With regards to annual fastag, it applies to toll roads of NHAI, not those which are delveloped by the State Govt or its arms. One needs to look into how many assets are not contracts from NHAI

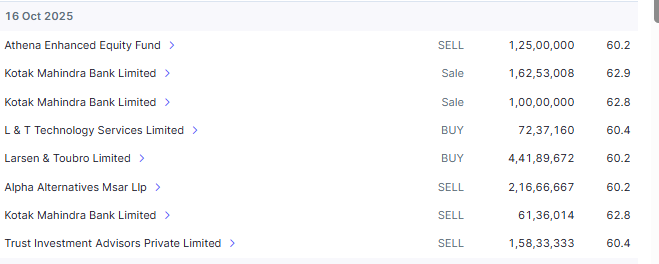

Surprising trading activities and not sure how these are permitted by Sebi. Kotak Mahinda Bank gets units in preferential QIP at 60 and sells in market within days

1 Like

Declared 2nd Distribution of Rs. 1.50/- per Unit, for the financial year 2025-26. The distribution will be paid as Re. 0.90/- per Unit as Interest, Re. 0.48/- per unit as return of capital subject to applicable taxes, if any and Re. 0.12 /- per unit as exempt dividend.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/11a07fd7-bddb-429b-8ba1-fed0b3fdd292.pdf

The 3 new assets came into the books in November but the additional units, to finance them came into play, well before this quarter’s record date. With the units swelling, and the cash flow from new assets yet to accrue, I am glad that they could put together 1.5 atleast as DPU. Obviously something else, would have helped in it and not the mere 10-11% toll increase that happens Y on Y from existing old assets.

Looking ahead, even the next distribution too won’t be normal since Oct is still with the old assets only. It will all get normal, only from Jan’26 qtr onwards.

All said and done, IRB invit has proved that they can digest this much quantum of fund raising and placement, to add the assets. The sheer longevity addition of the new assets is stellar by all means…what will be the reset on DPU? on to concall…

PS - invested and biased

6 Likes

Looks like, NAV per unit from ₹96.60 (as of 30 Sep 2025 with 6 SPVs) will come down, after adding the new SPVs, to approx ₹82**.

** Rough calculation:

(30 Sep 2025) 6 SPVs

NAV = ₹5607 crores

Shares = 58.05 crores

NAV per unit = ₹96.603 SPVs

EV = ₹8436 crores (as per Half yearly report)

Debt = 3600 (as per concall)

NAV = ₹4836

Additional shares = 70.11 croresThat means, 9 SPVs

NAV = ₹10443 crores

Shares = 128.16 crores

NAV per unit = ₹81.48I wonder if this is the right way to calculate revised NAV. Probably that ₹3600 crores debt is incorrect after part of it handled through equity dilution?

That is 15% down! Where did this 15% value go, I think to the private InvIT. What investors get in return, InvIT survives longer.

What is the point of keeping InvIT alive, if it only helps to transfer the value to the private InvIT in stages. It also helps to lengthen the employment tenure of the management. I don’t know if there is anything for the investors in this exercise, except the loss of value.

Yes, as per CMP, the InvIT is still about 25% discount to the NAV. But that means nothing, if we consider the value may eventually be transferred to the private InvIT.

NOTE

I consider myself a novice investor; here for learning and improving my understanding. I welcome corrections (to calculations and my views/biases).

2 Likes

I am not sure on the way you have calculated the NAV post addition of new assets on 5th November and would wait for management clarification on dilution or intent of taking new assets which may favor their parent company more.

Any other financial expert can check on the dilution and revert on the current NAV post this dilution.

1 Like

Many queries answered in recent concall

NAV between 75-80

Current levels may not see any appreciation for near future

3 Likes

Hi Amit,

Can you please share the link of the concall as I am not able to find it. Also is the 6.5 rs is for the entire year which is reduction of payment of current 8rs per year. I thought the 1.5 rs quarter is only for Q2 & Q3 of this year as the assets have been acquired in the mid of the quarter. If its 6.5 per year then the yield will be very low at 10.6 % year. Thanks for your answer.

