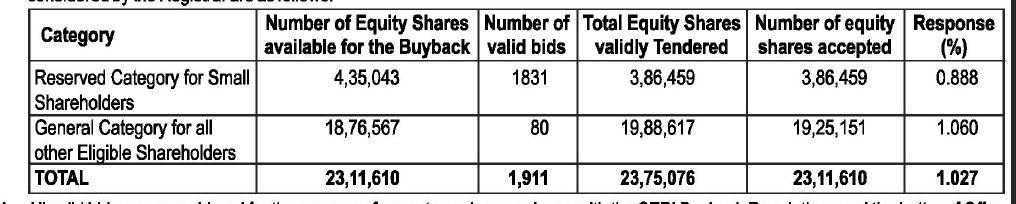

Retail quota shares offered were lesser than the reserved category!

Also, promoters have tendered meaningfully!

2 Likes

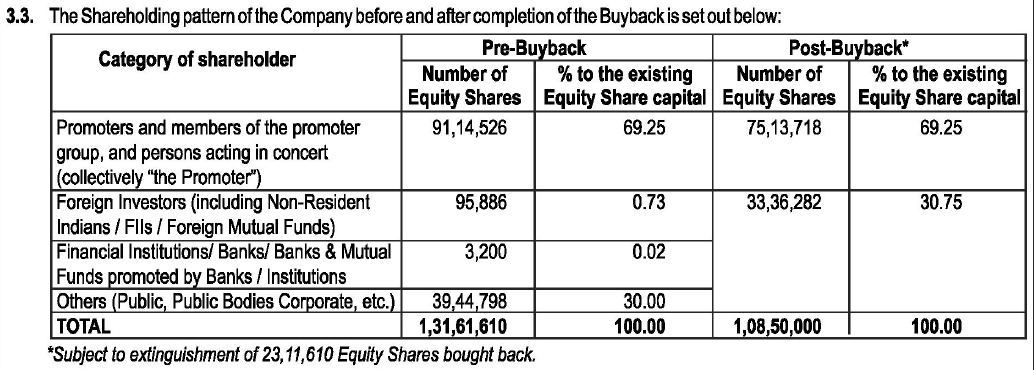

So nothing unusual with this buyback …

- Management and public shares got tendered in full, so

- Shareholding pattern has not changed

- Small retail investors participation was 88.8% also not many small retail investors tendered more than minimum entitlement.

- Unsubscribed portion of small retail got absorbed by other share holders.

Any particular reason for the recent run-up in this stock ? I have been holding this for a while. I would like to know whether it’s time to get out or there’s something more to it.

Only thing I can think of is that the valuation is reasonable and the recent result was not good owing to COVID-19 scenario and now expected to bounce back. There was low participation in buyback and not all shareholders offered shares despite being offered at much higher than then prevailing market price. This might have been viewed as positive by market participants.

Does anybody believe seriously about the recent duties introduced by GOI on Chinese imports will help this company ?

I had done some digging into this company as well the sector including finding information on its unlisted competitor as well information on the anti dumping duty order. Hopefully it could be useful for the members. If some of the information is already given above, then I apologize in advance.

INDIAN MARKET SIZE

The Indian after market toner segment (in which the company competes in) is around 7000-8000 tons/year as at FY18 inclusive of imports.

Assuming 80% capacity utilization of Indian Toner (as per ICICI Direct Note posted earlier) the Selling Rate per Kg in FY18 for Indian Toner would be Rs 390/kg derived as follows: 112 crores / (3600 tons*80%)

At this rate, the entire Indian market size would be Rs 275-315 crores in FY18. Something to this effect has also been noted in the ICICI Direct Note. Thus the entire toner after market segment is not very large.

MARKET PLAYERS

There are two major players in this segment - Indian Toners (capacity 3600 tons/year) and Pure Toners & Developers Pvt Ltd (capacity 2700 tons/year). Recently, in FY19 H2, a third player JIT Toners setup operation in Daman with a capacity of 600 tons/year.

