Rajesh sharma Interview

Rajesh sharma Interview

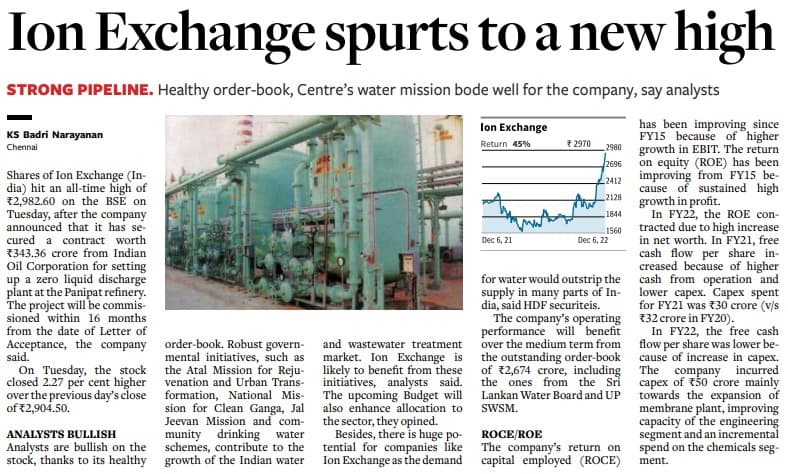

EC clearance for the chemical segment on the way, construction should start.

Ion exchange had about 2500 Cr engineering order book at end of FY 23.

order in bids ~8500 (assuming a 10% conversion rate, we get new orders worth ~800 Cr).

So total orderbook for enginereing alone stands at ~3300 Cr.

How long does it take for orders to be recognised as revenue on average ?

Can we assume that all of this is recognised in the next 4 years ?

