Found an article on Microfinance Review.

M-cril is independent Mircofinance reviewer. The last report is of 2014. Dont know why the reports for 2015 and 2016 are not there.

Key sectoral Risks of Microfinance Industries, their characteristics and the possible mitigation steps taken by Janalakshmi (Taken from Janalakshmi AR 2015)

This is really generic. Nothing different from others. Please read today’s Mint on the risks , these MFIs are running by this explosive growth. Only Ujjivan is the most conservative

They may be generic but often ignored/forgotten by investor which results capital Loss . Can you put some rationale why Ujjivan is the most conservative?

As you can see, there are 3 drivers of AUM growth - ticket size, borrower base and duration.

From Q4FY16 conference call transcript of SKS:

For FY16, 84% AUM growth can be dissected into three parts. Increase in ticket size is hardly 22%, but the borrower base did go up by 27% and duration enhancement of 18% also helped. While we talk about the 22% growth in the ticket size for FY16, you need to superimpose that on the ticket size growth of hardly 4% and 6% during FY14 and FY15 respectively.

@amitayu I saw a figure where it mentioned Ujjivan growth in Loan is 25% that is one of the most conservative @Rajesh_R- the worrying part is increase in borrower base and duration both in case of unsecured loan.

Currently ‘party is going on and so we need to dance’…No offence to anyone. This quote has been changed a bit but made by former Citi bank CEO Chuck Prince before the sub-prime crisis.

I read the article in Mint, but had a question. Should’nt Ujjivan’s loan portfolio (AUM) growth be 52% during the year, while the article mentions it as 25% . The investor presentation suggests that that their MF loans increased from 3000 crs to 4600 crores during the year.

yes correct pranav. Actualy Ujjivan’s micro finance business AUM growth is 60% yoy + and individual loan AUM groth is 102% yoy in FY2016. Same was told in conference call by management.

Satin would be raising capital ($25 mn = 170 cr) soon.

So for FY17 calculations, add 170cr to Net-worth as well as to Mkt Cap (let us say the money is raised at cmp itself).

Let’s say PAT for FY17 is 100cr (management’s guidance, let’s say it is achieved). Add this to Networth (assuming dividend is zero).

So new MktCap at cmp = 18.63 bn Rs. (so P/E at cmp will be 18.63 after FY17)

FY17E networth = 5.94 bn Rs. (P/BV at cmp after FY17 will be 18.63/5.94 = 3.13)

I am not sure you should look at mgmt commentary/press article alone to establish who is conservative. Suggest look at loan ticket sizes, maturity of disbursement (how much is first cycle), like to like growth in first cycle disbursement before concluding which MFI is more conservative. Taking mgmt alone on their word may not be the best analysis.

Vicky it would be interesting to extend this analysis further to FY18. Because the BV growth for Satin and SKS will be significantly higher than bank licensee holding MFI’s… The valuation will be very appetizing on FY18 BV (my estimates are ~Rs 210/share FY18 BV for Satin implying <2.5 (P/FY18 BV) and 180 for SKS implying ~4x P/BV). I believe I have been conservative on capital raise valueation. And These are certainly not high considering their expected growth (>30%) and ROE (>20%) exiting FY18.

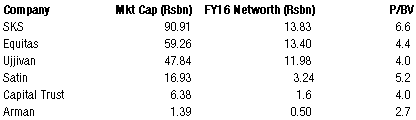

Financial Particulars on MFIs of Ujjivan,Satin,Equitas and SKS. I Feels , though OPEX cost for SFBs will be increased during transition in bank but Political Interference risk (biggest risk for MFIs) will not be there as they are regulated by RBI, this is a good advantage over MFIs.

SFB will also get acsess to cheaper funds in the form of deposits /ca, thus brining down the cost of capital to a certain extent.they also get to sell products like insurance to their customers.

Still I am skeptical on the loan growth and subsequent recovery. 2 consecutive years of Drought and Govt’s reduced hike in MSP in major staple products, + widespread rural distress + muted Industrial growth ( track the loan given for Corporate Credit), made me skeptical

Sugar sector is just coming out of the widespread distress.

I will be very happy, if proved otherwise as already invested