Some highlights from AR

Path forward per letter to shareholders

We believe that significant growth potential exists in cross-selling more products to our existing Customer base, extending a product to more customers

in the same geography based on the success of the first Go live, expansion to new geographies, distribution of products through the Cloud deployment model and deepening the engagement with key accounts adopting a customer-centric approach to their Business transformation or operations

transformation initiatives. These will drive the next successive waves of our growth roadmap. Apart from chosen geographies where we have a direct sales presence, we are also expanding into new geographies

successfully through Partnerships/ Strategic alliances. In addition, the next wave of products reaching the monetisation phase – Data and IDX, iWealth, Treasury & Markets and the next stage of growth anticipated in the GeM platform would also further augment our growth agenda

Competetion - a key point to observe

Given the spread of our Product portfolio as well as geographic reach, we do not have a single or a few competitors across the Board. Competition

varies with Product / Line of Business and Geography.

- In Consumer Banking, our competitors are Mambu, Thought Machine, nCino, Temenos, Oracle Flexcube, Infosys Finacle and TCS Bancs.

- In Corporate Banking, we have Finastra , Bottomline Technologies, ACI, Reval competing against us,

- while in Treasury, it’s Finastra , Guava and Finacle.

- In Insurance, we compete with Guidewire, Duck Creek and Carpe Data

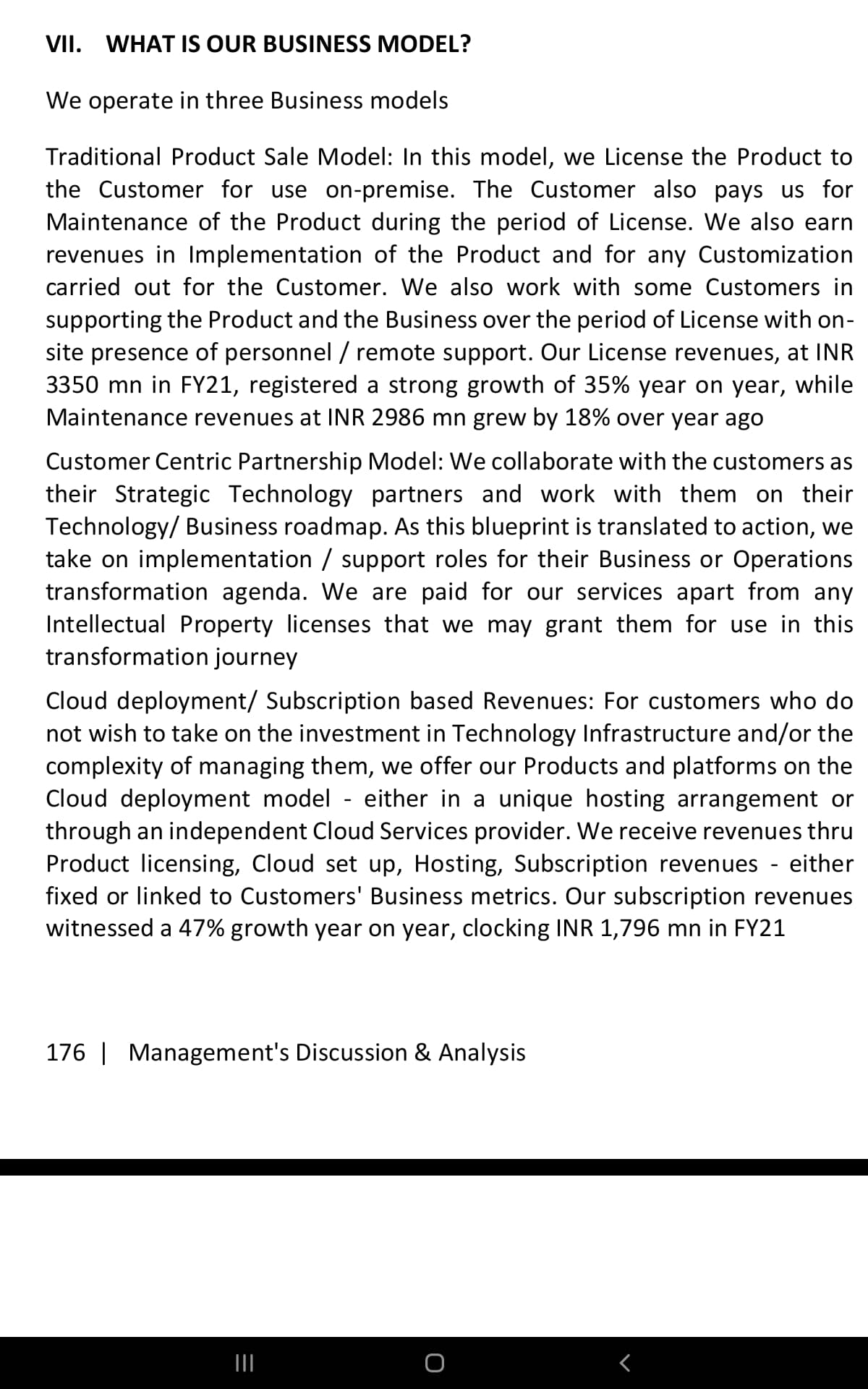

Business Model

Note the contrast in Traditional vs Cloud/subscription model in terms of former being heavy on front loaded revenue ( good for near term performance) vs latter which is superior on life time value and margins as well as business visibility ( superior for long term performance and stickiness) - these both form 56% revenue, middle one which is more services based( more like a door opener to build relationships and eventually push products in either forms)