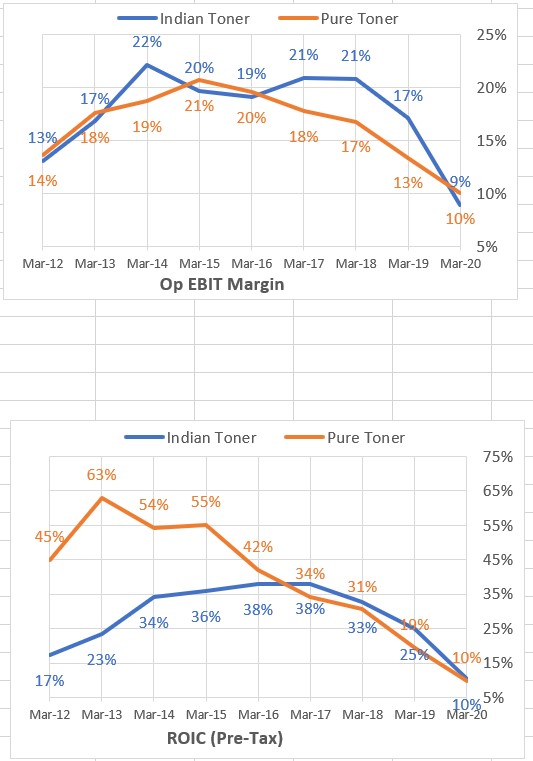

SALES, MARGINS, ROIC

If you notice the Sales profile for both companies match. Both grew steadily until Mar-17. Thereafter the sales were around the same level for two years until Mar-19 and thereafter both showed 20%-25% sales DROP in Mar-20. The reason for same level of sales from Mar-17 until Mar-19 and drop in Mar-20 is that imports from Asia steadily grew in these years and in FY20 these countries “dumped” toners in the Indian market as noted in the Anti-dumping Duty order. The import figures are given in the anti-dumping duty order (more on that later)

The margin and ROIC (other than FY20) have been good and the business has generated good amount of cash

Another thing to observe here that the unlisted competitor - Pure Toners is more aggressive than Indian Toners. It more than doubled its capacity from 1200 tons/year in Mar-13 to 2700 tons/year currently and also tripled its revenues from Rs 14 crores to around Rs 40 crores in the same period. While Indian Toners also increased capacity and revenues but it did not do so at this pace despite the fact that it was sitting on boat-loads of cash

Having said that, the margin and ROIC of Indian Toner is better than that of Pure Toner

It is pertinent to note that around half of raw material is imported. Exports, on the other hand, are only around 20% of sales. Also exports have been very slow for the company as noted in some past annual reports.

ANTI DUMPING DUTY ORDER

The Government issued a notification on 10.08.2020 imposing provisional anti-dumping duty on black toner in powder form for a period of 6 months, which was further extended to 5 years.

The duty is on imports of “Black Toner in powder form” and if it is originating in or exported from China, Malaysia, and Taiwan. The entire DGFT proceedings along with the final order can be downloaded from here.

The import data of the past few years as given in the Anti-Dumping duty order is tabulated below. It can be useful to understand how much the sales can change due to imposition of the duty

The duty imposed ranges from $1.167 - $1.568/per kg (i.e. around 87-117/kg at todays rates) for China and Malaysia. The duty for Taiwan is much lesser at $0.159/per kg

A write-up against the order and the difficulties to the importers can be viewed here. It will give some perspective as well from the other side as well.

In the words of the company as given in the AR:

“By this action of the Government of India, the imports of black toner became restrictive which helped your company to meet the tough competition from the Chinese Toner in a much

better way.”

OUTLOOK

At the outset, I would like to state that I have invested in this company and kindly take my views as biased.

Currently the margins and sales are at a low and are likely to improve due to the Anti Dumping Order and hence it looks like a good time to enter. A major deciding factor for the valuation is how the anti dumping duty will play out.

