SIDBI in a collaboration with Equifax (one of the credit bureaus) has released these Microfinance Pulse Reports on the industry. It has good industry level data and should be helpful in answering the questions of borrower/geographic concentration, borrower over indebtedness, default rates etc.

The most recent issue has a good overview of the state of West Bengal as well.

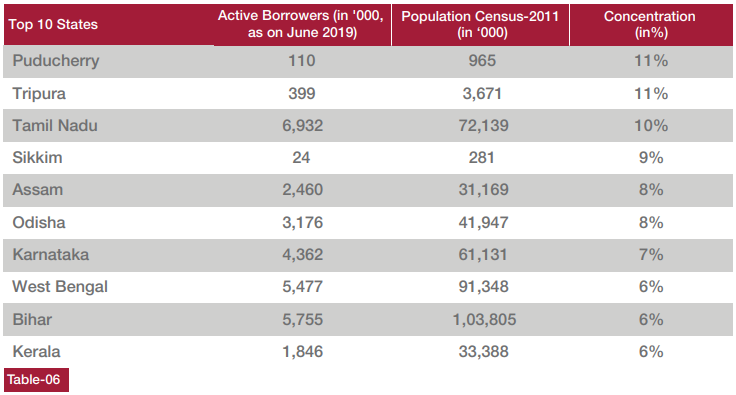

PS: On page 19 of the 1st report is this table,

I believe these concentration figures are misleading, we should be comparing the number of active borrowers by the no. of households (HH) instead of the population.

As we know that the industry primarily lends to women, so each HH should ideally account for one loan account. The report is not clear whether these are unique borrowers or not. In case they are not unique the concentration figures will come down.

Assuming on average each HH is comprised of 4.8-4.9 people. This is the factor by which the concentration figures will increase by.

It is the same case as with life insurance policies, most HHs just need one. In my previous post of TAM, I had estimated that India has around 28 cr or 280 mn HH. Outstanding LI policies are around 300 mn. Not all of these HHs have the surplus to insure themselves. (not my idea, taken from a renowned investor’s/fund manager’s interview whose name I cannot recollect).

So the concentration figure by HH could be 5x what is reflected in the table. However, this is not the complete picture. Just the borrower per HH figure does not reflect that each HH is having their credit needs met. A HH could be in need of 1 lac total credit to uplift from poverty through business ventures, health crisis, education etc. and the borrower counted could only be availing a portion of that amount.

We would have to go into more granular data to ascertain the penetration in this industry.