Could you summarize the article/paper (20+ pages paper without any conclusion/ summary in the end) for the benefit of everyone here, please?

The issue being highlighted for not able to get through market coupling is software intricities. The article published by CERC for staff gives details that multiple geography, multiple producers and multiple users can be added at different time.

1 Like

IEX Achieves Record Growth in Power Market: 24% YoY Increase in September 2024 Volume

- Total Volume Growth: IEX achieved a total monthly volume of 11,370 MU in September 2024, marking a 24% year-on-year (YoY) increase.

- Real-Time Market (RTM) Record: Highest-ever monthly volume in RTM at 3,913 MU, an increase of 34% YoY.

- Day-Ahead Market (DAM) Price: DAM price for September 2024 was ₹4.18/unit, lower by 33% YoY.

- Green Market Surge: Green Market volume grew by 214% YoY, achieving 723 MU in September 2024.

- Energy Market Trends: Total electricity volume (including green electricity) reached 10,332 MU, increasing 21% YoY.

- Renewable Energy Certificates (REC): 1,031 MU RECs traded, a 100% YoY increase, at a low price of ₹110/REC.

- Energy Consumption: National energy consumption reached 141.3 billion units (BUs), remaining flat YoY, driven by increased hydro and wind generation.

- Market Prices Decline: RTM price in September 2024 dropped to ₹3.98/unit, a 28% YoY decline.

- Day-Ahead Market (DAM) Growth: DAM volume increased by 33% YoY, reaching 4,610 MU.

- Term-Ahead Market (TAM) Decline: TAM volume saw a 43% YoY decline, trading 1,086 MU in September 2024.

- Green Day-Ahead Market (G-DAM): Volume surged 408% YoY, reaching 712.5 MU in September 2024.

- Green Term-Ahead Market (G-TAM): Volume reached 10.4 MU in September 2024, with non-solar prices at ₹8.28/unit.

- REC Market: 10.31 lakh RECs traded in September 2024, at record-low prices of ₹110/REC.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/c48b1a7b-61ed-4ac4-aa1f-f67dd8e42f49.pdf

9 Likes

Here are some of the interesting questions and answers from the IEX Q2 FY25 Earnings Conference Call:

Market Share and Transaction Fees

- Mohit Kumar (ICICI Securities Limited): What is your market share this quarter versus other exchanges?

- Management: Our market share has been almost about 83% now.

- Mohit Kumar: On transaction fees, when we take the revenues and divide by the number of units, it seems like the transaction fee for this quarter is 3.7 per unit. Are we giving a discount?

- Management: In the case of the REC market, the rates have come down. REC rates are now almost about 120–110 rupees, so we have reduced the transaction fees because of that.

- Bani (Aequitas Park): In your opinion, will the transaction fee for all the electricity products be changed in the future, especially given that we ourselves have decreased the transaction fee in REC products where prices have come down?

- Rohit Bajaj (Joint Managing Director): In case of electricity, our transaction fee is continuing at two paise per unit on either side, right from 2011, when the electricity rates were almost about 2.5–3 rupees. Today, the electricity clearing price is almost in the range of 5 rupees. In spite of that, we have not increased the transaction fees. Even if you look at the trading activities happening in the sector, the regulator has allowed transaction fees up to 7 paise per unit.

Market Coupling

- Bani: Why should coupling RTM and SCED markets be considered?

- Rohit Bajaj: The CERC, in their order issued in February, clearly mentioned that their simulations for 3 months did not show any merit in coupling only the RTM market or only the Day-Ahead Market of the three exchanges. They have asked Grid India to run simulations and see if there is merit in coupling the RTM and SCED. However, theoretically speaking, coupling these two different sets of generators (SCED with long-term PPAs and RTM with merchant generators) is undesirable.

- Vir Matani (Jupiter Financial): In case market coupling goes through, how will IEX be affected?

- Management: I am very sure coupling is not going to happen, so let us not worry about that. In case coupling happens, we have ways and means to ensure that we are able to retain our market share and volumes when we come to that.

- DH Aaral (Systematix Securities): Does the power coming into the RTM market in any way bring down the benefit that could have possibly come out by coupling the SCED with the RTM market?

