Astron Paper & Board Mill Limited

Story

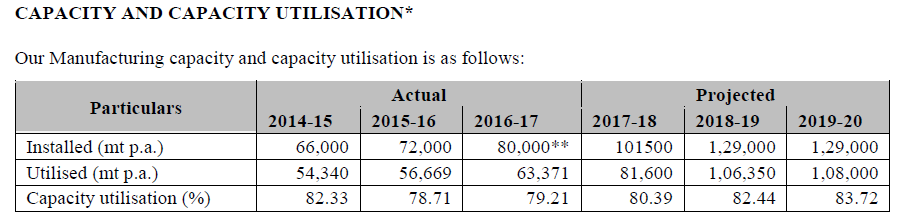

Astron Paper is a manufacturer of Kraft (brown) paper used in manufacturing of corrugated boxes. Unlike newsprint and writing and printing paper which use wood or bamboo as raw material, it uses waste paper as raw material sourced from UK and US. Company has a manufacturing capacity of 96,000 mtpa and production for FY 2017 was 63,371 mtpa. Company is planning to raise capacity to 129,000 mtpa and plans to raise production to 106,350 by FY2019. Company is planning for nearly 65% jump in production in 2 years. In comparison company has raised capacity by 25% and production by 20% in last 2 years.

Company’s competitors are Shree Ajit Paper and Pulp, Genus Paper and South India Paper Mills.

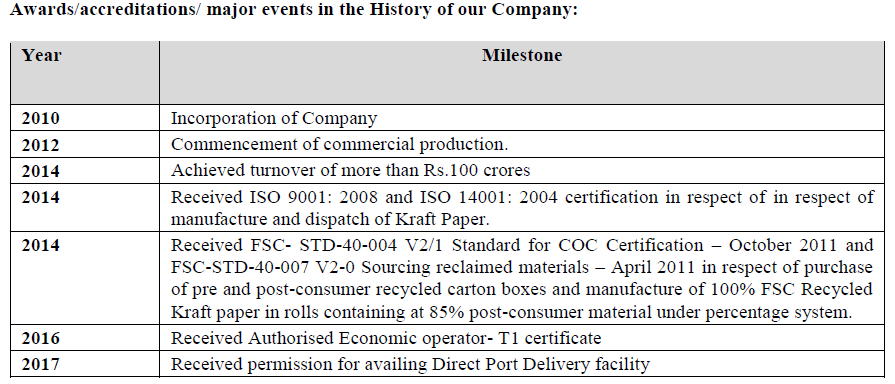

Brief History

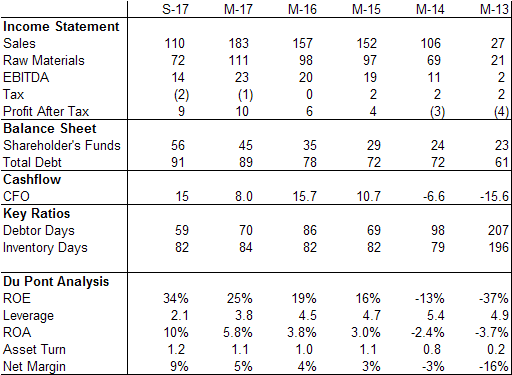

Financials

Company has become profitable in last 3 years. Before that it was profitable at EBITDA level. EBITDA margins have remained stagnant at 13% while net margins have improved from 3% to 9%. Debtor days are higher than normal for a company making commodity products. This has caused CFO to lag net profits although cashflow has improved recently. ROE has steadily improved even though leverage has dropped because of rising margins. Lower interest costs coupled with lower taxes has resulted in higher net margins even though ebitda margins have remained stable at 13%.

