With this IPO, IEX plans to reduce its current stake from 46% to 25% in IGX !

Whether the IEX share holders would get a preferential allotment in IGX IPO needs to be seen.

With this IPO, IEX plans to reduce its current stake from 46% to 25% in IGX !

Whether the IEX share holders would get a preferential allotment in IGX IPO needs to be seen.

Even though bringing down the stake in IGX to 25% is a regulatory requirement, there are lot of positives for IEX in this move:

As per IEX chairman, IEX still has 3.5 years before they are required to offload the extra 21-22 percent stake in IGX. Development of IGX is definetely a positive for IEX but the stake sale is happening way before IGX is given a chance to grow and mature.

Selling equity to strategic partners like Adani,torrent,ongc,iocl,nse makes sense but would it not be better to do that in the last year of deadline to get better value for IGX?

Or selling now so that you have the equivalent of vendor lockin of at least assured trades from the same players as compared to other Xchge players who mature in 3 years and offer huge discounts to get the same pool of producers and consumer initially; at that time you probably can’t charge premium valuations as there are choices for the participants?

I think IGX went from being subsidiary to being an associate by virtue of this transaction.

Interesting read

Interesting.

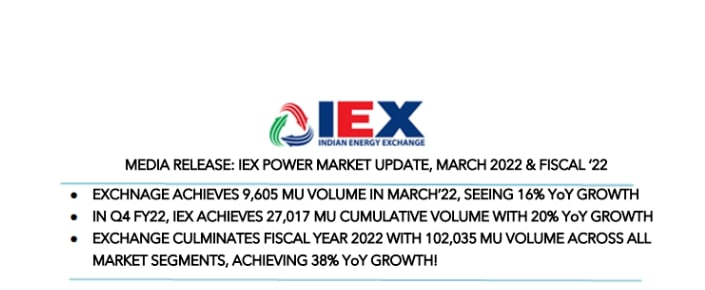

Shouldn’t this lead to higher volumes on the exchange since there was clearly a pricing gap in the market for the last month or so

Volumes,in my humble opinion, on the power exchanges will improve this quarter due to robust demand. This season generally sees more demand historically.

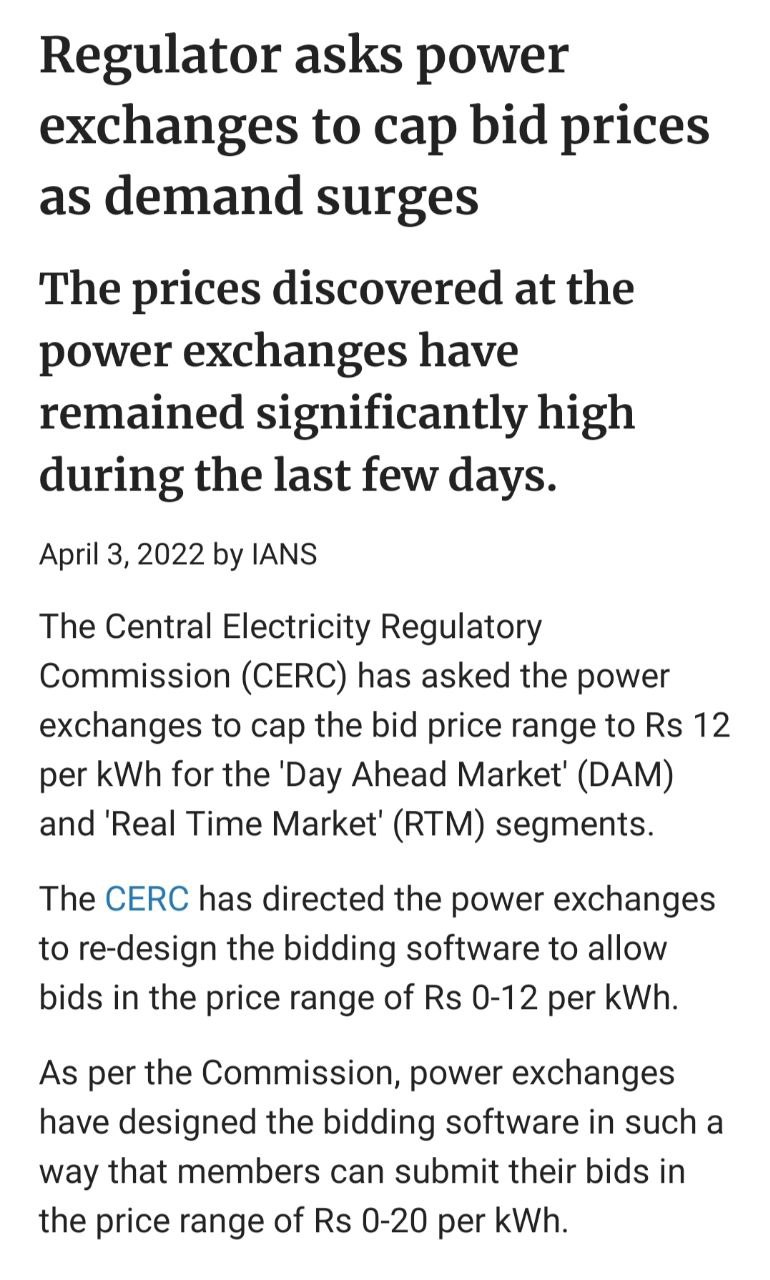

This capping of unit prices is good for the consumer but i do not think it will have a big impact to improve volumes. It’s a positive development nonetheless.

volumes going to increase this time in a big way. year 2020 and 2021 was kind of quite less delivered in terms of volume traded in IEX. due to lockdown in all major parts in country and closing of commercial institutions energy demand was significantly less. this time a normal year and rebound action on industries huge demand is anticipated. this is the only reason CERC has caped the unit prices in price discovery.

d: invested.

An interesting development that augurs well for IEX.

Disc: Invested

Good growth YOY for iex

Numbers in-line with a topline growth of 18% to 20%

Q4FY22 vs Q4FY21 (yoy)

Rev up 18% at Rs.111.72cr vs Rs.95.02cr

EBITDA up 18% at Rs.95.07cr vs Rs.80.84cr

Margins stable at 85% vs 85%

PAT up 27% at Rs.80.8cr vs Rs.63.8cr

IMO, 3 back to back quarters with almost flat numbers is not a very good news, particularly in an environment where we have lot of short term triggers (sky rocketing fuel prices, ever-increasing peak load) in favor of exchange traded power.

Disc: Invested