Am not able to reconcile why depreciation is stable in this qtr. Since they bought assets in Q4FY16, hence net fixed assets went up ~4x but still depreciation is flat. Would appreciate help from any CA who understands the asset treatment in our group. Or is it less than 180 days that’s why its stable, so from Sept qtr PATM will be even lower

The numbers are subdued for sure. Q1 however is not the strongest quarter for the company if we look at the last 8 quarters. EBITDA margins also a tad subdued. Overall numbers are not great. I think if they maintain last year EPS that would be great. Looks very tough though.

I think I would still urge the folks here to do the scuttlebutt by talking to franchisees, MBOs and big apparel stores like Lifestyle as it can seriously throw lot of insights about the company and the branded apparel space in general.

Tough is an understatement. There will be an additional finance burden of 2 crore this year (you can see 2.06 crore as finance cost compared to 1.50 crore) plus the tax burden. To offset the 30% tax rate, you need 42% higher sales with the same profitability at EBIDTA level. That translates into additional sales of 140 crore, out of which only 7 crore has been delivered this quarter. Means 133 crore of extra sales over the next three quarters - which is nigh impossible. Only with greatly improved sales + big improvement in margins can you expect the bottom line to be maintained.

Not happening, in my opinion. For long term investors it may be worthwhile to stay invested, but you are looking at an opportunity cost of at least 9-12 months. ITFL has finished its accumulated losses at the wrong time, going in for a prolonged decline in bottom line at a time when corporate earnings are generally turning around for other sectors. Opportunity cost, any one?

3 Likes

Agree with you. Don’t think there will be any improvement in the bottom-line. At best we can expect something in -5% to -12% range on the net profit as compared to last year. In terms of the brand recall and brand presence, Indian Terrain is pretty strong (I did a scuttlebutt 1.5 years ago and also 6 months ago). Personally, I am a fan of their clothing as well. In terms of price, don’t think we will have big movement for next 6-9 months (unless numbers really start to pick up and anticipation builds in). However, the recent market is pulling anything and everything towards the sky and we never know how market views the price.

Disc: Invested

1 Like

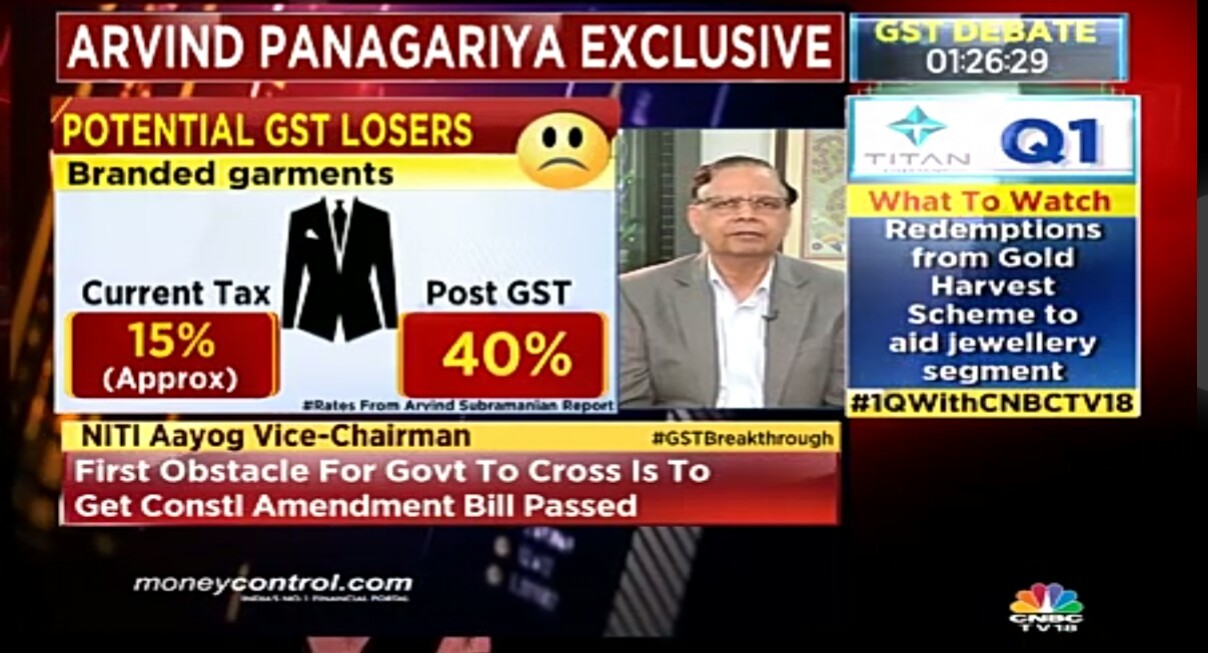

If GST rate for branded garments comes at 40% vs current tax of 15%, wouldn’t it be huge -ve for the sector itself? I’m not able to find any brokerage reports/ articles for details-- any views?

as a consumer im pretty annoyed for such high tax rate for apparels ![]()

Disc: Not invested.

Had been to Globus store at Rajkot for shopping. Saw good collection of Indian terrain brand. Had even inquired store manager as to which one is their best selling men’s brand. The answer was Indian terrain. Was pleased to hear that. Brand recall of Indian terrain seems very good. I wish they manage their balance sheet issues well, like debtors days, working capital cycle etc. If that is taken care of, I think this script can get much higher multiple. Also pledge shares now should be removed as land recently purchased can be mortgaged and should be sufficient for loan purpose.

