Thanks @desaidhwanil for sharing your thoughts and presentation. I have been following your threads for quite some time now and have learnt so much from your writings. Keep sharing.

Operating leverage is an interesting investing strategy. I am trying to take this discussion further with couple of examples purely from learning perspective.

(Discl: I do not have any positions in any of the below mentioned companies and also don’t have buy/sell view).

Operating leverage plays well in capital intensive companies where majority of the operating costs are fixed.

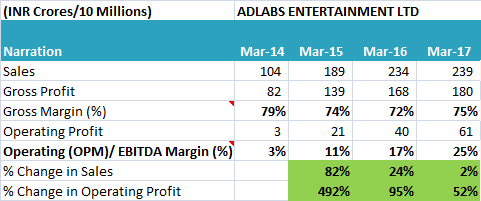

Look at the below example of Adlabs Entertainment Ltd. They set up a theme park Adlabs Imagica, which became fully operational from November 2013. There was an initial capital outlay of approx. Rs.1,470 cr. to set up this theme park. As majority of the capex is already incurred with huge capacity, there are very minimal expenses to be incurred to generate additional sales.

As can be seen, the OPM has increased from 3.34% in 2014 to 25.46% in 2017. This is clearly due to better capacity utilisation (footfalls in case of a theme park).

For the year 2017, mere 2% change in sales has led to 52% change in Operating profit.

There is no growth in footfalls in 2017 when compared with 2016, still OPM has increased by approx. 8% (from 17% to 25%). This is mainly due to increase in Gross realisation per visitor.

Thus, increase in capacity utilisation / increase in sales price can lead to high OPM for companies with high fixed operating expenses.

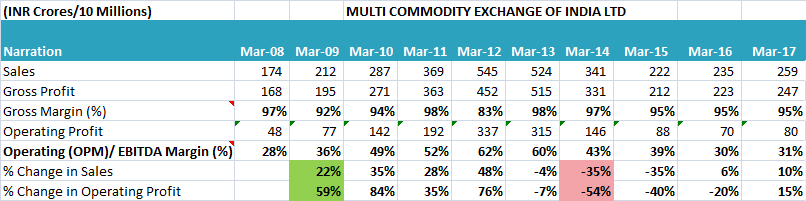

As pointed out by Dhwanil, operating leverage is a double edged sword. Let’s look at the below example of MCX where Operating leverage has played negative role with sudden lower capacity utilisation.

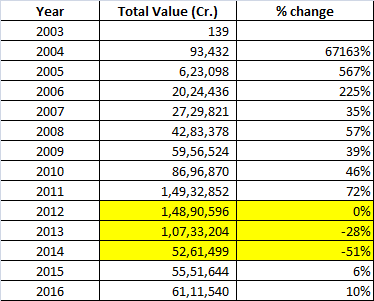

Below table shows total contract values for different years. The value continuously kept increasing upto 2012 and then there was a sharp decline in the years 2013 and 2014. There were multiple factors for this sharp decline like imposition of Commodities Transaction Tax and stability in the prices of precious metals which constitutes major portion of MCX’s trading value. This coupled with NSEL scam (promoter group company) led to sharp correction in the stock price at that time. Understanding of operating leverage can help to value the company differently in such scenarios. Dhwanil has very well articulated his thoughts in MCX thread.

Source: Historical Data

Below table shows that in the initial years, as the volume and value of the traded contracts on the exchange grew, operating leverage played a positive role (Positive disproportionate change in Operating profit compared to change in sales).

However, as the volumes and value of the traded contracts declined in the year 2013-2014, there was a negative disproportionate change in Operating profit. 35% reduction in sales led to 54% reduction in Operating profit.

MCX has built a platform which has handling capacity of 40,000,000 transactions (Orders and Trades put together) per day, which is well above the record volumes witnessed by the Exchange till date (As per AR 2017). This means that there is huge operating leverage and any change in sales (positive or negative) will have disproportionate impact on bottomline.

Dhwanil has pointed out in the presentation in slide 8 - “Typically, businesses with high gross margins may have high operating leverage”. Both the above companies have Gross margin of 75% and 95% respectively.

Requesting all members to please their thoughts.

Discl: Companies mentioned above are for learning purpose only. Both companies have very different capital structure. Adlabs has huge debt which is not able to generate sufficient operating cash flows to service interest payments and also need to incur high maintenance CAPEX. MCX on the other hand does not have any debt and generates surplus cash. Investment decision should be based on various such other factors.

No buy/sell recommendation. No holdings in any of the company.