Future performance

Inferences

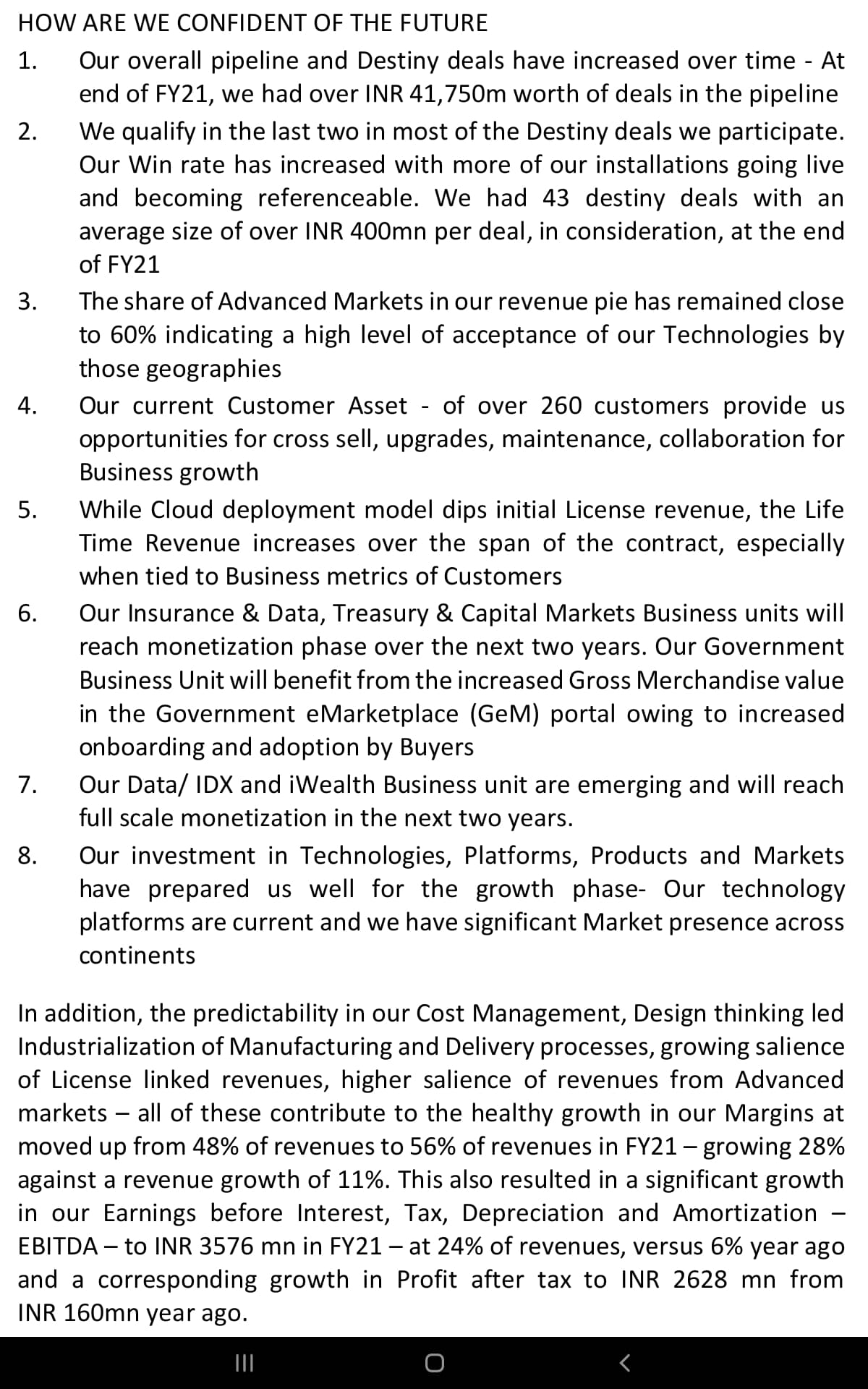

- Pipeline close to 3X FY 21 revenue - approx half of that is destiny deals - where they reach in last two.

- Destiny deals - 43 deals in consideration with avg 40 cr+ deal size. They are in last two in most of destiny deals - reflects well designed sales lead qualifications and pre sales efficiency.

- Developed mkt share at 60% - higher margins- supporting upcoming product lines and lower margin emerging Geo - This mix improvement will aid margins.

- GCB and GTB are doing hevaylifting and next phase products per #6 above for monetization over next 2 years( by FY 24)