Concall-IRB-InvIT-13112025.pdf (227.9 KB)

Investors disappointment evident

1 Like

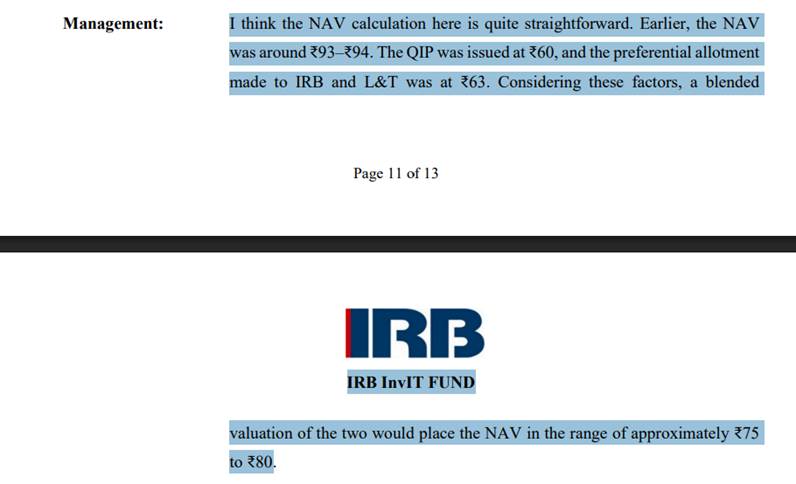

I think the NAV calculation here is quite straightforward. Earlier, the NAV was around ₹93–₹94. The QIP was issued at ₹60, and the preferential allotment made to IRB and L&T was at ₹63. Considering these factors, a blended valuation of the two would place the NAV in the range of approximately ₹75 to ₹80

NAV reduced from ₹96.60 to ₹75-80 which is 17-22% fall. Both NAV and DPU are reduced. Then what is the point of the acquisition? The justification given:

when you have a growth asset that compounds consistently, there is a natural mismatch between the life of the existing assets and the life of the asset being acquired. If the new asset has a much longer residual life, the initial DPU is bound to adjust downwards.

I don’t think this is clear me. I guess this sort of means, the revenues will grow later only.

Otherwise, increasing the life of InvIT seems to be the only thing management keep talking as the benefit from these acquisitions. I still don’t understand how this helps the unit holders when the overall value is taken away.

2 Likes

It could be possible that new asset is less profitable. Therefore making DPU of 8 unsustainable.

That’s why, they might be reducing DPU. I am new to InvIT and maybe I am wrong.

Agreed. As an investor, what we care about is the value of our investments, and the NAV is supposed to be an indicator of the value. Any action that reduces the NAV, i.e. the value, is by definition not in the interests of shareholders / unitholders.

These sort of acquisitions - others do it too, a particularly egregious one by Brookfield REIT a couple of years ago comes to mind - should be prohibited by SEBI. Because these are quite clearly hurting us minority shareholders and benefiting only the promoters/sponsors.

On the other hand - I still have a tactical allocation to IRB InvIT Fund, having entered only recently. I will keep it for now, because this seems to be the only InvIT undervalued in the market as of now. But these sort of actions illustrate that there is probably a good reason why it is undervalued.