A not-so-rosy scenario could be that:

• The sales resume to Rs 115 crores & Op EBIT margin to around 20% (the level that the company was doing in FY17 just prior to the increasing imports) and thereafter it grows at 6% (which is its revenue CAGR of past 15 years) until FY26 (when the Anti-Dumping Order expires) and there is no “high growth” period after that.

• For the Terminal period, one can assume that WACC=ROC since the company is in a competitive environment. (As a side note: when WACC=ROC then growth does not matter as the extra earnings from growth are taken away by the reinvestments needed for the same thereby leaving the FCF at the same level)

Even with the aforesaid assumptions the valuation, assuming a discount rate of around 10% the valuation works out to Rs 100 crores for the operating assets + 97 crores cash = 197 crores i.e. around 180/share. Thus the current price at around 160/share means the market is pricing very low expectations on this stock, which is a good thing.

You will note that I have not considered exports as it my view that exports have not been very fruitful for the company in the recent past. The company also has stated its USA subsidiary (wholly owned) is not producing the results as expected. However my views maybe wrong on this

Obviously, there could be worse scenarios than the one described above such as importers find ingenious ways to get the product without the duty, Asian countries price their product more cheaper thereby negating the duty, promoters go back to their old ways or do a “diworsification”, the domestic competition heats up which causes margins to decline despite the anti dumping order, etc.

Also there can be more positive scenarios wherein the company (and also the other Indian manufacturers) grab a larger pie of the imports. As stated in the ICICI Note, 75% of the sales of Indian Toner are to bulk purchasers who are “probable importers”. If these people start buying from the domestic manufacturers instead of importing due to the price parity then the upside could be larger. Even the terminal value assumption of WACC=ROC can be challenged as the company did manage to earn above its WACC in virtually all years except FY20. The company has also increased its capacity to 4200 tons/year which would come into effect from June 2022 and even this factor has not been considered above.

Thus the valuation is more dependent on the outlook you take. A key thing to watch would be the revenues and margins in the coming 4-6 quarters. Just remember that this is not a “consistent compounder” story and the entry & exit prices do matter as you can even gauge from the comments posted in the thread.

A larger post is on my blog here which could be useful for people who do not know much on this company/industry

8 Likes

Excellent results

Just an update on my post written above more than 1.25 years ago.

The main question the current post tries to answer is whether anti-dumping duty (levied on imported toners) benefitted the company or not. IMHO, the answer is clearly yes:

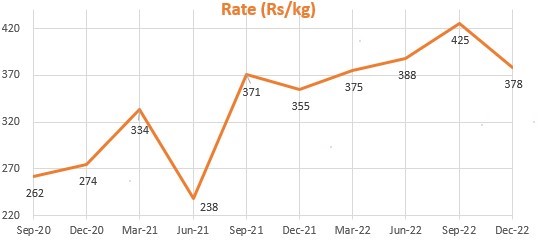

1) Import Data

The anti-dumping order is in effect from August 2020.

If you observe the chart (SOURCE: Screener.in), you will observe that the Import Rate has steadily increased from 300-350 levels to 450+ levels. Admittedly, import data is noisy and also does not give accurate rates unless the HSN code is EXACT. However the general trend, shown in the red line, is unmissable

