I am also slowly coming to a similar conclusion. Bought the stock around Rs 150-180 levels as it was really undervalued at the time. 20x PE for a monopoly business in a under penetrated industry was criminally low. But now that the PE has run-up to the desired levels (maybe more) we have to solely rely on EPS growth for any share price gains.

Wanted to understand the views of fellow boarders here - what is the 5 year EPS CAGR expectation for IEX? Most research reports have modelled a 20% EPS growth for the next 2-3 years. If thats the case then it doesn’t make much sense to hold the stock as even a slight PE multiple correction means you end up with zero/meagre returns over the next 2-5 year period.

Totally agree with you on the valuations part. No margin of safety remaining and seems priced to perfection/overpriced even.

But looking at possible reasons for this rerating, there are a few things that come to mind, wrt a few recent developments -

Unchanged transaction fees in Power market regulations 2021 - Margins protected

MBED draft paper confirming phase 1 execution with NTPC plants moving to IEX to sell their power by Apr 2022 (uncontracted power only? will the timelines be honoured?) - Inorganic (pushed by govt) volume growth scope

Market coupling has been pushed back/delayed and the definition of the coupling operator has been withdrawn, indicating that price discovery might actually be given back to the exchanges - Optionality towards maintaining the monopoly/market share

I personally won’t be adding further at these prices but i think there is an equal chance for surprises on the upside as on the downside driven by cross border trading + volume growth due to MBED and op leverage so we might end up getting that 20% EPS growth.

Will be holding and seeing how the triggers play out. Worst case is a bear market/sentiment driven multiple derating which is a chance to add unless any of the key risks play out

Key risks - Unless there’s a regulation mandated margin contraction or market share contraction due to competition/market coupling, this company will be a steady compounder + cash generating monster in the coming future

I bought this business around 130 levels in Covid panic. Here is my two cents on current valuation.

We do not know how high the valuation can run up and sustain there. Considering how much cash the business generates, it can increase its EPS just by buying back the shares and there by decreasing the denominator (no of shares) while increasing earnings at 25%+. So judging by PE and evaluating solely based on EPS and its growth isn’t right, in my opinion.

This is one of those businesses that generates a lot of cash but doesn’t need any. The 50% mandate of dividend still leaves a lot of cash on balance sheet. I believe eventually the business will keep providing steady dividend along with occasional buybacks.

I haven’t added more post it crossed 200 but I wouldn’t sell it either even if it corrects by 50% from here. The dividend yield alone is very lucrative on this. In fact I will add more if it corrects in panic market like Mar’20.

Very interesting discussion on valuation. This is where the ‘art’ part of investing comes in.

Apart from the factors that Tar mentioned, the longevity of the business is another factor which might continue to give hefty P/E multiples. The power market in India is still in fairly early stages and far from reaching mature levels. Over a period of time I would expect more business moving to exchanges and with focus on renewable energy some of which is not a 24x7 supply the exchanges will have increased role to play with time.

I would not worry about P/E multiples at this point in time. It may very well time correct for a period of time, but if we sell out now, we may miss a long term compounder.

Of course, more exchanges, regulatory changes etc. can upset the story. We don’t know what we don’t know - hence the story requires monitoring.

Question to some senior members here >> I have been following this discussion, I see that the biggest risk that everyone is talking about is regulation and PTC, as a stock strategy does it makes sense to divide investments in both PTC and IEX, given that even if any one of these takes off, it should give handsome returns in future given the upside.

I am looking for an analysis on approximating IEX revenue for the quarter based on the publically volume information across products (DAM, TAM, RTM etc.). If anyone has done work on this, would be great to understand. I am sure it will benefit many people and also add some color to the valuation debate.

lets fast forward to 2033. India’s energy growth grows at 6% / year for 12 years

Power exchanges, which had 6% of electricity share grew to 60% with industry annual revenue growing from ~ 300 cr to 3000 cr.

It is still extremely capital light so pre tax profits are approx 2800cr = 2000cr post tax profits.

Lets assume IEX has 50% market share because of 1st mover advantage etc, meaning PAT = 1000cr.

A reasonable multiple for an industry growing at 6% per year ~ 12-15 meaning a market value of 15000cr in 2033.

Valuation in 2021 - 12000cr…

missed it thanks for pointing it out, iex pat with these hugely ambitious assumptions would be 2000cr, giving it a rough value of 24000cr, meaning cagr of 6% in the value of the company + dividends whatever they may be

While this makes it clear that the risk reward at the current mcap is not in our favour, we seem to be completely ignoring optionalities like IGX, derivatives (huge potential), RECs etc with an estimated 400-450GW of just green energy estimated to be installed by 2030

Seems to be a futile exercise to try and predict revenue sources 10y down the line as every business will have these kinds of terminal risks to find ways to keep growing and innovating, this isn’t any different. The hard upper limit you are assuming here is purely basis the spot market which is the country’s installed capacity (should be even lesser with long term contracts)

No better cue to take than equity exchanges/foreign power exchanges where derivative volumes/turnovers are several times of the spot volumes. Derivatives and margin lending (IEX has this facility for certain participants as i read somewhere) is where the real growth is always at as evidenced even by most equity brokers who also make maximum cash off FnO/margin (anyone interested can check out the S1 filing for Robinhood’s IPO)

Even a factor of 2x from these optionalities combined would take the terminal mcap to ~50k cr (even with a rock bottom PE of 12) which is a respectable ~13% CAGR excluding buybacks and dividends. It’s clear that a small variable here or there is impacting CAGR hugely, so not going to even attempt

As far as I am aware, derivatives may not be a big revenue driver as they will be traded on MCX and only the settlement price will be taken from IEX. Will need to wait to figure out the revenue share for IEX but the press release looked as if they will only provide the settlement price. If IEX is able to get a sizeable share of revenue from derivatives it can be an even bigger market than spot market if we take the example of Europe.