- Rohit Bajaj: The optimization opportunity is definitely reduced because the volume in the SCED market is very less—less than 28 million units per day—while the RTM market volume is about 100 million units. With the new government rule on the sale of unrequisitioned surplus (URS) power, about 20 million units of this power is being sold through the RTM market itself. This further minimizes optimization opportunities by coupling the markets.

RECs and Transaction Fees

- Sumit Kishor (Axis Capital Limited): During the September quarter, the REC volumes kept coming off from July, which was a very good month, followed by a lower number in August and a further decline in September. What was the dynamic here?

- Rohit Bajaj: Volumes were significantly higher in July because Bihar, a state with a large deficit, purchased a good amount of RECs to complete their RPO compliance that month. In August and September, their demand was not there, and because of that, the numbers have reduced.

- Vishal Periwal (Antique Stock Broking): On the REC transaction fee that we have revised, I just wanted to understand the rationale for it. When the volume for any product is going strong, what was the reason for reducing the fee that we charge?

- Rohit Bajaj: We felt that transaction fees should also be reduced since the rates for RECs have come down substantially, from earlier about 1,000 rupees to almost 120 rupees.

Diversification and New Products

- Jira (Keynote Capitals): Which one of the diversification initiatives—coal exchange or EPR trading—has the largest potential in terms of becoming sizable, and which is the one that you think will be started first or will commence operations soon?

- Rohit Bajaj: Both questions are difficult to answer because both initiatives are dependent on government decisions. Both will need some time, depending on government approval. For the coal exchange, it will take 6–8 months after the approval to start. Similarly, for EPR trading, we have to wait for the government to finalize regulations and appoint an agency.

- Ruchita Kadgi (IIFL Asset Management): What is the opportunity size in the REC segment in terms of volume?

- Rohit Bajaj: The opportunity is very high because many states, distribution companies, and industries are not meeting the RPO compliance norms specified by the Government of India. Now inventory is also available, and the rates have come down. It is a big opportunity, but again, it depends on market participants and the enforcement by the state regulators.

Other Interesting Insights

- The management shared that IEX’s market share has been gradually decreasing over the last few years mainly due to the introduction of long-duration contracts, where the competition is more evenly spread.

- IEX is accredited to issue iRECs (International Renewable Energy Certificates) through its subsidiary, ICX. However, the management admitted that the opportunity size in this segment is currently very small.

- The management highlighted the significant reduction in battery storage rates, which makes it commercially viable and presents opportunities for market development.

These are just some of the interesting questions and answers from the IEX Q2 FY25 Earnings Conference Call. They provide insights into the company’s performance, the regulatory landscape, and the future outlook of the power trading sector in India.

Note: Its AI generated, transcript from audio. Pls let me know if there are any erroneous info/notes.

Disclaimer: Invested and Biased. Less than 4% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any investment decisions.

20 Likes

need the full transcript, please share if you have it with you

1 Like

Here is the recording intimation and link to file. regards.

IEX_25102024215401_Signed_IEX_Intimation_Audio_Recording_Earning_Call_Q2_Sep24.pdf (249.1 KB)

1 Like

I have tried to read more on what management says, and trying to figure meaning.

1.

IMO, This doesnt make a case for non-coupling.

IMO, This doesnt make a case for non-coupling.

once i read this i get more questions …how theoratically it is undesirable ?..why would regulators bring up such stupid idea of coupling at all if its undesirable ?

I think i would follow up on this statement and try to study how IEX can do that, if they can do, it’d be interesting.

If i again go back to experiences with regulators, last time few organizations went to GERC with lobbyst/big recommendations etc on certain banking issues. Regulators didnt budge “these are too small amounts and you can manage”

So, i would like IEX to be successful here but i doubt if regulators would ever consider individual companies.

To me, coupling is the norm untill CERC formally abandons it, sooner or later in some sort or another it will be implemented till then. I think Mr.Market knows it . Why take risk without clarity ? I would rather wait on next results and their other verticals growth.

6 Likes

Market coupling has to come. It is need of hour due to vastly different nature of generation, Solar, wind, hydro etc. which generate electricity with highly unpredictable behavior where as consumption too varies. It is single gate (market coupling) which can ensure balancing between all these variables.

1 Like

The kind of balancing that is being expected can happen successfully only when majority of power being generated is traded via the power exchanges.

