Q2FY21 CCT Notes:

MISC.

Power demand -0.5% in Q2. Renweable at 89GW, 24% of installed capacity.

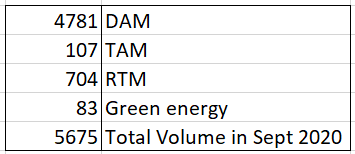

4.9% yoy Op.Rev, 0.8% yoy tot. Rev., -4.4% yoy PAT. 13.2% yoy volumes.

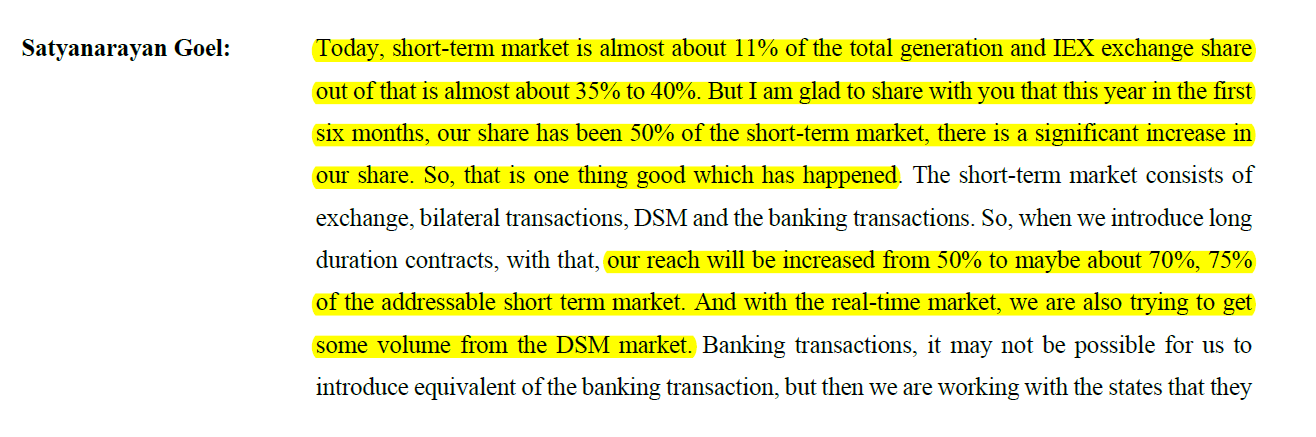

Addressable market is 12% of total generation. We are 40% of it. In H1FY21 we were 50%. With long duration contracts we could reach 75%. Banking transactions we are working on it with the states. It will not be equivalent to what DISCOMs do, but the states can sell power on the exchange and bank that money and use it later to buy power when needed. We will cover the entire ST market with these products, but how much MS we will get is unknown. Banking txn volume is 10-12 BU. Rest is bilateral.

Regulatory

UP has issued DMO on DPPO Reg. 2020. To procure power from exchanges. Already in place in Delhi, MH, should serve as a precedence for other states.

Filed with CERC to commence trade in long duration delivery based contracts. Quorum not available in CERC. Waiting on PMR. We filed for LT contracts to save time. CERC will only give approval when the case is settled in SC. This was a joint app. by CERC, SEBI, MOP. Was filed an year back. But SC is only taking urgent cases. Date was 8th OCT. Now Dec 1st week.

Number one, derivatives in electricity can be introduced only after the jurisdiction issue is settled by the Supreme Court. Because today derivative will be regulated by whom? That is an issue. In fact, SEBI, CERC, Ministry of Finance, Ministry of Power, they all discussed this issue, minutes have been signed, and they have been filed with the Supreme Court, that derivatives will be regulated by SEBI and long duration, delivery contracts will be regulated by CERC. So, once that case is disposed off by Supreme Court, then SEBI will be able to introduce financial contracts in electricity also. And these will be introduced on SEBI regulated exchanges. But you know this will have advantage in electricity market also. There is lot of volatility in the price. So user will be able to hedge his position in the derivative market and take delivery in the spot market. So a part of the bilateral contracts will then get shifted on the exchange platform

Advocating on allowing unrequesitioned power in DAM. But not accepted by regulator. It would bring a lot of liquidity to DAM.