Plus as people have mentioned, IGX is yet to take-off and will have to see what sort of numbers it is able to generate.

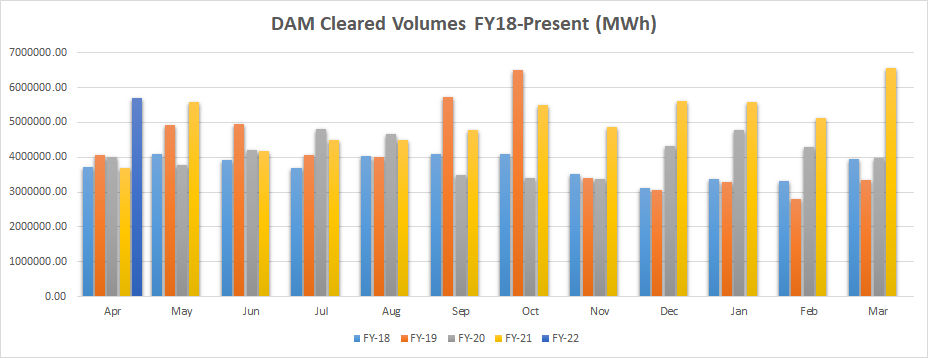

Another interesting point from the recent investor presentation was that short term market share has almost doubled to >6.5% over the last 3 years, will need to see if this was a temporary phenomenon due to Covid or will it sustain.

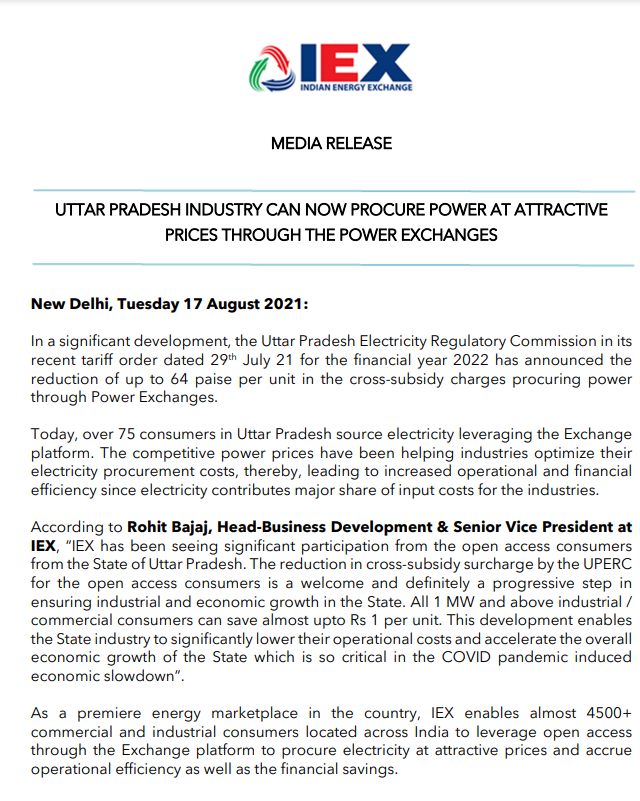

NTPC traditionally supplies power under PPA’s but this is the first time company is offering to sell power on an open access basis. any possible impact for IEX over a short/long term? if in case, all genco’s starts practicing the same?

I agree PTC being PSU declare lots of big plans on papers but really to execute it is difficult. If PTC fails than clear winner IEX will be benefited lot.

You enter into the power purchase agreement with the supplier (long term contract for a fixed price )

New School

Your entire system is integrated ( I have 6 plants across India and other offices ) I might be using a software like SAP or something else , I know my consumption and my system can predict how the demand for next day and next week and next month based on my production ( or sudden lockdown in the plant could be due to be some incident or covid or anything else ) , since I have more clarity and control and my SAP system is now integrated with IEX platform ( please read earlier posts / concalls where this solution is already implemented by IEX) I can see what is my total requirement what is the ongoing price and my system can do modelling and can trigger an auto order to IEX exchange . This is one of the real example . I am sure more will very soon follow this route.

Now if we take this discussion a step further , the entire transaction can be executed seamlessly by using a blockchain based ledger transaction, so everything from prediction of the usage / demand → Price discovery on the IEX platform → Order placement → Order execution → Payments → tracking the total units available to consume … this process flows goes on with zero human intervention

Many thanks to @Worldlywiseinvestors for bringing it to our attention to understand the thesis with a live example