Currently 90% of the generated power is traded outside the exchanges (due to long/medium term PPAs), implementing Market Coupling at the moment is like putting the cart before the horse.

4 Likes

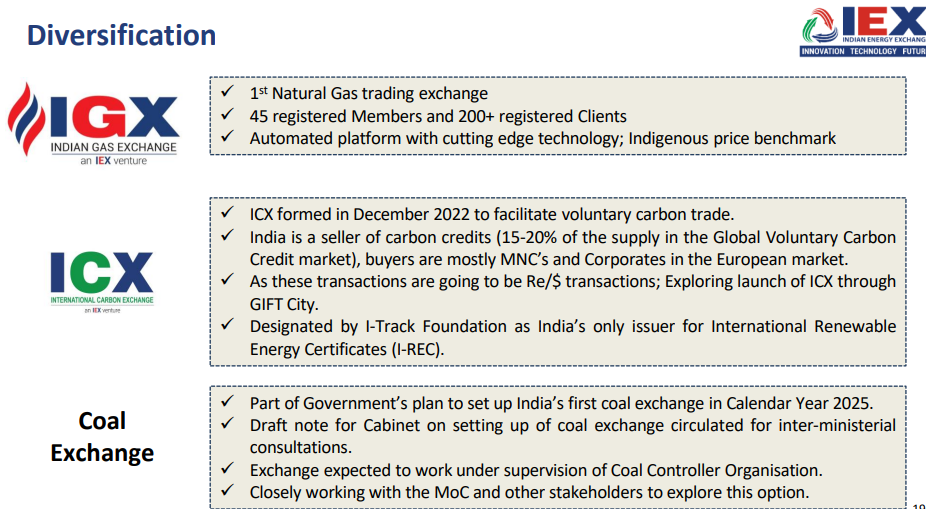

While everyone is focused on Market Coupling, here are some diversification and growth catalysts shaping IEX:

- Long Duration Contracts Pending CRC Approval:

- IEX has filed for approval of 11-month contracts, awaiting CERC’s final decision.

- Also filed for the Green RTM segment, offering premium pricing opportunities for renewable energy and enabling green power trading just one hour in advance, helping to manage weather-related supply variations.

- Launch of International Carbon Exchange Subsidiary:

- IEX’s subsidiary is accredited as India’s first renewable energy certificate issuer for globally recognized I-REC digital certificates (representing 1 MWh of renewable energy).

- Potential Launch of India’s First Coal Exchange:

- Recently announced by the Coal Minister; IEX is collaborating with stakeholders to explore this new platform.

- Draft Guidelines for EPR Trading and Settlement:

- CPCB’s draft guidelines for Extended Producer Responsibility (EPR) trading platform (for plastics, e-waste, battery waste, etc.) aim to enable transparent price discovery for recycling compliance certificates. IEX is evaluating entry into this segment.

- CERC’s Proposed Enhancements to Market Structure:

- Proposed changes in Term Ahead Market (TAM) aim to standardize products across exchanges, boost liquidity, and increase Real-Time Market (RTM) volumes due to stricter grid discipline requirements.

- Cross-Border Power Flexibility:

- CEA now allows plants selling power cross-border to redirect unscheduled power to Indian exchanges, potentially improving liquidity.

- Extension of Section 11 for Coal-Based Plants:

- MoP’s directive to operate imported coal-based plants until Dec 31, 2024, supports demand on exchanges.

- New Rules for Late Payment Surcharge (LPSC):

- Directives for long-term PPA generating stations to offer un-requisitioned power (URS) on exchanges, with 100 million units of URS power now available daily.

- Enhanced Compliance Norms Under Gujarat’s Energy Conservation Act:

- GERC’s stringent penalties for unmet renewable purchase obligations aim to strengthen the REC market, maintaining a vibrant platform for green certificates.

Overall, these developments enhance liquidity, help manage power prices, and support DISCOMs and C&I consumers in optimizing procurement costs. Positive signals for IEX growth!

17 Likes

Few takeaways from the last week’s exchange filing on October business’ update. DAM and RTM prices declined by 38% yoy; indicating in the near-term the volume should continue to increase for the exchange.

