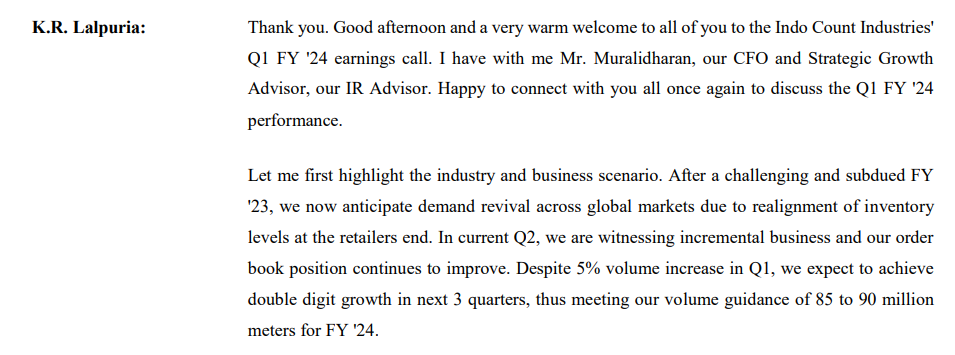

Indo count Q2FY24.

ICIL announced superb Q2 results with revenue growth of 22% to reach its highest ever revenue of 1033Cr and EBITDA growth of 58%. EBITDA margins at 18%(incl other income) for Q2.

Overall management commentary was bullish for the H2 with increasing volumes guidance…

Q2FY24:

Volume growth of 40% in Q2 to reach 28.7million meters.

Volume guidance of 90-100 million meters for the year (revised upwards from earlier 80-90mm).

EBITDA margins will be maintained at 16-18% for the year.

US retail customers restocking continued from Q1 and better traction is continuing.

FTA agreement existing+ongoing, China+1 strategy by global players driving growth.

Adding new customers, brands and new geographies.

+ve on domestic market demand: two brands , “Boutique living” for aspirational customers and ”Layers” for the middle class.

Target to take domestic revenue to 10% of topline in next few years from 2.5% in Fy23.

70% of current business is from US…Going ahead US will be 60% and rest will be 40%

Employee salary will be at 300 Cr for the full year.

Cotton prices in India have stabilized.

Commissioned new spinning and fashion bedding unit.

1100 cr investment in capacity during the last 2 years. current capacity utilization is 65% on yearly basis.

Further investment on value added products, fashion, utility and institutional bedding. ( last yr contribution was 19% and target to reach 30% of revenue).

Discl: Invested.