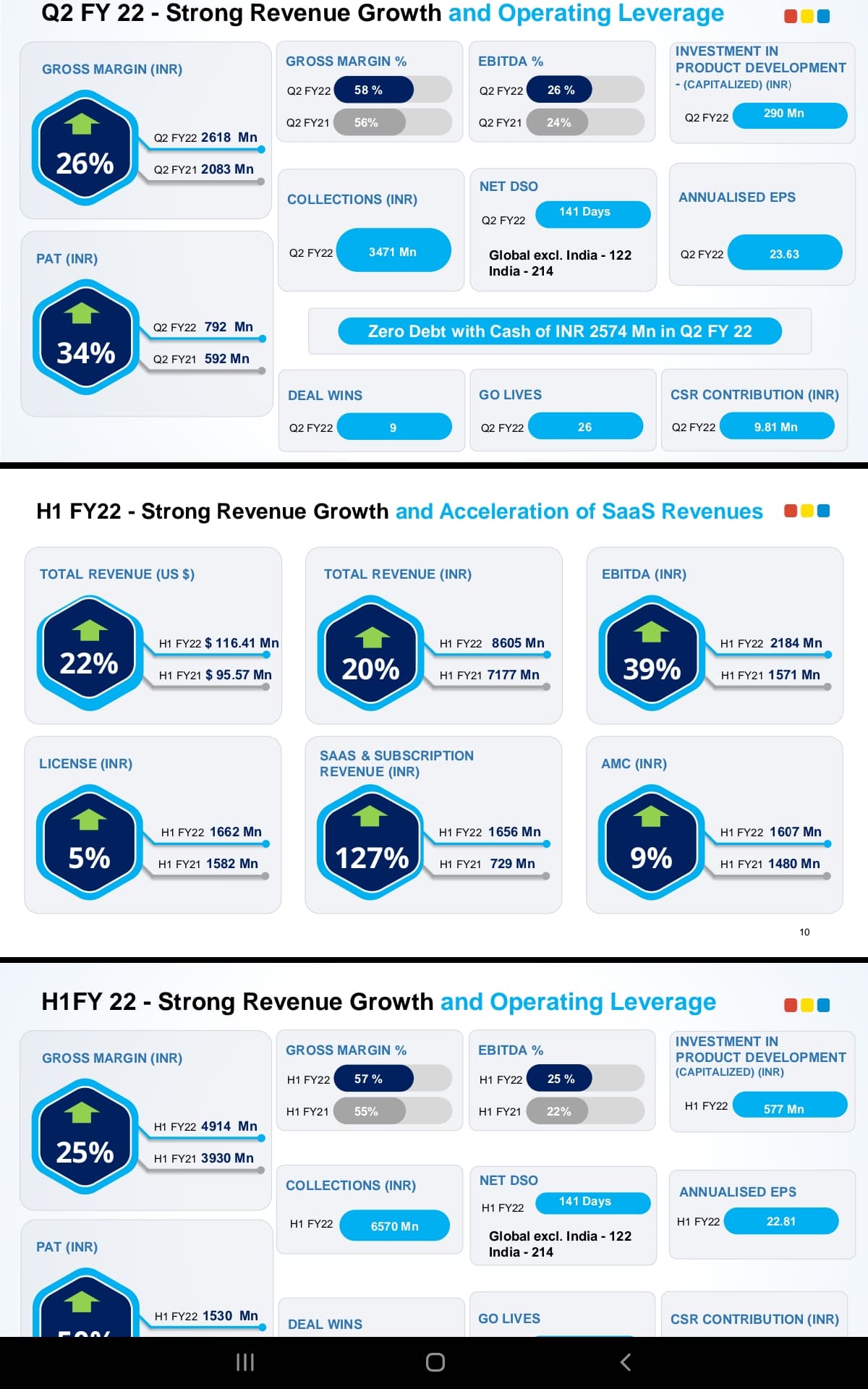

- FY 21 has seen heavy operating leverage kick in with EBDITA increasing many folds vs mid double digit revenue growth. In other words two product lines ( GCB and GTB) has delivered these results - three more product lines are likely to go through similar monetization journey( Insurance & data, capital markets , GeM) - with all five products firing by FY24 they can be be in a different orbit - of course market will reward them much before it happens- need to track it closely.

This 2+ year journey when all 5 product lines start firing , is likely to have some hiccups - such as Q1 22 where commentary around margins and insider trading incident spooked thus realtive underperformance in last 2 months.

Key points to track

- Mid teen growth in sales and texture of win by products per deal, destiny deal wins and revenue mix from developing vs developed mkts - at 260+ active customers ( avg 6 cr type revenue per customer is quite low - in other word sales efforts are done for entry in door, time to cross/up sell ), lot of cross selling has to happen hence from hunting to account mining

- EBDITA margin band annualized( 25 to 26%), suspect that given 3 new product lines being in GTM phase will be demanding for matured products doing hevaylifting, there could be quarterly gyrations - however winning trajectory of deals in developed markets and account mining/cross sell should help