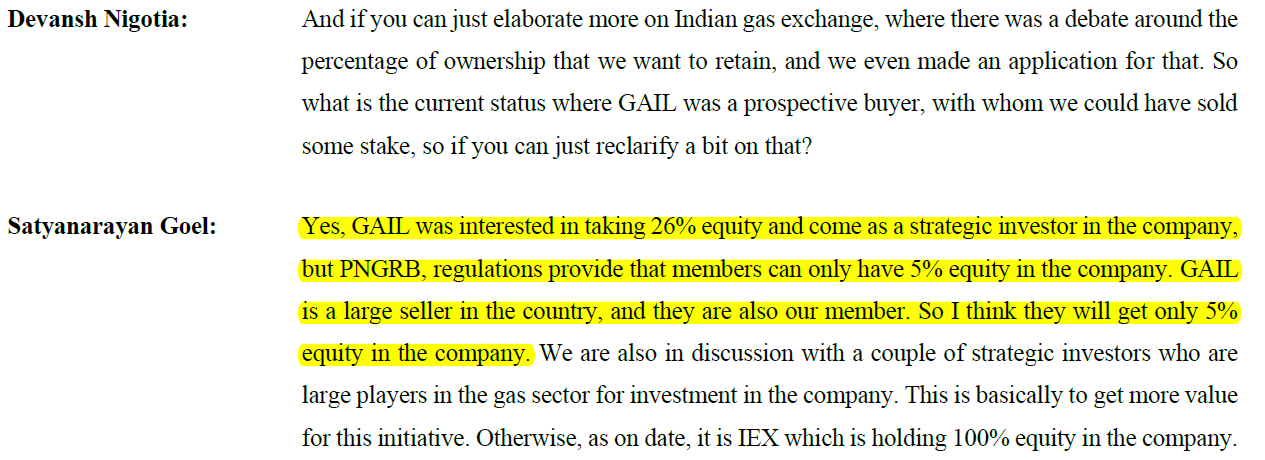

GAS

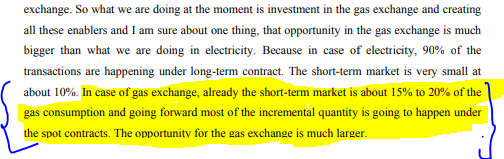

When we started electricity exchange in 2008, at that time, all enablers were in place for starting the electricity exchange, enablers like, we had a system operator, which is NLDC, RLDC, SLDC. There was a deviation settlement mechanism which was in the form of UI. We had open access regulations by CERC, non-discriminatory open access to all participants. There was no taxation on interstate sale of electricity. So all these issues were settled. And the trading of electricity became a reality from day one when we launched IEX. In case of gas exchange, we knew that many of these enablers are not in place. But then even to get these enablers in place, there is a lot of policy advocacy to be done. We launched this exchange and activities are happening but then transactions will happen in a big way only when these enablers are in place. First thing is gas market regulations. We launched the gas exchange on 15th of June. In the month of July, the draft regulations were issued. And after the public hearing, the final regulations were issued on 28th of September. So, that is one enabler which is now in place. PNGRB has issued draft regulations for the access code and also issued regulations for the gas transportation tariff, and they are again coming out with the simplified gas transportation tariff system in November which is required for the exchanges. So that is other activity which is workin progress. Gas is unfortunately not under GST. So, different states have got different taxation on the gas. And because of that, it is very difficult to introduce standard contracts on the gas exchange. We are working with the government. What we understand is that government has already referred this issue to the GST Council. Hopefully, that should also happen in the next couple of months. On System operator, GAIL is already working in this area. They have in one of the offices, all pipelines, metering systems, all those activities have been provided, all information systems are available now with them, they are also going to do this data gathering from the other pipeline operators. So I think system operator also will be operational maybe in the next couple of months. So, on all these enablers, it is work-in progress. It may take another five, six months and only thereafter, we will see gas trading in a big way. Even if you look at the infrastructure part of it, gas LNG terminals, regasification terminal, today we have only two regasification terminals which are operational which is by Petronet and Shell. Petronet terminal is overbooked and operating at more than 100% capacity under the long-term contracts. Shell terminal also operating in 100% capacity. So, if you want to develop the market, I think we need more terminals so that spare capacity is available for the traders who want to bring cargo and sell in the market. A lot of activities are happening on the regasification terminal. I understand work is happening on five, six terminals and maybe two, three terminals will get commissioned in the next one year. Pipeline also, lot of work in the eastern and southern part of the country is happening. We should see interconnected gas pipeline network in the country, the way we have for the electricity, and that will be the time when we will have real good volume on the gas exchange. So what we are doing at the moment is investment in the gas exchange and creating all these enablers and I am sure about one thing, that opportunity in the gas exchange is much bigger than what we are doing in electricity. Because in case of electricity, 90% of the transactions are happening under long-term contract. The short-term market is very small at about 10%. In case of gas exchange, already the short-term market is about 15% to 20% of the gas consumption and going forward most of the incremental quantity is going to happen under the spot contracts. The opportunity for the gas exchange is much larger.

