Thanks Yogesh excellent post for someone who does not ve understanding of valuation of nbfc . I believe some of these kpi r strongly correlated n some not.also, I understand how much weightage to be given to each kpi must b art than science . Possible to come up with a valuation kpi attractiveness ranking of companies ? Will it even make sense or it should be left to the art side of valuation with qualititative analysis of each of these companies , what’s your view ? Disc: invested in bfsi stocks as basket approach

KPI depends on the industry and current issues facing the industry. DuPont Analysis (ROE = Leverage * Profit Margin * Asset Turnover) is a good starting point for any industry.

I use peer analysis to decide discount rate and growth to be used in my DCF valuation.

Updates to the earlier peer analysis post -

Added Equitas, Manappuram and Muthoot based on the requests from some members. Added relevant analysis. Added Tax Costs so that all costs % + net profit margin % should add up to 100. Added value labels for 2016 series.

General notes on the charts - Charts with shades of green - higher the better. Charts with shades of red - lower the better. Blue - KPI specific for the industry.

Requesting all interested members to cross check these numbers with your own analysis and point out if these are any major deviations. Small variance is expected.

3 Likes

Where is the updated analysis…please share link

I have updated my earlier post so you can refer to the same post for updated charts and analysis. There is not much change in the analysis as Equitas is just about average and gold loan companies are also about the industry average.

Moreover, purpose of this post was to present the data so members here can express their own opinions for the benefit of others.

Did anyone here attend Equitas conference call yesterday evening around impact of demonetization? If yes, could you please put in a brief summary for people like me who could not attend the conference call due to timezone issues?

Before few days group was over optimistic about microfinance and any valuation was looking reasonable…now what’s fresh thought on valuation after correction?

1 Like

Overall microfinance view is short term pain, long term gain… having said that in the near term its more about:

- how long demonetisation mess carries itself… answer to this would be well covered by newspapers

- next quarter results… which would show pain experienced… though market may write it off as one time

Story beyond this quarter is extremely good as many moneylanders would either be wiped out or would have less new money to lend in future add to it interest rate reduction which would happen at faster pace now (but market would want to see how deep the demonetisaiton stains are first)

2 Likes

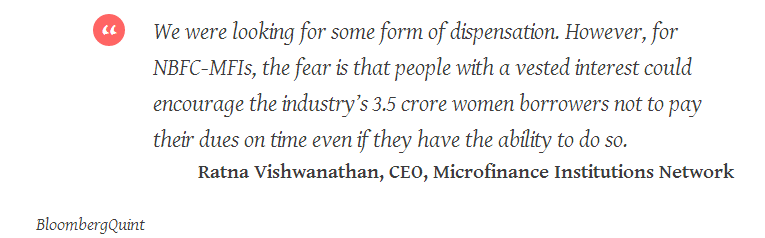

Anyone predicting a mass default by MFi customers citing lack of cash currency? something similar happened during the AP fiasco where borrowers were encouraged by vested interests to default en masse because MFIs were engaging in predatory practices. They did and pushed MFIs on the brink of extinction.

The reason mass default works (from a borrowers point of view) is because the loan is unsecured and cost of collection in case of a mass default is higher than the principal itself because the ticket size is small so borrower expects lender to just give up on collecting. The only way a borrower can get hit is a default will make him/her ineligible for refinance. Even here, a mass default will leave the industry with no customers (or substantially reduced customer base) so they will have no option but to ignore the default and continue to lend albeit after a cool off period.

Bajaj Finance collects post dated checks so there is less chance of a mass default and profile of customer is also better than that of MFI. Gold loan companies have a good collateral so a default is less likely here.

RBI offered an additional 60-days to certain categories of borrowers to make good on their dues.

http://www.bloombergquint.com/business/2016/11/21/rbi-provides-repayment-relief-to-small-borrowers

This is essentially a debt relief (even it is for 60 days it is still a relief). Such move could trigger a mass default and is a sign of distress for the industry. Similr relief was offered by AP government that backfired for the industry. even industry is now worried about it now.

3 Likes

Do you think demonetization has impacted the income of MFI borrowers?

This certainly seems like a risk. But my view is, situation is different from the previous occasion this time because of two reasons

1-The RBI notification explicitly calls out that the relaxation is for all type of personal and business loans below 1 crore. MFI is a sub set on which this rule would apply. This is an important call out because unlike in the past when the relaxation was only provided to MFIs this time the relaxation covers wider spectrum of loans. My understanding is borrowers would hear from other type of loan borrowers that ultimately they have to pay back and delaying the repayment would only increase the burden on them.