- Subscription linked rev growth and share - there is trade off on going heavy here as impacts short term numbers- a calibrated approach with mix going up balanced way is good for long term and valuations.

- Any material incidents in perception around governance quality

- Healthy cash in hand and future cash flows - capital allocation

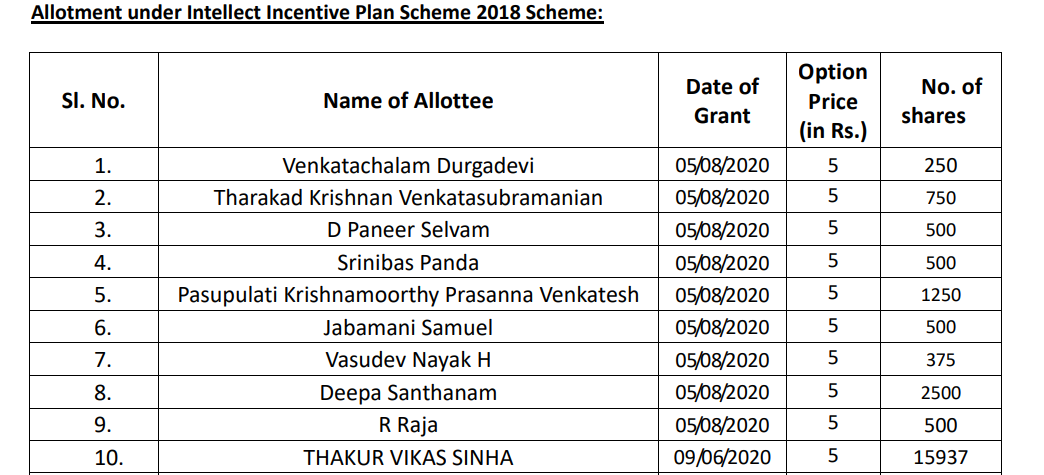

For folks getting annoyed with insider selling and exercise prices being very low to CMP can refer AR, has transparency on what/when/why of multiple ESOP plans as well as Q1 21( corona times) steep price drop causing revision in policy - again individual calls - don’t want to miss forests for trees. Believe ESOP will help mitigate skill crunch to some extent in current times.

All in all they are at TTM 1550 cr revenue ( licencse/subscription inching close to 60%) , 380+ cr op margins at 24%, near 300 cr profit ( much higher cash generation), Net cash positive. Available at 9K cr mkt cap, potenyialy less than 23X EBDITA, 5.5X sales on FY 22 numbers at mid teen revenue and slightly higher profit growth, and very healthy cash flows.

We have many midcap IT service commanding 10 to 20X sales or 25 to 40 X EBDITA.