Malabar reduced stake : https://www.bseindia.com/xml-data/corpfiling/AttachLive/994A9EF8_B562_483E_A401_9F887E7C7924_083755.pdf

Poor FY21 results. Though optically there is revenue and profits growth, it is not actually the case. Revenue growth seems to be driven by pushing inventory to distributors and marking such inventory push as revenues. This can be triangulated by the fact that on an FY 21 Revenue of Rs 224 Cr, the outstanding receivables are Rs 226 Cr. Receivables > Revenue which is a clear indication of inventory shipment booked as revenue. Similarly profits at Rs 3.69 Cr is on account of Inventory adjustment and Deferred Tax amounting to Rs 41.42 Cr, else PAT would have been Rs -37.73 Cr (Loss). Poor results in my view. Stock’s going up as some operators are pushing it up, may be giving exit to some large investors. Otherwise expect Indian Terrain to trade around its 52W low

2 Likes

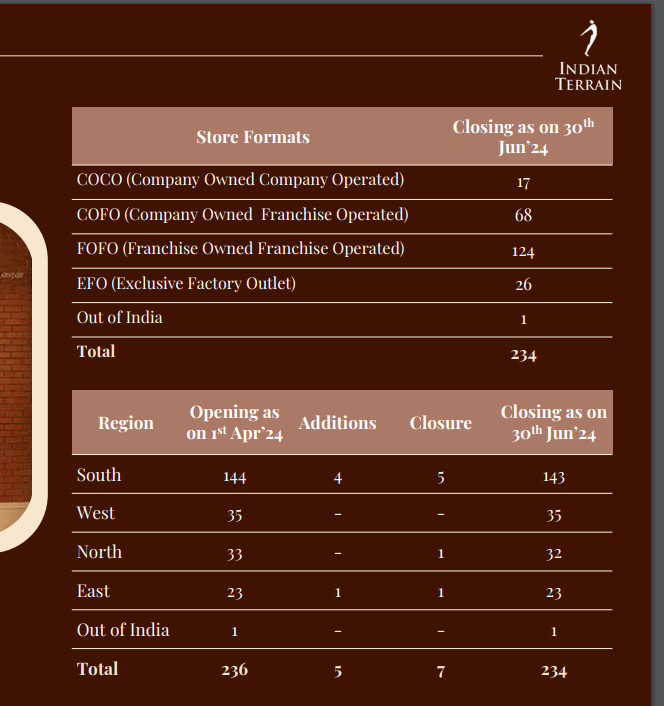

Indian terrain has increased it’s fixed assets ( buildings ) to expand their exclusive brand outlets (EBO). At present they have 227 EBOs and have a plan to increase this to 400 by FY 24.

They’ve also raised funds last year.

It’d be great if anyone can help me find the reason for such fundraise.

Also, they Celebrity Fashions Ltd have the same promotor group.

1 Like

100+ Cr revenue in Q3 FY22.

Revenues back on track. Not sure about the situation on the inventory and receivable side.

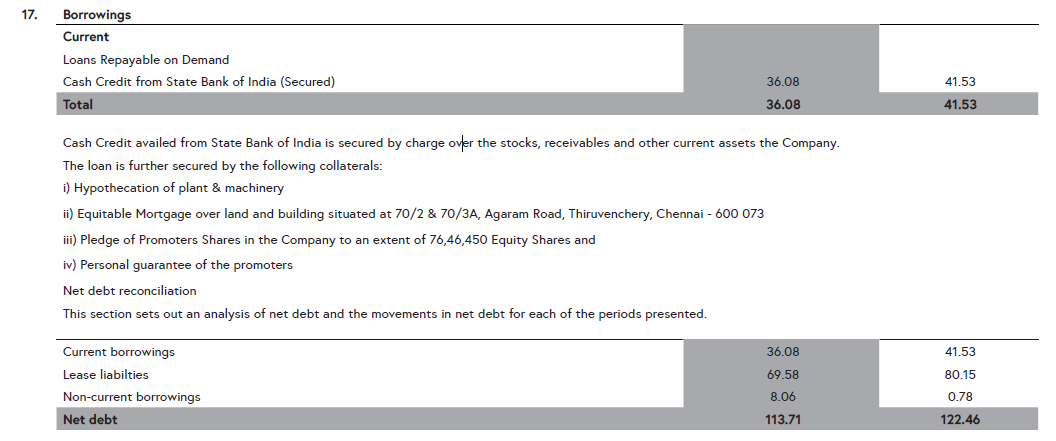

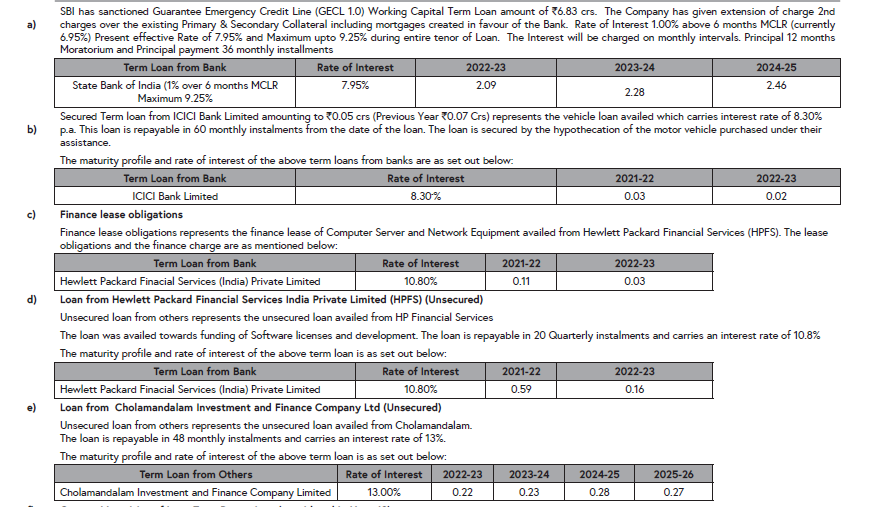

Debt seems to be their biggest issue. Huge interest outgo.

