Sir,

I agree with the view that it is not in Interest of existing Investors to Buyback at a Higher Price. My understanding is that the management is doing this buyback to satisfy PE Investors who demand that the company give performance in their private management interaction.

In the larger context of 2 issues plaguing the Co. i.e. Mr. Ravi’s resignation and racial discrimination case in US. The management need not answer the uncomfortable questions and can simply deflect attention to Buyback. For shareholders making money is the most important thing. In the longer term it is simply favouring the outgoing investors, rather than adding value to all the investors.

This also shows lack of creativity of management. It should have saved the cash kitty to buy companies adding value in the downturn if at all it is realised.

Why it is not in interest of existing shareholders to buy at higher price? Can you elaborate and your views on resignation will also help us to understand more?

Cash in the balance sheet belongs to existing shareholders. If that cash is used to purchase shares at higher price, than market price, then its misallocation of capital…its like purchasing the company by paying higher price than it deserves.

There is an ancestral house which true value is 2 crore.

This is jointly owned by two brothers.

So one of them should pay 1.1 crore to buy the one half that is owned by the other brother.

Is it good business acumen for the first brother?

The shareholders who quit (by selling in the buyback at high price) get more money than what they should get.

The shareholders who stay back (because they are the ones who pay when the company pays) have to pay more than the intrinsic value to the ones who sold their stocks.