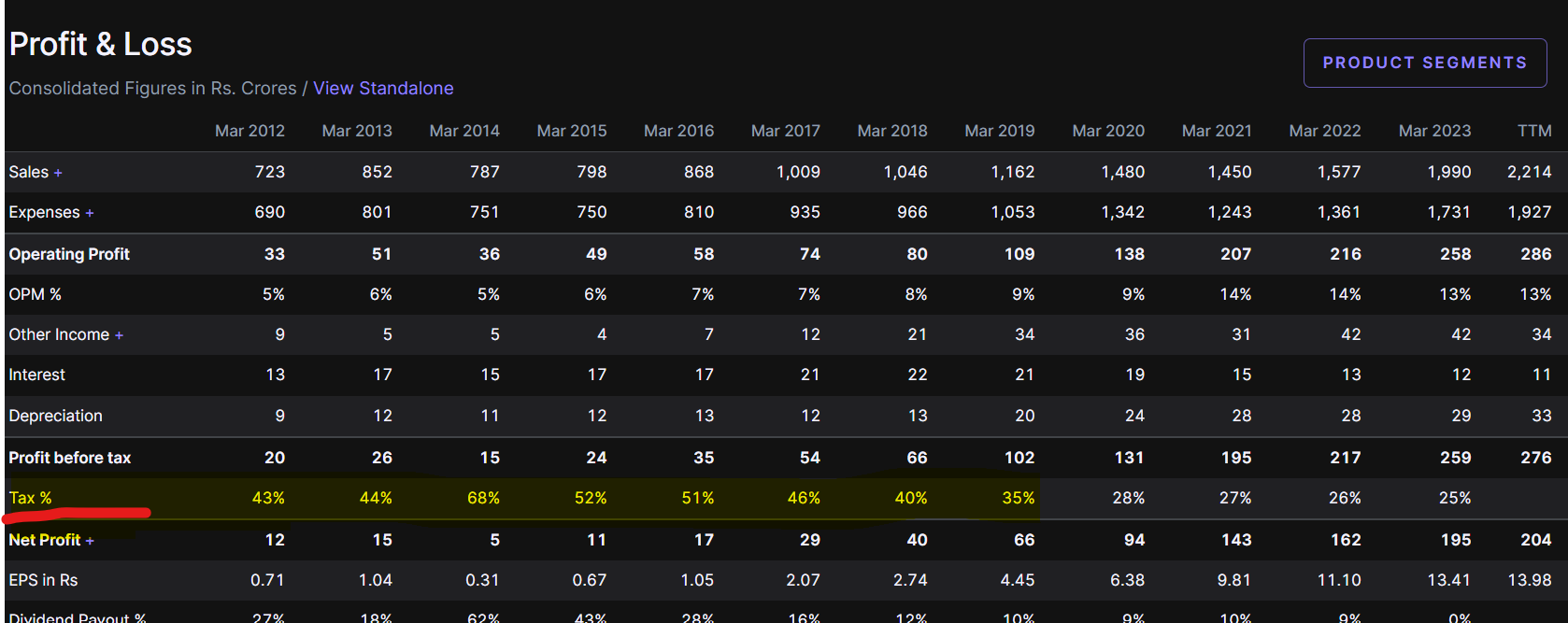

Now Engineering has been about 55-60% of overall revenue so we can assume that apart from this, chemicals and consumer will contribute about 1000 cr over the next 3 years (Assuming 30% of overall revenue).

So are we looking at close to 4000-4500Cr revenue by Fy 27?

That’s a really good growth rate at approximately 25% every year, which seems too good to be true.

What am I missing here?

I’m guessing enginereing growth rate is much higher than chemicals (which is growing at about 10%).

Even then , if chemicals and consumer can generate about 600Cr by FY 27 and Engineering can recognise ~3000 cr, that’s still about 3600-3800 Cr revenue which is a good 20% annualised growth

tracking - not invested

ion exchange is an incredibly amazing company, no two-ways about that however valuations are surpassingly piercing through the roof. moreover fundamentally speaking, one must not ignore the fact that engineering/water division which contributes about ~70% (q4fy23) to overall revenue pie got ferociously impacted as margins in the said segment nosedived ~1050 bps and the same is likely to weigh negatively in the ensuing quarters too!!

lopsidedly overvalued — its high time fellow investors

Sir I feel that most investors are awaiting their chemical resins plant capex to come onstream. Environmental Clearance has finally come, so it will take a year for the chemical plant to commercialize. Resins is high margin and ROCE, it’s a moat. Order inflow is strong so expect the water treatment segment to do well. Really wish they hived off the consumer biz which is a drag. If we look at numbers on a 2 year forward basis from here, I think the stock is at a slight premium and definitely a hold and by no means a buy at CMP.

Va Tech Wabag new CEO seems enterprising and I am bullish on their growth prospects. Valuations are favourable too in comparison to Ion.

Disc - My firm has recommended both Ion and Va Tech Wabag under our service. Va Tech Wabag is a part of our smallcase so I am biased.

How is the business model of Ion Exchange and Va Tech Wabag differnciated (excluding Chemical and Cusotmer Buisness).

Ion Exchange’s comprehensive water treatment & wastewater treatment solutions extend from influent water through potable and industrial process water; sea water desalination process, process separation, purification and catalysis; industrial effluent treatment, water reuse & zero liquid discharge and waste to energy solutions. Ion Exchange’s predesigned and pre-engineered water treatment, waste treatment and process water and non-water purification systems cater to a wide range of industries, institutions, communities, municipal & infrastructure segments.

Ion exchange is into Engineering business … so from where do they get done the PC part.

My notes from 2023 Annual report for Ion Exchange:

| Sr. No. | Description of Main Activity | Description of Business Activity | % Of the Turnover of the entity |

|---|---|---|---|

| 1 | Engineering Segment | Provides comprehensive and integrated services and solutions in water, wastewater treatment & solid waste management to industries & communities. This includes advanced Membranes & their applications in Sea Water desalination, Recycle, Zero Liquid Discharge, purification & concentration of process stream and integrated waste to energy systems with comprehensive operation and maintenance services. | 61% |

| 2 | Chemical Segment | Provides widest range of ion exchange resins, adsorbents, speciality process chemicals and customized chemical treatment programmes for various utility applications. | 29% |

| 3 | Consumer Product Segment | Caters to individual homes, realty, institutions like hotels, educational institutes, hospitals, railway and defence establishments, laboratories etc. To provide pure & safe drinking water and sustainable waste management. | 10% |

Segments:

With these the segment has visibility for sustaining growth in the next 2-3 years.

a. Home water solutions

b. Institutional segment

c. Commercial Water segment

d. Rural Segment

Exports ( 394 Crores for FY 23) - Having built a favourable position as a reliable exporter of quality ion exchange resins, two of its important markets, namely North America and Europe continued to be constrained due to economic and geopolitical reasons.