- IEX recorded a 4% year-on-year increase in electricity trading volume, achieving 9,642 MU in October 2024.

- The DAM experienced a 7% decline in volume in October 2024 compared to the same month in the previous year. However, the RTM achieved a significant 30% year-on-year increase in volume, reaching 3,123 MU in October 2024.

- The Green Market demonstrated substantial growth, with a remarkable 364% year-on-year increase in volume during October 2024, reaching 872 MU. This growth was driven by both the Green Day-Ahead Market (G-DAM) and the Green Term-Ahead Market (G-TAM). The G-DAM achieved 829 MU in October 2024, marking a 358% increase from the previous year. The G-TAM reached 43 MU, a 498% increase year-on-year.

- The REC market witnessed significant activity in October 2024, with 4.44 lakh RECs traded, representing a 105% year-on-year increase.

Interesting to see continuous traction in DII holding since June’23.

Disclaimer: Invested and Biased. Less than 5% of PF, recently added into this scrip. Post purely for study purposes. Consult your advisor before any investment decisions.

4 Likes

A good read!

How these developing story will play out for IEX? Although economically not viable for generators, seems eventually they all have to get these traded in exchanges.

2 Likes

You are right. Renewable energy sources like solar and wind are highly unpredictable power source. Thus, it has to be shunted via energy exchange. Even with reasonable pumped hydro storage it has to get transected via energy exchange in both directions. This is highly positive for IEX but again to come for price parity in both directions, a market coupling is must.

5 Likes

2 Likes

IEX’s Next Growth Lever: Carbon Credit Certificate (CCC) Trading

The Central Electricity Regulatory Commission (CERC) has issued a draft regulation for the Purchase and Sale of Carbon Credit Certificates (CCCs), 2024, creating a structured framework for trading CCCs on Power Exchanges.

This presents a major new growth opportunity for IEX as it can facilitate CCC trading alongside electricity and renewable energy credits.

Key Highlights:

![]() Objective: Establishing a regulated exchange for CCCs for both Obligated and Non-Obligated Entities

Objective: Establishing a regulated exchange for CCCs for both Obligated and Non-Obligated Entities

![]() Exclusive Trading on Power Exchanges: CCCs will only be traded on Power Exchanges, ensuring transparency and liquidity

Exclusive Trading on Power Exchanges: CCCs will only be traded on Power Exchanges, ensuring transparency and liquidity

![]() Market Segments:

Market Segments:

- Compliance Market for obligated entities

- Offset Market for non-obligated entities

![]() Price Discovery & Regulation: Market-based pricing within a floor and forbearance price approved by the Commission

Price Discovery & Regulation: Market-based pricing within a floor and forbearance price approved by the Commission

![]() Role of IEX:

Role of IEX:

- Managing CCC transactions in a regulated, transparent manner

- Enabling monthly trading cycles

- Ensuring compliance and reporting mechanisms

With increasing sustainability mandates and corporate carbon offset needs, IEX is well-positioned to capitalize on the growing carbon credit market, adding another revenue stream to its business. This could be a long-term value driver for IEX investors!

Source:

Mangement commentary from latest concall

3 Likes

May be its because it makes them feel like its AI generated and goes for vetting etc..also as anyone can flag the message …it goes as flagged and hidden …

Have they mentioned any monetary value which will be added to IEX , any time frame by when CCCs will go live on IEX ?

Just to understand the process of having a carbon certificate, Can you also elaborate, How CCCs are being issued at present and how such credits can be brought to IEX for trading ?

2 Likes

Taking into account the delays and adjusted timelines, Grid India should have completed the shadow pilot by Jan 2025. I am unable to find any information regarding this online or on the CERC website. Does anybody have any information in this regard?

