Adding on to what @Chandragupta has said, let me quote some real life examples where ignoring these ratios led to reverse compounding of investors’ wealth ![]()

These are cases of investors who ignored CFO vs PAT and got caught on the wrong wicket.

Note: This isn’t to pin point faults in any investor’s analysis. All of us are learning and making mistakes is the tuition fee we pay to the market. And these case studies are vicarious experiences for normal mortals like all of us.

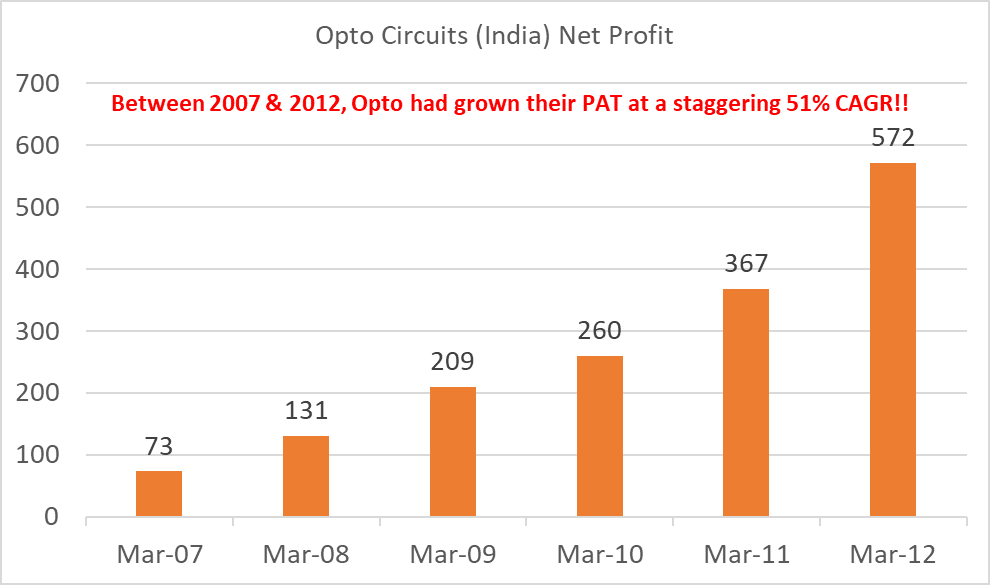

Case 1 - Opto Circuits

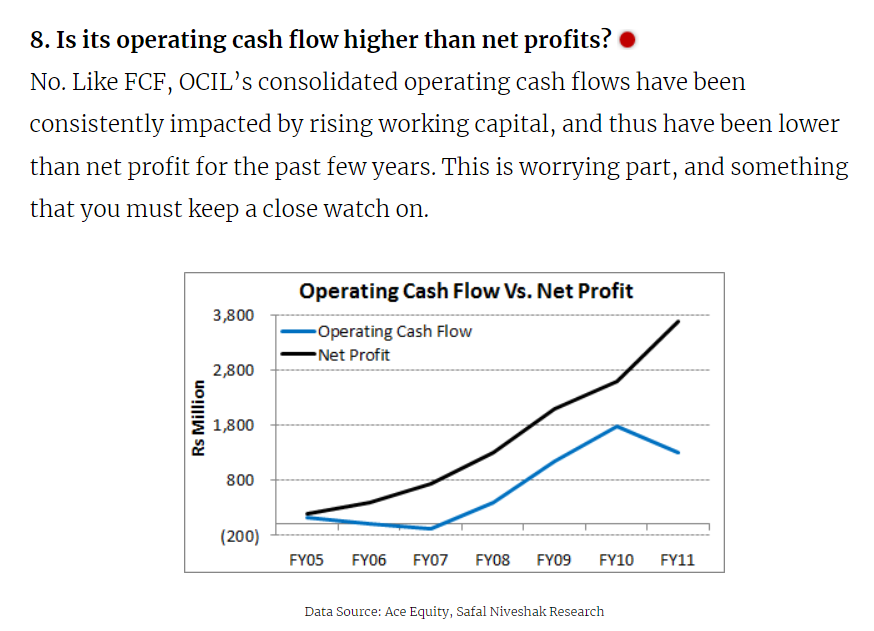

In this article, Vishal had analyzed Opto in depth and these were his observations about CFO vs PAT.

Yet, he did not pay give enough weight to CFO vs PAT, went ahead and invested. Perhaps, a lot of growth investors like myself, might have done so too, because their growth was mesmerizing.

And here’s what happened to the stock price subsequently,

To Vishal’s credit, he publicly accepted that his investment thesis had been broken at the hip. (Not every blogger is bold enough to do this. Unlike Vishal, some others just try to push things under the rug

Case 2 - Photoquip India

In this case, Amit Arora talks about his experience with Photoquip India, which he picked up in 2011. Since this is a paid article, I don’t want to quote anything written in it. But the gist of the story is he trusted the management at face value.

What was missing in the article though was that cash flows were lacking before, during and after he’d invested.

And here’s the subsequent downfall in the company’s stock price.