2 Likes

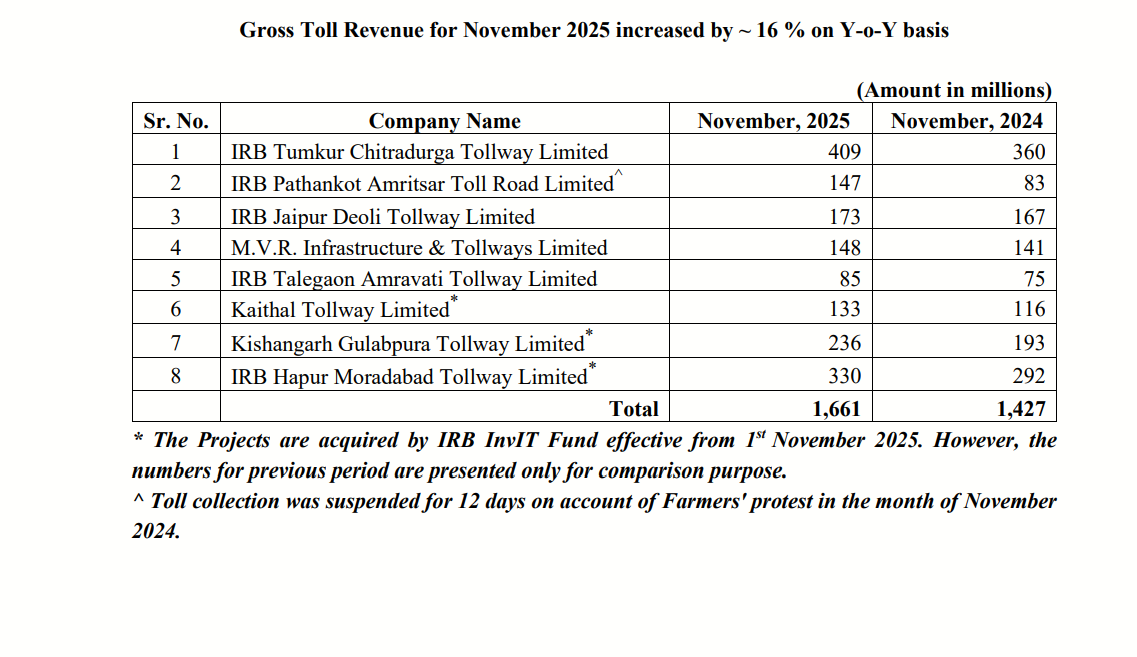

This is the 1st toll collection report, after acquisition of the 3 assets (6/7/8 above)

Report came on 9th Dec at the exchange…Pathankot is not a direct comparison across years,so, read the fine print below the table

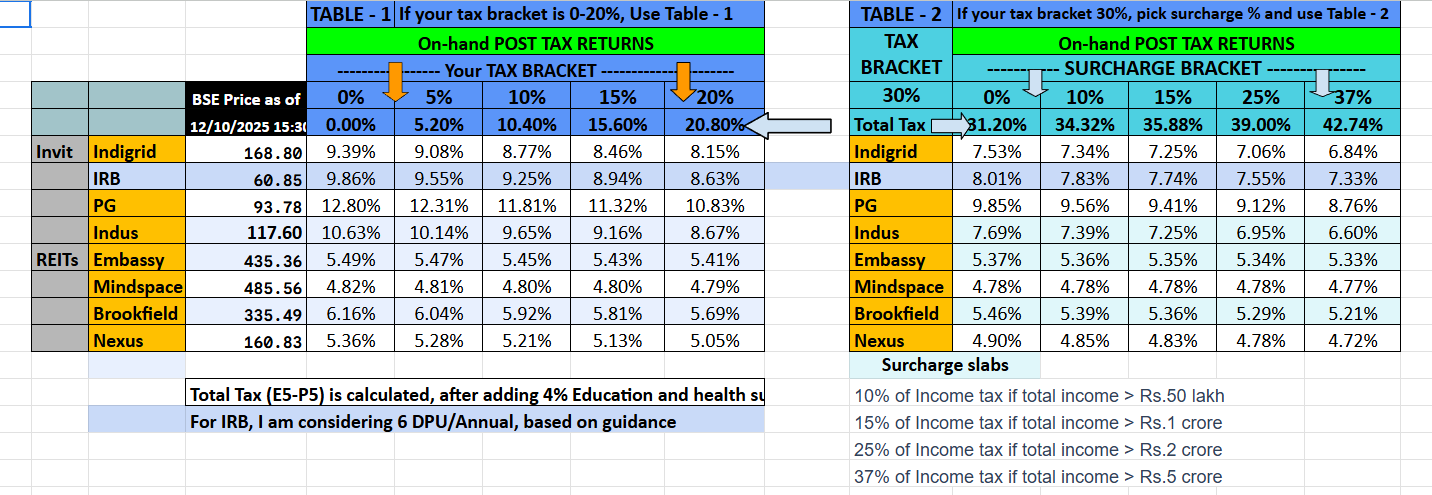

Post tax Yield tables, based on running 4 qtrs…before you deep dive into the numbers, here are some important points to be read

- The separation of taxable and non-taxable is a tedious job and one can be only sure, if you have the distribution advice (one can look at the TDS and if there is TDS, I take it as taxable). Since I don’t own every single REIT and INVIT below, there can be an odd mistake but that is why, I am giving the underlying table, that feeds into this yield calculation. I am no expert in Tax and hence do your diligence