1 Like

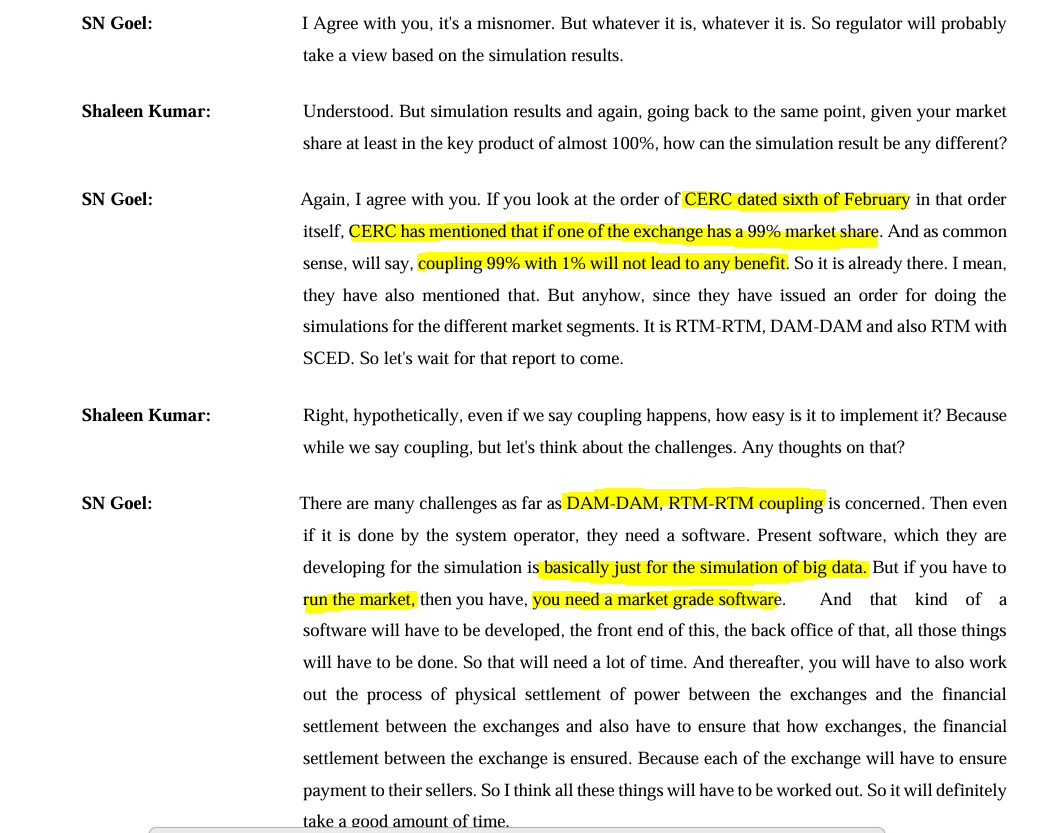

As per the latest concall, the whole conversation with IEX Management - Mr S.N. Goel gives us a decent view of where things stand on the MBED and market coupling front.

MBED was in discussion since 2018, but it ran into serious roadblocks because it aimed to centralize scheduling, which most states weren’t comfortable with. States currently have control over their scheduling based on PPAs and allocations, and under MBED, they would’ve had to give that up. So over time, MBED was more or less dropped and is no longer being actively pursued.

On the market coupling side (or more accurately, exchange coupling), IEX has consistently maintained that it doesn’t really add any value. Their key point is that when one exchange already has ~99% market share, coupling it with another that only has 1% doesn’t make much sense. It wouldn’t lead to meaningful efficiency gains and could potentially stifle competition and innovation in the market. IEX has already made submissions to CERC on this and raised these concerns in response to the staff paper.

Even CERC, in its February 6th order, noted that coupling 99% with 1% offers little benefit. Still, they’ve asked for simulation exercises to be conducted across segments like DAM-DAM, RTM-RTM, and RTM- Security Constrained Economic Despatch (SCED), possibly to formally validate this before taking a final decision.

That said, IEX pointed out that the software being used for these simulations isn’t capable of running a live market - it’s only meant for data simulation. For actual market operations, a full-scale market-grade software platform would be needed, including backend, frontend, and settlement systems (both physical and financial). That development alone would take significant time and investment. Especially in the case of RTM-SCED coupling, it could take 2-3 years due to the complexity of algorithms and the large number of participants involved.

Now, coming to your question about the shadow pilot that Grid India was supposed to complete by January 2025 - there’s no official update or confirmation available online or on the CERC website so far.

Based on how things were progressing and the challenges mentioned, there’s a good chance the timeline has slipped. Also, it’s not unusual for these kinds of pilot results to be submitted first to the regulator and only later opened to the public or stakeholders.

Sources: IEX Latest concall

6 Likes