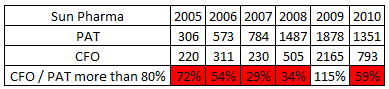

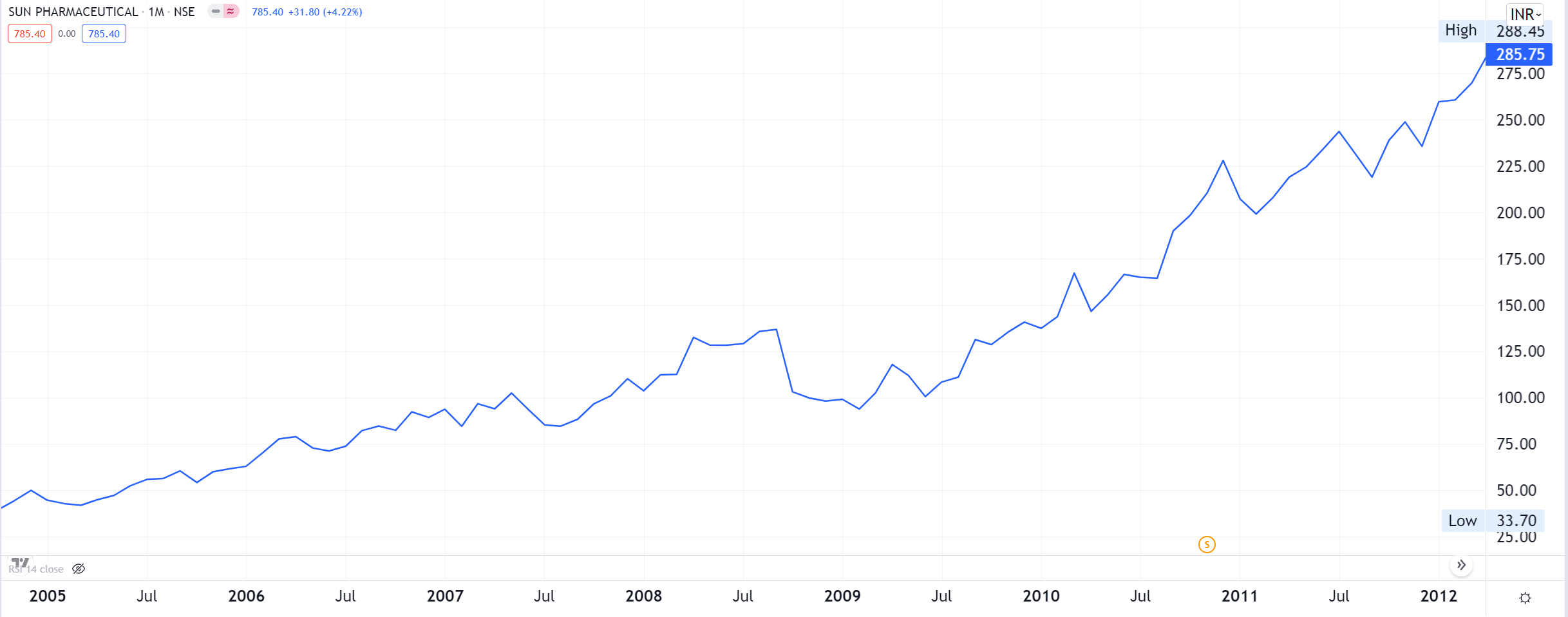

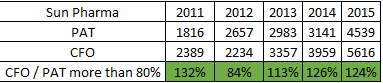

Case 3 - Sun Pharma

Here’s some disconfirming evidence that can be very baffling. Between 2005 & 2010, Sun Pharma’s CFO consistently stayed below the 80% threshold (barring 2009).

Yet their stock was rocking because the market believed in the promoter’s ability to turn things around from a cash flow perspective.

And indeed, they did manage to improve their cash flow subsequently.

Case 4 - Laurus Labs in July 2020

Some investors were worried about Laurus’ receivables being high and chose to skip investing in its stock. In effect they were saying, Laurus’ future CFO would be impacted because cash would be stuck in receivables and some of those receivables would become bad debts and would therefore lead to cash flow problems for the co.

What they missed is that receivables in pharma usually don’t end up being bad debts and write offs because relationships between pharma cos and their clients are multi year and there is a lot of inter dependence. If one of Laurus’ large clients defaulted or delayed payments, Laurus could simply cut-off future supplies to that party and start recovery. (Hitesh bhai had written about this aspect somewhere, but I can’t remember where)

Besides who were these clients that owed money to Laurus? Were they some fly by night operators that would vanish into thin air some day? Or were these clients big MNCs that could potentially delay but not deny payments to Laurus? In my view, the answer was the latter and hence I took a big position despite their receivables being high, at 102 days at the time.

To conclude, like any other metric, a low CFO vs PAT can tell you there’s something getting cooked in the books. Yet, as the case of Sun Pharma shows, if the jockey is good, he can turn things around and CFO doesn’t become a problem then.

Too many times, we get stuck up on a single metric and let go of some great opportunities, without looking at the grand scheme of things instead.