considering that valuations are already on the higher side, I’d like to hear others’ thoughts and expectations for the company’s future.

3 Likes

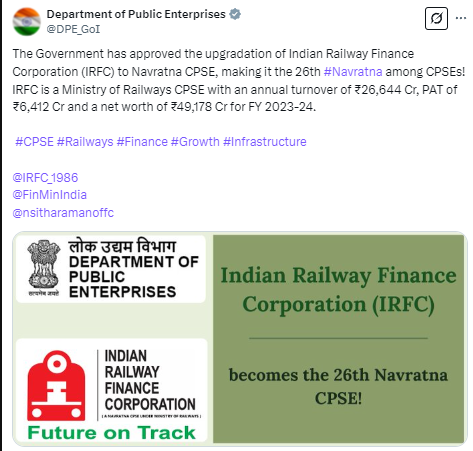

The Government has approved the upgradation of Indian Railway Finance Corporation (IRFC) to Navratna CPSE, making it the 26th Navratna among CPSEs!

2 Likes

IRFC has now expansion plans of venturing into other domains apart from railways while maintaining its zero NPA status as per the recent PPTs and Concalls. However, will that improve its NIMs and PAT subsequently and have a positive effect on the share price is something to ponder upon. If anybody is tracking this, will love to hear their opinions.

Currently this company trades at trailing price to book of 2.3; this is now crazy as HDFC Bank also trades at similar valuation, SBI and other PSU Banks at even lower. I am not even talking about one/two year forward which I should as market will start recognizing FY 28 by nov/dec.

2 Likes