- The fine print in IRB’s case is that, I have assumed, the last qtr payment of 1.5 DPU (and its breakup) as the common one across the entire year since using the previous 2 DPU will not give the correct picture

- The intent as always is that , if you go and buy these instruments today morning at 9.15 AM (assuming they open at the previous day close price), then what will be the yield on hand? that is the intent…

- Comments are always welcome

2 Likes

After holding almost for 8 years (First purchase being 6 May 2018 at around Rs 78/unit, and followed with multiple purchase sell in various family members name, I am finally exit from IRB InvIT today and switching my holding in India Grid InvIT.

Reason for exit:

At expected distribution of Rs 6 per unit for IRB InvIT for FY26 (current price Rs 62, Yield 9.7%) and Rs 16.2 per unit for India Grid InvIT (current price Rs 162, Yield 10%), I find risk reward being more favourable.

Further, the management conduct in acquisition of new assets in IRB InvIT was not at all favourable to existing investor. If you are willing to sell unit at 62/unit when declared NAV of 95.64 unit declared in 31 March 2025, the economic value of NAV become completely irrelevant in my view. How can management agree to dilute something valued at Rs 95 to be sold at Rs 62/unit? I did not find that action suitable. Only way to justify such action is case new issue happen in Right whereby all shareholder get pro-rate benefit (like India Grid did Right issue at Rs 100 when market price was around Rs 130). After this development, I was not comfortable to hold unit for long term. In order to command respect from world, one need to respect self-first. If the management themselves have no trust in NAV (which is demonstrated by diluting unit capital more than 35% discount, Rs 95 being NAV dilution at Rs 60), from wherer the investor would get confidence? When they do not support Minority shareholder with pathetic track record on distribution, why investor shall support such management? In my view, I made mistake of evaluating management qaulity. Having said that, It is my error and I am solely responsible for my expectation. During interaction over con call and also AGM meeting attended, I got multiple indications which I ignored.

Second point, Management acquisition of assets also has not been great in past record. Management acquired three assets Jaipur Deoli, Pathankot and Vadodara Kim (HAM assets). If distribution to unit and unit listed price anything to go by, the assets failed to deliver promised yield in my opinion. Partially, it could be attributed to external challenging environment like Covid crisis, Mine litigation stay (for Jaipur Deoli assets) and Farmer protest and Operation Sindoor (For Pathankot Highway). However, net result is decline in distribution from Rs 3 per unit to Rs 1.5 per unit per quarter and decline in price from Rs 100 per issue (IPO price) to Rs 62 currently. We need to consider that IRB has distributed ~ Rs 76 per unit as distribution since listing. However, IndiaGrid, which listed at almost same period, with IPO price Rs 102, Total cumulative distribution much higher at Rs 89 per unit and Current market price of Rs 160+ has done much better. While the business segment wise Road and Transmission line have different environment, but as an Investor, I would look at actual return I receive. Normally, Transmission assets have lower risk and volatility and hence offer lower return, while Toll Road assets have higher volatility and risk and hence shall offer higher yield to investor. In past, the performance was opposite of my expectation.

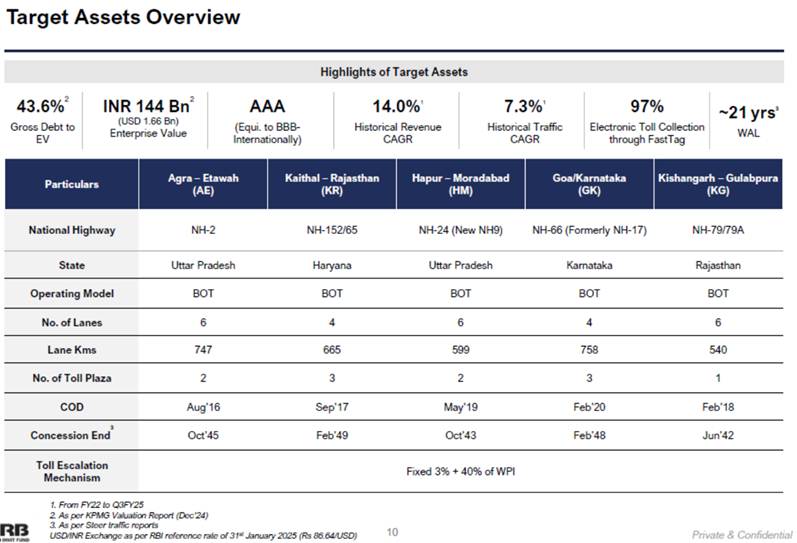

Further, declining revenue of three new acquisition assets does give discomfort of wrong selection of assets. Enclosing details of 5 assets offered to InvIT