2- The MFI industry and RBI have the AP fiasco behind them. They have learned few lessons from the past and I am assuming that they would be very vigilant in ensuring that money is collected at the earliest. There have been no involvement of political parties so far (does not mean that there would not be in the future) and there are not any news about distress causing impact only to the borrowers of MFI. The distress is wide spread but it has not reached to a state where it had in the case of AP fiasco. MFIs have learned to have the human element while recovering loans.

I have limited knowledge of what actually has changed from RBI perspective since AP fiasco. But the situation on the ground seems different this time. I am invested in MFIs and I may have ownership bias.

2 Likes

@subashnayak_19_ and @v4value

In past you did lot of positive inputs on MFI…now with change in scenario…please share your thoughts about valuation and future prospects

Please listen to Ujjivan’s Concall yesterday. Mr. Ghosh said time is tough but things are picking up. It was arranged only with focus on current issue and MFI.

Wondering given the UP situation as mentioned in Ujjivan’s concall yesterday, why Satin management is coming out and talking to shareholders till date

I have a different way of looking at this issue. I have been tracking normal market activities on the streets of delhi. There was a sharp drop in business after demonetization. Things are improving rapidly off late. ATM queue length have reduced to 10-15min waiting time off late, Can see multiple ATMs dispensing cash now, businessman seeing rebound in their business. The waiting time in one afghan resturant near Central market which only takes cash was 10-15mins on Sunday. Many feel things will be as before in 2017. So there is a temporary cash crunch and business slowdown.

This will effect the borrowers of MFIs in 2 way, 1. Cash crunch, 2. Business volume dip. Both of these are short term one-time thing. The ever-resilient Indian economy will back to normalcy in 1-2 quarter. The customers to whom MFI lends will see their business back to normal way way earlier.

My original thesis for investing MFIs hasn’t dented at all. The unbanked poor will never ever wish to take loan from money shark paying 30-100% rate. MFI lending him at 20-24% seems way better arrangement even today. MFIN tracking will make sure that they will never default and get barred from the system from further borrowing.

So the move to bring them to banking is still on, and will continue in near future. NaMo has done many steps for betterment of poors in the correct way (like Adhaar, janDhan, DBT, Insurance, Mudra etc) and will continue to do so. Grapevine is filled with rumours of NaMo planning to distribute a part of the demonetization windfall to poor and middle class, and bunch of govt babus are working full time on it. If that will happen, guess the effect on MFIs.

To conclude, I feel demonetization is a short term pain for India and MFIs, with solid long term gain. One need to think beyond what is being written/shown in media/social-media, think contrarian to see the opportunity that is plain lying in front us, and make most of it. I feel it is an awesome opportunity for accumulation of stocks for superb long term return (I have no doubt 90% of us wont remember demonetization after 2-3years).

20 Likes

As per this article, NBFC/ MFI’s loss is Bank’s gain and they only stand to lose going forward.

The concerns raised by this article are valid but it seems to assume that the chaos will last forever. Highly alarmist article. Its just been 14 days people!!

Just having higher deposits does not mean that the banks will be able to lend to all kinds of borrowers or steal customers away from NBFCs. If that was the case the entire NBFC sector in India would never have existed. Everyone would have simply borrowed from SBI. MFIs have a deep and broad moat in terms of brand recall, reach & relationship with customers. Somethings which traditional banks have failed to achieve.

On the contrary I believe the banks, who find themselves flush with funds, will be under pressure to generate returns on these deposits. Hence they will lend to NBFCs & MFIs with good credit risk assessment systems.

3 Likes

Yes @fabregas I also think the same. Banks will need to find the borrowers and will need to increase the loan book subsequently, otherwise it will need to only give interest on funds in Savings accounts which they have collected.

This will also hammer the CASA ratio of the banks and we may see tepid growth for next few quarters

One good thing for MFI sector will be relatively low Cost of Funds.

Disc:These are my views. I am not expert on banking and finance.

MFI industry is like a roaring fast moving sports car that suddenly ran out of petrol. Can only go downhill without power until some rescue arrives. Will take time to get back on track and that time is likely to be much longer than what it appears to be. Market is pricing that now.

1 Like

@hnk_so I think we are in early stages of business re-adjustment. No one knows the duration and complete depth of adjustments required. My simplistic thesis remains beyond the next 3 months would I want to own this business? Money lenders gone, cleaner collection system, economics improving at bottomof chain, interest rates going down are all yes. Need from an end user point of view is still there - last mile distribuitiuon on collection. So medium term should make one more bullish. Now the key qn is can these businesses survive to see the medium term - ie, give these are levered unsecured lenders - one big hit can kill them. That qn, after demonitisation, I dont have an answer for. Only time will tell. Demon was an out of filed black swan, given teh mood of the govt there can be more such positive or negative events. You can drown in a river even if one spot has more depth than your height. I hope we dont reach such a spot for MFI’s but we are in unforecatable tewrritory now…

6 Likes