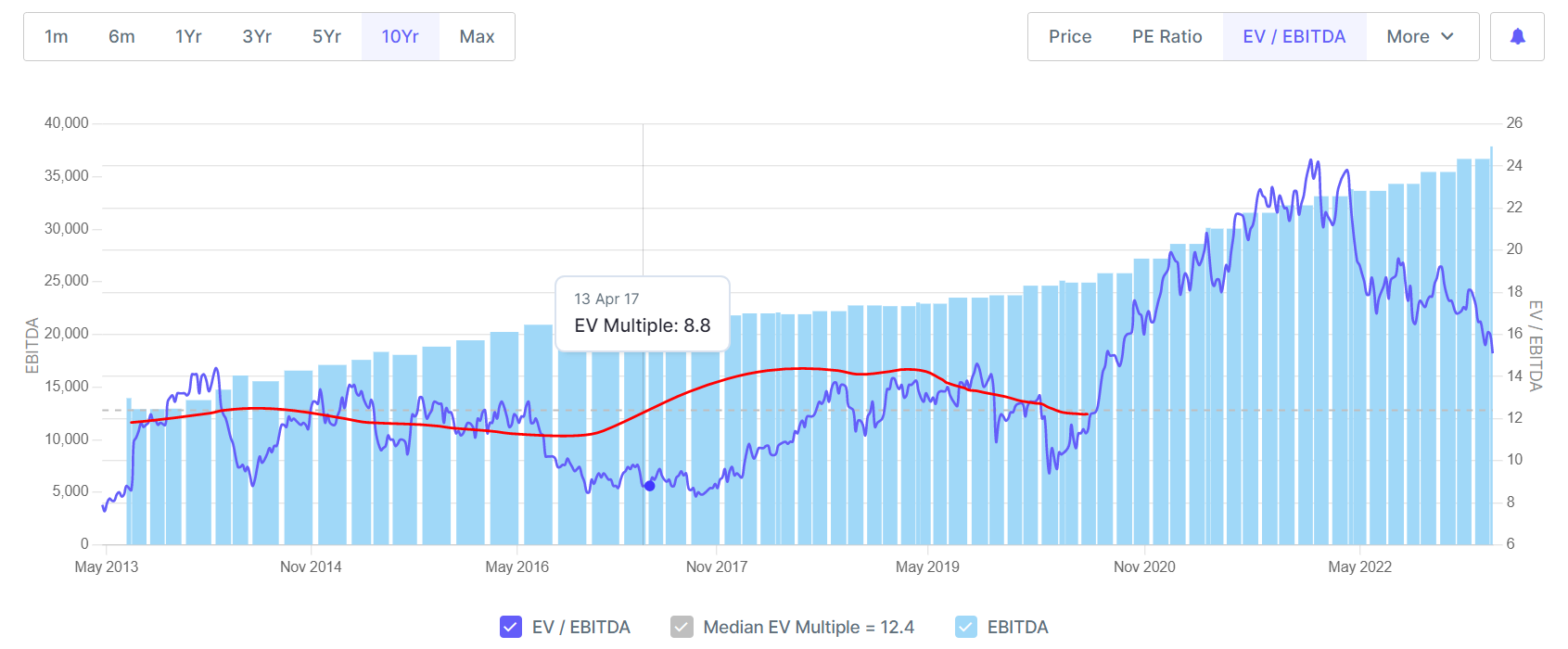

Thanks for clarity…But as far as I know this is not buy back through tender route. Here company will buy at existing market price subject to max of 1850 and company is only bind to buy 50% of buyback amount.

So warren buffets point about buying back shares is simple. He would buyback when the prices are below the intrinsic value or fair value.

Also if there are avenues to increase the ROI by investing the shareholder’s money in better places.

When the company has no good allocation of the cash in books, they have two options either to give away dividends or to buyback. Dividends leads to tax liabilities on the shareholders. So buybacks which attract capital gains taxes are the route they reward existing shareholders.

My hunch: Large shareholders wont get affected bcos on one hand they will pay higher to the seller (themselves) and on the other hand they will get the same higher money (themselves) So for them it should be net neutral. ( some more erudite member might give more insight into this hunch of mine mathematically)

Management of any company has duty to allocate capital prudently, we can all agree on it.

Lets take a hypothetical case of TCS buying Infy. Today Infy is trading at Rs. 1500 (approx.). Lets suppose we are TCS Management now should we buy at Rs.1500/ Rs. 1300 / Rs. 1600. The answer is quiet simple buying low will help TCS share holders. I hope no confusion there.

The same logic applies to TCS as well even if we buy our own stock we should buy it as cheaply as possible. Then a question on why TCS and Infy Mgmt are buying at a premium. This has 2 benefits 1. Posturing that we can easily earn our cash back 2. Institutional investors are required to show returns every year. If the share has performed badly in the market, they want the management to distribute cash to show superior returns for the time being, if not they will simply put pressure or get a new CEO.

With regard to Tender route, all Investors will place shares to get maximum offered price.

@Nishant_Sah Large shareholders(Read Tata’s or Murthy’s) are positively effected, as their share holding % remains the same but in addition they also get much needed cash for karcha pani.

@thakurvi If you are still not convinced, I have a mathematical model(Link). Please observe that lower the buyback price higher the EPS. So if same PE is maintained, higher the value to investors.

Strong Q3 performance with stable operating margins and broad-based growth.

Large deal value 3.3 billion USD with growth in digital revenue.

Margin and growth:

Strong Q3 performance with 13.7% YOY and 2.4% QOQ growth in a seasonally weak quarter

Stable operating margin at 21.5%. This because of cost optimization benefits plus healthy revenue growth.

Margin for 9 months FY23 at 21%, in line with guidance

Margins for FY23 remains between 21-22% with anticipation at lower ends.

Subcontractors reduced over last 3 quarters.

Growth in Q3 has been broad based with most industries and geographies growing in double digits.

Continue to gain market share, vendor consolidation underway. When there are 6-7 vendors and client want to narrow down to 1, 2 or 3, Infosys seems to be benefitting from these discussions.

Revenue growth guidance revised from 15-16% to 16-16.5%

Large deals, clients, and business outlook:

Large deal value 3.3 billion USD, 32 large deals, highest in 8 quarters.

7 in retail, 6 in financial services and communications, 5 each in EURS and manufacturing, 2 in life sciences and 1 in high-tech.

Region wise, 25 in the Americas, 5 in Europe and 2 in the rest of the world.

Digital revenue grew at 22% in the quarter and is close to 63% of overall revenue.

Very good new client acquisitions in Q3, with 134 new clients added in the quarter.

Number of $50 million clients increased by 15 to 79. Number of $200 million clients increased by 5. Number of $300 million clients increased by 3.