Final purchase by InvIT excluded Goa-Karnataka and Agra Etawah. While there could some other commercial factor which management may have considered in avoiding these assets, I did not find commercial sense in acquiring selecting assets with decline in revenue in last 3 years, They could have avoided that asset as well.

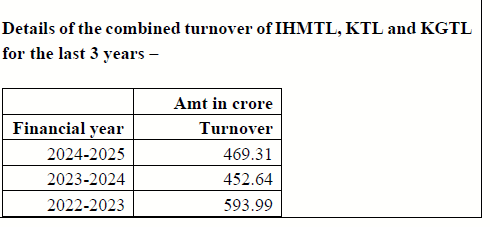

Enclosed details of three acquisition assets revenue during last 3 years. It declined from Rs 593 Cr FY2023 to Rs 469 Cr during FY2025.

I am not comfortable with such assets. Hence, decided to exit from IRB InvIT and switch to IndiaGrid InvIT.

Disclosure: My view may be negatively biased due to from exit from IRB InvIT. I am not an expert and my understanding may be wrong. I do not recommend any investment action. I am not SEBI registered adviser.

23 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2b87a6e6-6511-4d85-8a26-41a77c97f29a.pdf

1.5 is the DPU…..news came out, about 1/2 hour before market close today

1 Like

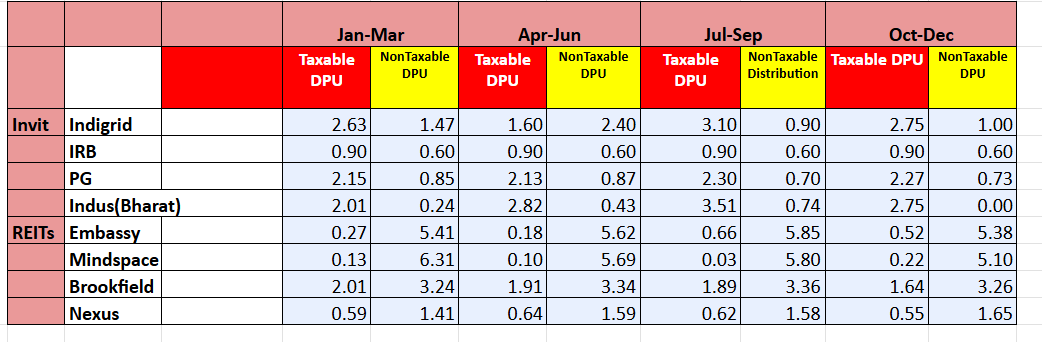

with Oct-Dec Qtr DPU updated, here are the yield tables and the underlying DPU info that feeds into it….Pl read the fine print of disclaimers, from my post above (July-Sept yield) before taking this as gospel or acting on this. Do your due diligence before acting on this

2 Likes

In Feb 2026 toll collection across 8 BOT project has shown 13% all round growth. Both 5 old project and 3 new BOT project has shown growth. I think this growth is underlined by traffic growth.

Quarterly results. First full quarter, after assets addition and hence not easy to compare financials.

DPU - minor uptick but with heavy interest (and hence higher tax outgo for the investor) to 1.6

“Declared 4th distribution of Rs. 1.60 /- per Unit, for the financial year 2025-26. The distribution will be paid as Rs. 1.44 /- per Unit as Interest, Re. 0.12 /- per unit as return of capital subject to applicable taxes, if any and Re. 0.04 /- per unit as exempt dividend”

NAV 81.26, for what it is worth (CMP 61)

Results came out a few minutes ago, before market closure

2 Likes

Proposal offer from the Private invit to IRB public invit

1 Like