Corporate Governance

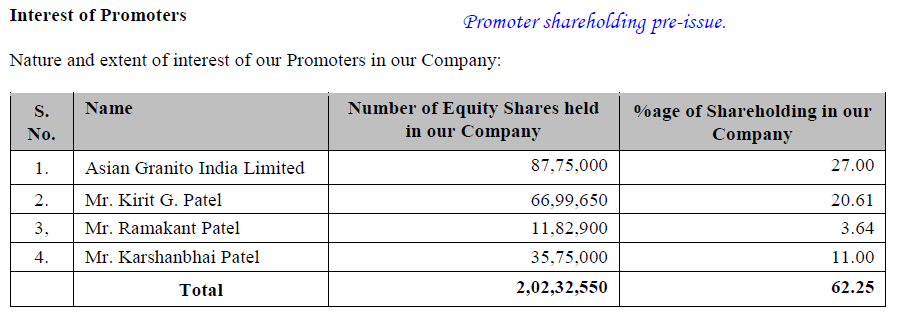

Company is promoted by 44 year old Kirit Patel, 51 year old Ramakant Patel, 64 year old Karshanbhai Patel along with Asian Granito India Limited. Kirit Patel holds a Bachelor of Commerce degree from Gujarat University. Kirit Patel and Ramakant Patel has 20 year experience in paper industry.

Post issue promoter shareholding will drop to 43%.

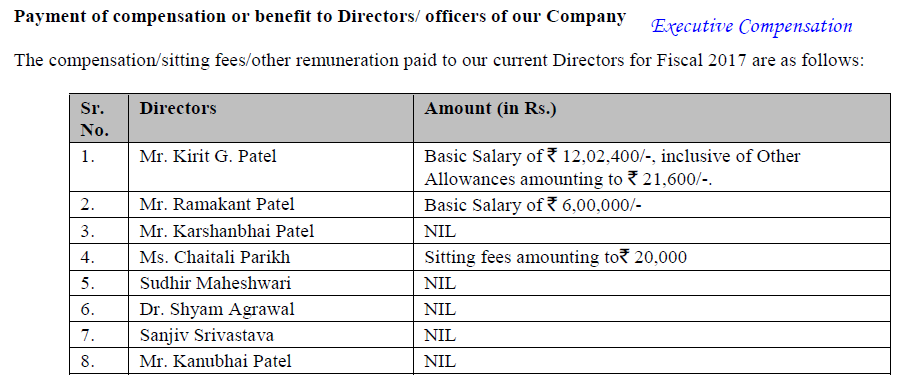

Executive compensation is low.

Dividends – No dividends are declared in last 5 years.

Tax payments – Company has not paid taxes in last 5 years mainly because accelerated depreciation has resulted in taxable income to be negative.

Debt repayments – Company has borrowed money in every year except 2015.

IPO Details

Company is selling 1.4 Cr shares at 50 rs per share to raise 70 cr. Shares outstanding post IPO will be 4.65 Cr.

Objects of the issue

Out of the 70 Cr raised, company plans to use 23cr to set up 33,000 mtpa plant, 8 cr for repayment of debt, 24 Cr for working capital and remaining (15 Cr) for general corporate purposes.

Valuation

Company is being valued at a valuation of 233 Cr on a post issue basis. On an estimated FY 18 PAT of 15 Cr shares are offered at PE of 15 and on a post issue book value of 110 Cr, P/B ratio works out to be 2.1. Company is more than doubling book value from 45 Cr to 110 Cr.

Investment Rationale

Company has managed good growth in last few years and generates good profitability going by the high ROE generated in recent years. Company is planning to raise production 65% in next two years which provides good visibility. Demand for kraft paper is growing as user industries like e-commerce and FMCG packaging are growing. Since company uses waste paper as raw material, shortage of raw material is not an issue.

Key Risks

- Kraft paper prices are currently on a cyclical high.

- Company margins may drop in near future.

- Drop in rupee is likely to cause drop in gross margins as raw materials is imported. Company has reported flat gross margins in last 5 years.

- Debtor days are high.

- Promoter holdings will drop to a low of 43% post issue.

- Company has not paid taxes in last 5 years.

Disc: Applying for IPO