2) Improved Rates & Margins

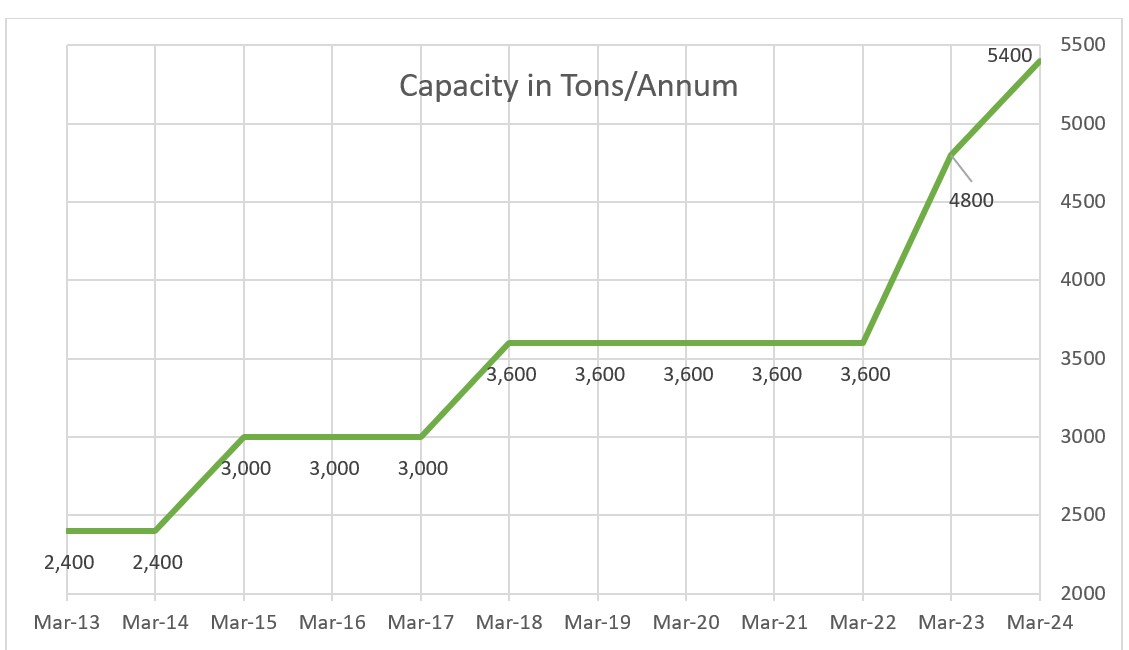

The company had a capacity of 3600 MT which has increased to 4200 MT from September 2022. (SOURCE: Minutes of AGM held in August 2022). Using this we can calculate the Rate.

Again we don’t have utilization levels and hence the rates will be biased lower, but even here the trend is clearly visible. The company was getting Rs 262/kg in Sep-20 quarter and is now getting Rs 375/kg

Secondly the EBITDA margins have improved from 14% in Mar-20 to around 20% now

3) Higher Capex planned

The company has increased its capacity from 3600 Tons/annum to 4800 Tons/annum in January 2023 and has further announced its intention to increase to 5400 Tons/annum.

See Milestone section of their website. This clearly shows the confidence of the management in its business.

The current market cap is Rs 210 crores (Rs 195/share) and the company has Rs 85 crores cash (as per September 2022 Balance Sheet). At this price the market is effectively saying that after the elapsing of the Anti-Dumping Order (in August 2025), the company will not grow anymore, will not earn more than 12% Op EBIT margin and also will not have ROC>COC. These assumptions are EXTREMELY pessimistic and not consistent with past.

Even if you think in terms of the relative valuation, it is priced low. The business is being priced at Rs 125 crores (Rs 210 crores market cap- Rs 85 crores cash). If we assume capacity of 5400 tons/annum (in FY24) with an average rate of Rs 380/kg, it leads to revenue of Rs 205 crores. The average Op EBIT margin of the past 17 years is 16% and thus, after tax, we see a Net Profit of around Rs 25 crores. This yields a PE multiple of only 5 (Rs 125 crores/25 crores). One way to justify the cheap valuation is to assume that the margins will go back down to the levels it reached during the ‘dumping’ years of FY20/21 even in the long term. However, this assumption seems pessimistic (to me) and inconsistent with past data.

My views maybe biased as I hold the stock. Furthermore, my views are (and SHOULD BE!) subject to change in price and information.

12 Likes

Today’s official announcement of Additional proposed capacity of 600 MT adding to existing capacity of 4800 MT, financed by internal accruals and increased demand.

Paper stocks are trending. Next ink ???

#indiantoners.

3 Likes