Digital: your Company launched their new Corporate (www.ionexchangeglobal.com) and Hydramem (www.hydramem.com) websites which were stronger in functionality, appearance and navigation. Development of the new regional websites for Asia Pacific, Africa, Europe, India, Middle East and North America widened our marketing and sales reach to global customers.

Risks and mitigation:

Ion exchange update

(From credit rating 2023 and investor presentation)

ION EXCHANGE

FUTURE GROWTH

1…Order book

=The engineering segment had orders worth Rs 3,351 crore as on June 30, 2023, with strong bid pipeline of ~Rs 8,500 crore offers strong revenue visibility

2…Recent acquisition

=Recent acquisition of a Portugal based company MAPRIL (acquisition completed in Q1FY2024 at a total consideration of ~Rs 24 crore, funded from internal accruals), will provide better access to the European market and increase the product offerings in chemical division.

3…Greenfield expansion

=Greenfield expansion in the chemical division for Resins manufacturing in Roha, Maharashtra with an estimated capex outlay of ~Rs 400 crore (to be funded in the debt equity ratio of 4:1), to be phased out in fiscal 2024 and fiscal 2025, the debt tie-up is already in place.

=The company’s ability to commission the Roha project within the budgeted cost and estimated timeframe, stabilize the facilities and ramp up sales post commissioning would be a key monitorable.

4…Market potential

A…Sewage(Municipality)

= Study by the Central Pollution Control Board (CPCB) has revealed that almost72,368 MLD of sewage is generated across urban India and there are just 1,093 STPs installed that treat 31,841 MLD or 44% of sewage per day

B…Industrial

=• In India only 60% of industrial

wastewater is treated.

• Around 40% of the STPs do not conform to the environment protection

C…Nal se jal

=Following the announcement of the

‘Har Ghar Nal se Jal’ scheme on August 15, 2019, it has provided tap water

supply to more than 12 crore rural

households.

= At the time of announcement of the Mission, out of 19.27 crore households in the country

only 3.23 crore (17%) had tap water

connections.

D…SWACHH BHARAT ABHIYAN

=Namami Gange” the clean Ganga

initiative, can create significant

opportunities.

=INR 200 bn (USD 3 bn) has been pledged by the government over the next five yearsto clean up the Ganga.

5…After sale services

=Longstanding presence of the promoters and a robust nationwide aftersales service have helped the group to establish the brand.

Disc…invested since 2020

Pretty Good result:

I know few popular investors and funds have reduced their stakes of late concerning over valuations.

Disclosure: Considering the current quarterly result i will stay invested.

P/BV is very high according to current market price.

The Chemical segment is very profitable, and the upcoming CapEx @ Roha, Orissa worth of Rs 400 Cr will be capitalized in FY26.The Fixed Assets Turnover in this segment at 1.8x-2x at peak level.

I am analysing Ion exchange result. The ROE and ROCE is very good for the company and PE is in good range, not too over valued.

company has a consumer product business which is consistently loss making.

the chemical business is the cash cow. I am not sure, why company is not taking steps on the consumer business. it is in loss since 2014.

i need to analyse further. Have not taken any position yet. but curious.

They don’t do advertisement but are doing innovations in consumer products .The consumer prd. division is about to break even in quarter or two.

Water.pdf (1.9 MB)

Useful report to understand Water business in India.

Any particular reason there has been continuous sell-off ?

yes, same question from my side. is the promotor selling off its stake ?

It is fairly overvalued!! And it has gone up significantly before this selloff!! also in last concall it was mentioned that they see a slight slow down in order pipe line along with slow down in engineering division!!