The attrition numbers are the lowest quarterly annualized attrition rates in the past 7 quarters. Attrition expected to reduce further in the near term.

Utilization levels (excluding trainees) reduced to 81.7%. This is due to seasonality and employees re-joining bench.

On-site assets mix stable at 24.5%

Cashflow, dividend and buybacks:

FCF for the quarter is $576 million, 72% of net profit conversion. YTD FCF $1.8 billion, conversion of 81% of net profits.

Q3 marks 30th consecutive quarter of positive forex income

Consolidated cash and investments declined from $4.79 billion last quarter to $3.91 billion. $1.32 billion returned to investors via interim dividend and ongoing buyback program.

Buyback program: initiated on December 7. So far 31.3 million shares worth INR4,790 crores or 51.5% of the total authorization of INR9,300 crores have been bought back. Average price of Rs. 1,531 per share (max. buyback price is Rs. 1,850 per share)

It is now widely known that Infy quietly invested $1 billion in Open AI in 2015, thanks to Vishal Sikka’s visionary leadership. With the recent impact that Open AI products, particularly ChatGPT4, have had, just curious if anyone has assessed how this 2015 investment will impact Infy’s revenue in the near future, given that OpenAI is currently valued at $24 billion with $200 million in revenue.

None. Infosys was a small investor (donor in early non-profit structure). It has no proprietary access to OpenAI. I assume only Microsoft has commercial access and will hold 49%.

This is probably one major area for improvement for IT companies in India.

Investment in future trends can generate immense revenue streams if you can foresee the future trends well in advance.

I keep seeing most of the managements of IT service companies have restricted approach when it comes to investing in future technologies and R&D and Build IPR around it, except few exceptions.

They were also against employees working from home till almost 2019 End and then suddenly they realized some benefits of it after March 2020. Complete 360 degree shift in their thought process due to pandemic, else they would have continued their traditional thought process (read reluctance to change!!). This lack of vision probably might have impacted their potential to attract lot of talent due to restricted approach.

Things are changing now for the good, and they have learnt their lessons. We have started seeing lot of investments in R&D, and Digital technologies now in the past 2-3 years in addition to flexible hybrid working models.

OpenAI is a non-profit. They have twisted arrangement with Microsoft which allows them to recover their expenses in developing their models and serving them. Infosys donated to OpenAI, they did not invest in it in a VC way.

As per street, average Q4 results, so much pessimistic analysts, stock may not be cheap but who knows where is bottom. I like the company & structural advantage for indian IT industry. What’s your view. Dividend & cash flow is good.

Disc : Holding 2 % of portfolio since before covid. Will add some during recent time. Allocation target 5%

Too much pessimism circulating for such respectable stock. I believe that the company, management, structural advantage is excellent and is not going to go away anytime soon. But the thing is, in 2021, market became too optimistic for IT cos. and that reflected in their share prices. Now when UK, US, etc. is going through high inflationary environment, cos. that depended on those clients are facing a setback. And this quarter’s results also came not so good. I believe there can be more pain ahead as Nifty It head towards 26400 levels. and this can extend till 8-12 months more. As valuations will meet reality. But nothing wrong with the co. for the long term.

Disc.- Not invested. looking to build positions at lower levels for the long term

Infosys for multiple years have been in pe range of 15-20 and even higher dividend yield.

Market is normalising it back as excessive run up 2021 is getting normalised.

where do we find what was the currency realization for last quarter? considering rupee depreciation, the topline and bottom-line look very subdued, the concall however wasnt very disapponting, the management didnt warn of any serious slowdown .

But I think @KrishnaA is right , the market is readjusting valuation

Infosys shares turned ex-dividend on May 31, 2023, meaning that investors who bought the stock on or after that date will not be eligible for the company’s upcoming dividend payment.

The IT giant has announced a dividend of ₹32 per share for the financial year 2022-23, which will be paid on July 15, 2023.

The Murthy family, which owns a significant stake in Infosys, is expected to receive around ₹1,100 crore ($140 million) from the dividend payout.