Diwali shopping normally happens for customers 15-20 days ahead of Diwali and stock gets purchased by franchisee nearly a month ago, last year Diwali was at around 20-22 October, so sales of Diwali season was fully booked in sales figures of Indian terrain or for that matter all garments company in Q2 only, this year Diwali was on November 11th, so much of Diwali season sales would have been booked in October month. Only Q3 figures would tell actual figures. Fingers crossed…

1 Like

Oh yes, definitely. That was just on a lighter note. Maybe I shud have qualified my statement in terms of doesn’t matter on sales booking front.

I have been invested (9% of my PF) in ITFL since Feb’2015 and expect better things ahead

Although I am not sure of what to make of the related party transaction, but none the less I expect better things business performance wise.

1 Like

What I meant was exactly what dhawaldoshi said.

2 Likes

Can some one tell me why kewal kiran is getting such high valuation and indian terrain is getting lower valuation in terms of pe and ev/ebita. Both the companies are having simillar roe and debt to equity.

KKCL is getting higher valuation because of higher ROCE, better working capital cycle, higher EBIDTA and higher PAT ratio. Still the difference in my opinion is very large and will shrink soon. Or to say after split, difference has already started shrinking. Indian terrain gave very good move in last 2 days, up from 140 to 160, that effectively up 800 from 700 considering pre-split levels. Also it made all time high today and volumes too were decent. Also delivery volumes were good yesterday. Much more upside in store. Keep riding. Enjoy the ride.

Dislcosure - Invested at 600 levels and roughly 10% of my portfolio.

Movement due to split is sustainable?

Movement due to split, theoretically should not be sustainable. But in practice, it may sustain due to following reasons.

- Volumes were very low in this script as mostly it is cornered stock and has very low free float. So till now, many were not entering this counter due to lack of liquidity. After split liquidity would increase and thus this counter would attract those investors.

- As mentioned in earlier post, difference between KKCL and ITFL valuations should shrink gradually and thus movement may sustain.

- Per share profitability, in my view, would increase due to lower interest cost due to long term debt repayment, interest income from excess QIP funds and margin expansion. My view is EPS of 40+. This would take price somewhere near 900 conservatively.

Fingers crossed.

Decent results by Indian terrain

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/2596F4DC_BE26_447F_A84C_D0426BE1A9C3_150049.pdf

But they could be even better as festive fell in Q3.

Edelweiss report on Indian Terrain :

Indian Terrain Fashions Ltd - Betting on the brand

3 Likes

Good information and discussion provided here. I have a question regarding their pledged shares it is about 60% of promoters holding. As it was inherited from celebrity fashion but going forward what are their plan to unpledged the same shares? as if you see ITFL is almost debt free and celebrity has also reduced their debt but their pledged has not came down and even it is not at very high levels. As it is a very high levels of pledged its really a big concern as per my opinion.

Thanks

Prashant.

These brokerage analysts really know how to stretch out a report…36 pages for what could have been done in 10.

Am looking at screener data for tax payments and bse data for share holding pattern. Any idea why company is not paying tax even when net profit on the books have been growing steadily ? No tax payments, low promoter holding of approx 30% and out of which 69% is pledged. @varadharajanr, @mmvravindra aren’t all these negative signs for a small cap ?

1 Like

They have accumulated losses pertaining to Celebrity fashions from where they are demerged some 5-6 years back. So they are not required to pay tax till that accumulated losses figure get exhausted. Also they are subject to MAT and I think they are paying MAT regularly, which is reflected in profit and loss account and also Cash flow statement.

3 Likes

Q4 results are out: ITFL Q4 results

Revenue at 97 crore vs 69 crore

Net profit at 6.82 crore vs 4 crore

Overall, yearly revenue at 325 crore vs 290 crore and net profit at 33 crore vs 17.50 crore.

What beats me is how ITFL manages to stay afloat with more than 35% of its yearly revenues locked up in receivables. The receivables have increased on an yearly basis from 95 odd crores to 117 crore. How is it possible that the company is not receiving so much of its sales in cash? Is it ever receiving this cash, because receivables have never gone down.

Hi Guys,

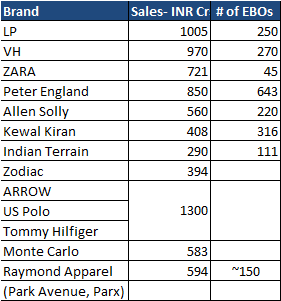

I am analyzing the overall apparel space and wanted to share a few learnings that I have had. We can use this in the context of Indian Terrain and perhaps other companies as well.