RTM

Yes, initially, we thought that a substantial part of DSM will get shifted to the RTM market. But actually, what has happened is our intraday TAM transactions, they have now reduced practically to zero and the transactions have got shifted to the RTM market. Because that makes a lot of sense also, now distribution companies can buy on real-time basis, and at a competitive price. At the same time, volume in the RTM markets are much more than what we used to do in the TAM market. So, a good part of the volume is also the additional volume for the exchange. Because of the competitive price, many of the states are replacing the high variable cost by purchasing power in the real-time market. We are working with the states. We are doing analysis of the power drawn by the states under DSM, what kind of penalty they have paid, at what rate they have overdrawn that power and does it make sense for them to replace that DSM power by the exchange power. We are doing all that kind of analysis. Tt will take some time but some shift from the DSM to RTM will definitely happen.

NTPC is selling on RTM, entire power is allocated to states, states have the right to revise schedule with 90 mins notice. As per regulations unrequesitioned power can be sold on RTM.

We are working on that. If you look at the DSM price, DSM price are linked to the day-ahead price, with the reduction in the clearing price in the day-ahead market, the DSM rates also have reduced. DSM becomes costly only in the event there is overdrawl beyond the specified limit. So we are doing these calculations for state-by-state. What is the quantum of overdrawl beyond the limit, what kind of rate and penalty they have paid under these overdrawl, and whether there was an opportunity for them to optimize and how they could have done that? I think these kinds of analysis and interactions with the state over the period of time then only we will be able to get the volumes from the DSM to the real-time market.

Long Duration Contracts

In the long duration contracts, I do not think there is a risk of cannibalization of the DAM markets because DAM market is on day-to-day basis, it is the difference in the demand and supply of the distribution company which gets purchased from the market. Long duration contracts will be basically getting volume from the bilateral market. Today, bilateral market, volumes are also about 40 billion units. So maybe part of those volumes will get to the longterm contracts.

IEX vs DEEP

On the DEEP platform, it is only discovery of price which is happening. Once the price is discovered, then the DEEP platform will indicate who are the and thereafter it is up to the distribution companies to enter into agreement with those sellers. And then future delivery, financial and physical settlement is happening between the discom and the seller directly. DEEP platform is only doing price discovery after that their role is over. In case of our long duration contracts, there are going to be auction mechanism, and also matching mechanism. In addition to price discovery, we will do physical and financial settlement also, we will take open access and ensure the supply to the distribution company and payment to the generators on daily basis. That is the value add which we are going to provide.