Disc - Invested

2 Likes

Hi,

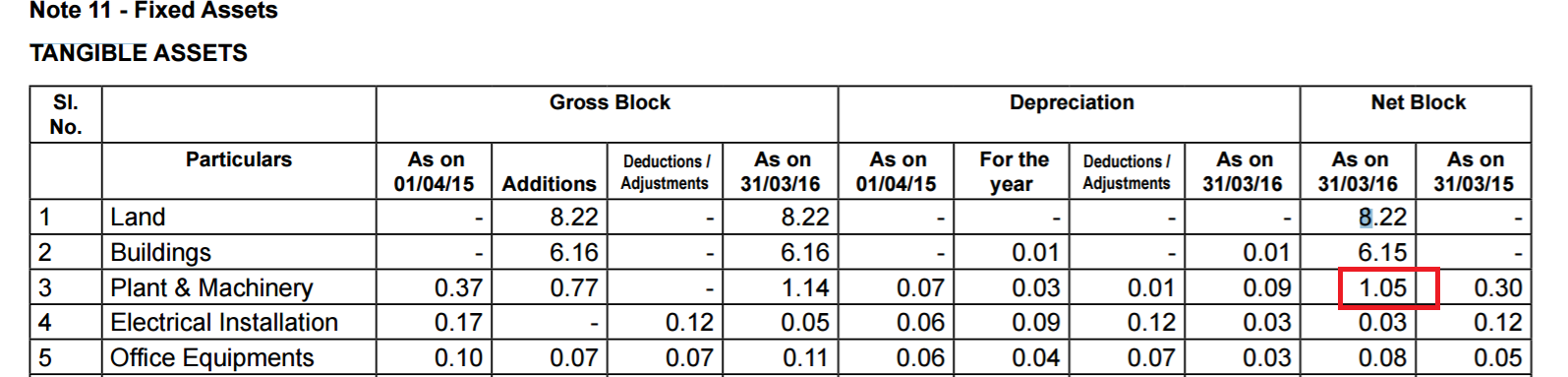

Can some clarify why “plant and machinary” of ITFL is so less for a company with sales of 300+ crores ? Does it outsource manufacturing to others ?

Regards,

Kiran

ITFL sources their goods through Celebrity Fashions Limited (also a listed entity). They are owned by the same promoter and ITFL was demerged from Celebrity Fashions a few years ago. Therefore, the model is asset-light.

1 Like

Sequential fall in profit margins from 12% to 6% in the last 4 qtrs. I would be wary of investing in Indian Terrain.

Indian Terrain has very little in-house production. Thus they have one of the highest fixed assets turnover ratio in the industry.

Thanks guys for the clarification

Guys, is it correct to assume that the Indian Terrain Fashions merely holds the brand and has no real physical assets? Does not manufacture, does not own most of the stores. Looking for an answer to this. Tracking ITFL and considering some investments

That would be a fair statement. It owns the brand and outsources manufacturing. Most of its stores are franchise owned

Forgot to post here- few days back FLFL announced that it is selling its stake in Lee Cooper brand. At a valuation of INR 1000 Crores. Sales are 250 Crores and EBITDA of 40 Crores.

Indian Terrain in comparison has sales of 325 Crores and market cap of ~600 Crores.

1 Like

The reason Lee Cooper got premium valuation might be because they get premium placement (most visible and more shelf space ) in all future group store, thus they are less dependent on third party sellers and also they can plan production better because of this fixed space.

This is same reason almost all brands (Raymond, Aditya Birla Group brands) are pushing for EBO instead of traditional MBO channel.

Better control over inventory and prime shelf space are essential

The improvement in top line is very encouraging and I believe 30% growth in apparel industry is no mean feat (from 95 crores to 125 crores Y-o-Y).

What still remains a big worry is the following:

-

Other expenses have jumped from 20 crore to 42 crore - this is a jump of 22 crores for a top line increase of 29 crores. Usually, “other expenses” is marketing and advertising spend for such companies. This implies that it required approximately 10 crores to drive 13 crores of sales. Of course, if you look at net profit per unit sold vis-a-vis the marketing/ad spend per unit sold, the cost of customer acquisition is clearly astronomical. One counter to this may be that customer satisfaction of ITFL products is usually quite high (can say from personal experience), so customer stickiness may be something that we are not accounting for.

-

Trade receivables have again jumped from 117 crores to 132 crores on a half yearly basis. Tentatively, this means 15 crores out of 37 crores (that is, 40.5%) of sales have not been received in cash by the Company.

Unfortunately, I am not experienced enough in analyzing how much time companies of such scale, size and industry generally take to start generating free cash flow. It is entirely likely these are the efforts that have to be made to build a brand and reach critical mass. Comments are welcome.

2 Likes

Indian Terrain has launched boy’s wear, denim and footwear over the last few months. I suspect the increase in the expenses could be related to that.

I suspect they have also opened some COCO seeing the jump in fixed assets.

Overall the results were ok. Tax is a dampner however, over-all increase in sales is a good sign. I think ITFL reported the highest growth in the branded apparel category with 30% YoY growth. Madura, Raymond, Arvind, KKCL all reported sub ~ 20% growth.

Working capital continues to be the key monitorable.

Given markedly lower margins, I suspect they pushed a bunch of inventory online at deep discounts. This helps show a top line growth but clearly doesn’t help margins. Also a sign that the brand doesn’t have ‘pull’ and is being pushed through channels by discounts. Need to monitor if inventory is being liquidated at lower prices.