But before sharing some key data on some apparel brands in India. Most of them are listed and thus data was easy to get.

Overall the space is hyper competitive and in general difficult to scale. Even an old brand like VH or LP is still only 1000 Crores in sales. Compare that to Zara which is maybe 5 years old is already a 700 Crore brand!!! It must be doing something right. It would be really interesting to see what they are doing right. Can others replicate it?

Overall industry observations

-

Margins in the MBO channel are much higher. However this channel is tough to scale up and is slowly losing its sheen

-

Players who focus more on EBO led expansion earn margins around 12-14% . This is fixed capital light however, working capital is the key here (Inventory + Debtors - Creditors). Madura scores very highly here. It’s working capital is close to 80 days. Kewal Kiran is also extremely efficient here.

2 Likes

Tushaar, agree on this point. However growth in the margins has been very heartening. If this is sustainable then it would be fantastic. On balance sheet- I think the management is trying to work on this aspect and has said that they would like to get it down to ~ 100 days at a net level. Currently it is at 139 days.

debtors increased to 132 days but the silver lining is that the they increased their payables as well. So at an Net level the WC days has actually come down from 152 days in FY15 to 139 days in FY16.

The key to serious re-rating would be sustained margins and improvement in balance sheet from here. I think as they open more stores, they would be able to do so on better terms. A leaner balance sheet will also help them.

Overall, these results have been more positive than negative in my view.

Disclosure: Hold Indian Terrain and maybe positively biased.

1 Like

The receivables aspect is something I wrote a detailed email on to the CFO and Investor Relations Officer Mr Manikandan last year. I also sent him a hard copy of my letter but obtained no response. I wonder if this constitutes an “investor complaint” and whether the company was obligated to respond to it.

In any case, I am also pretty highly invested in ITFL because I just see the brand working on the ground. The receivables aspect has always foxed me though - what if the receivables were to turn bad? They never seem to though, because the annual report barely reports any bad debts.

If they are able to sort out these balance sheet issues (and get rid of the pledged shares already, for god’s sake) then ITFL deserves to trade at a PE in the mid 20s seeing other listed peers.

On that note rohit, where did you get information that Zara is listed in India? As far as I know (and I know this from pretty much the person who has rights to distribute in India), Zara has a distributor in India who buys the goods off the foreign entity and sells it at a markup and remits a royalty. Also, given how long these foreign brands have been in existence, it is difficult to compare with ITFL right now. However, I would say you may be right that this may not be a billion dollar business. On that note, though, I believe ITFL is far more profitable than most other branded apparel plays out there. The net profit margin of 10% is fantastic and if maintained, augurs well for shareholders in the future.

I maintain some interest in unlisted companies, so I was researching on Numero Uno, which had filed a DRHP for IPO in May 2015. That also is an interesting play, but not much of a differentiator from other low to mid range denim/lifestyle brands. The margins were also lesser than ITFL, though the huge equity capital basically makes the comparison even more unattractive. I hear ITFL is moving into the children wear space, which I believe can only be good for margins. Children’s clothes are always sold at a premium and need regular replacement. If someone could shed some light on the competition in this space in India, that would be insightful. Unfortunately my knowledge of the apparel market does not extend that far.

I read an article on success of Zara in India and their USP is getting international fashion in India before anyone else. Zara has the biggest team of designers who copy international fashion and Zara launches their fresh line of clothing within a week of the fashion show. This allows them to charge higher margins and attract customers who want to stay in line with the latest fashion. But their play is not on masses where these other brands come in.

I remember LP being a more premium brand 5-7 years back but now it is reaching out to the masses while the likes of Zodiac Allen Solly and VH has tried to move higher on the price range.

- My personal observation based on my consumption over the years.

Hi Tushaar, The point of comparison was to just get a sense on what makes some company tick. The mortality rate in this sector is fairly high. Thus the comparison. On the margins front, I have been very positively surprised. I was expecting such margins maybe 2 years out. But a major positive surprise.

On the management not getting back, well its the same sad story with most of these companies. I won’t read too much into that.

On Balance sheet- Management has mentioned that they are installing ERP (should have done much earlier though) it may help them reduce the receivables.

Also, while I am not sure on this, but maybe because of the last quarter being very strong, maybe the receivables number looks more bad than it should- this is just my guess. I maybe wrong here.

Tata Trent has invested in Zara in India. It owns ~ 49% stake in Inditex India. So you can get numbers on them.