Need to look at the balance sheet to conclude anything here.

I am hoping that post-covid recovery should help them get back to normal business and help them pay-off the debt.

Disc- Invested. Not a recommendation.

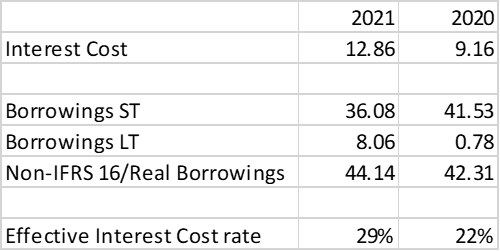

Does anybody have clarity on their Debt? The debt costs look too high.

Long-term rates are 8-13% (see below), which implies the ST loan is @ these exorbitant rates.

2 Likes

Hi

Can anyone help with links of Indian terrain’s AGM for last two years.

Is it available on youtube?

2 Likes

some positive developments

- Promoters pledge reduced

- Exited boys wear segment as it was not scalable and dragging on overall profitability. Management says this would help improving working capital and cash flows.

Q2-FY24 presentation:

1 Like

Hi. anyone tracking this company. Any update on the discontinuation of boys wear and impact on ops for the company?

1 Like

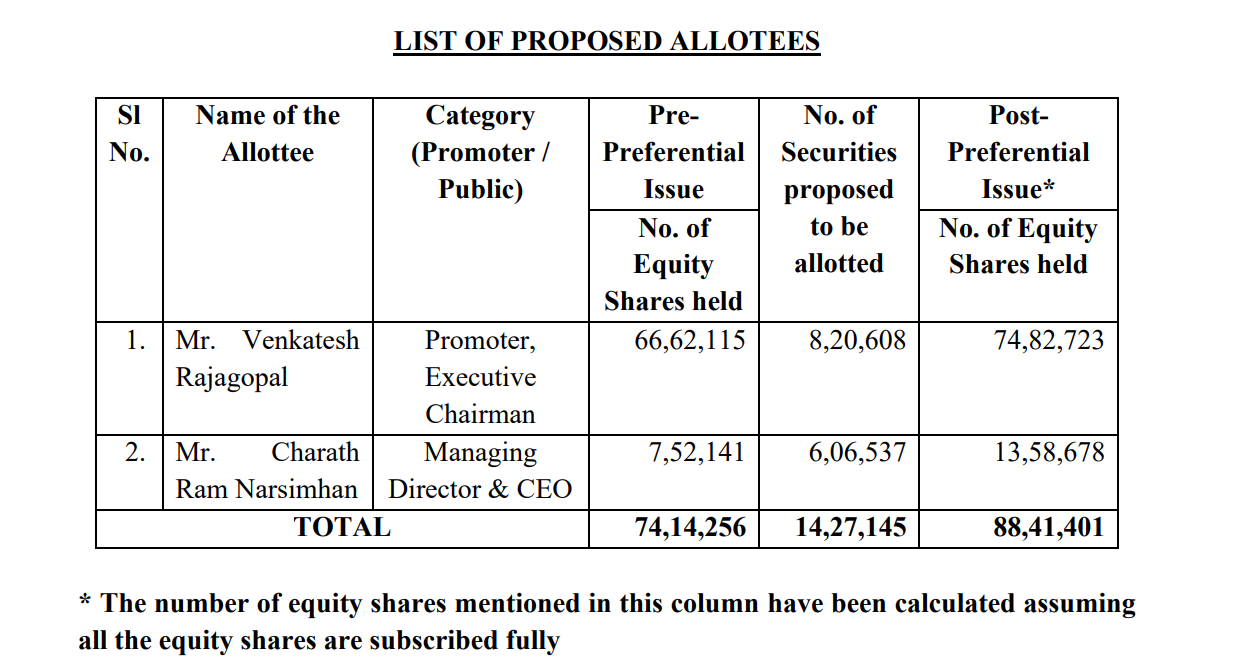

Promoter Venkatesh Rajagopal and MD Charath Ram inducing 10Cr to the company via preferential allotment.

The closure of kids segment has significantly impacted the topline and bottom line. Indian Terrain is a 20 year old brand present across 230+ EBO and 800+ MBO and is available at 260-270 Cr Mcap. Promoters do have 30+ years experience in garments.

Latest Inv presentation: https://www.bseindia.com/xml-data/corpfiling/AttachHis/e372ed28-1087-4728-8e10-5517277c3119.pdf

Disc: Invested. No transactions from last 6 months.

cc: @Sridharj

2 Likes