REC

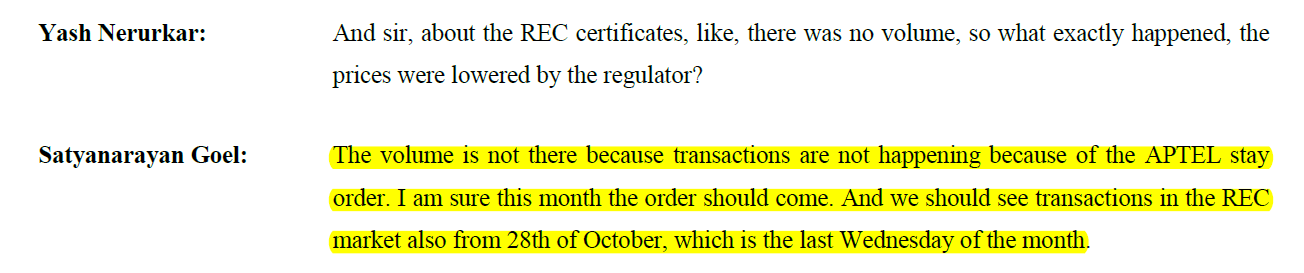

APTEL will hopefully declare the result which is in reservation before OCT-28th. Everyone in industry has requested for the order before that. No transactions have happened for 3 months. There is no other product available to meet the demand. Pent up demand scenario cannot be forecasted as states have given carry forward benefits to DISCOMS. Price has reduced by CERC, demand could be higher.

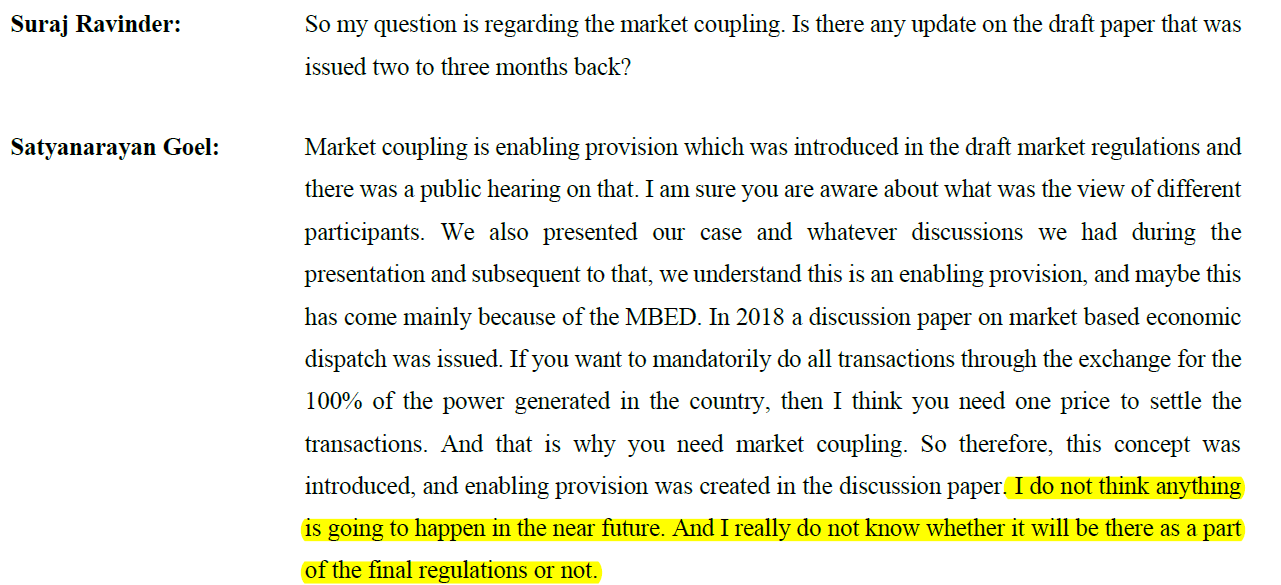

Market Coupling

Market coupling is enabling provision which was introduced in the draft market regulations and there was a public hearing on that. I am sure you are aware about what was the view of different participants. We also presented our case and whatever discussions we had during the presentation and subsequent to that, we understand this is an enabling provision, and maybe this has come mainly because of the MBED. In 2018 a discussion paper on market based economic dispatch was issued. If you want to mandatorily do all transactions through the exchange for the 100% of the power generated in the country, then I think you need one price to settle the transactions. And that is why you need market coupling. So therefore, this concept was introduced, and enabling provision was created in the discussion paper. I do not think anything is going to happen in the near future. And I really do not know whether it will be there as a part of the final regulations or not.

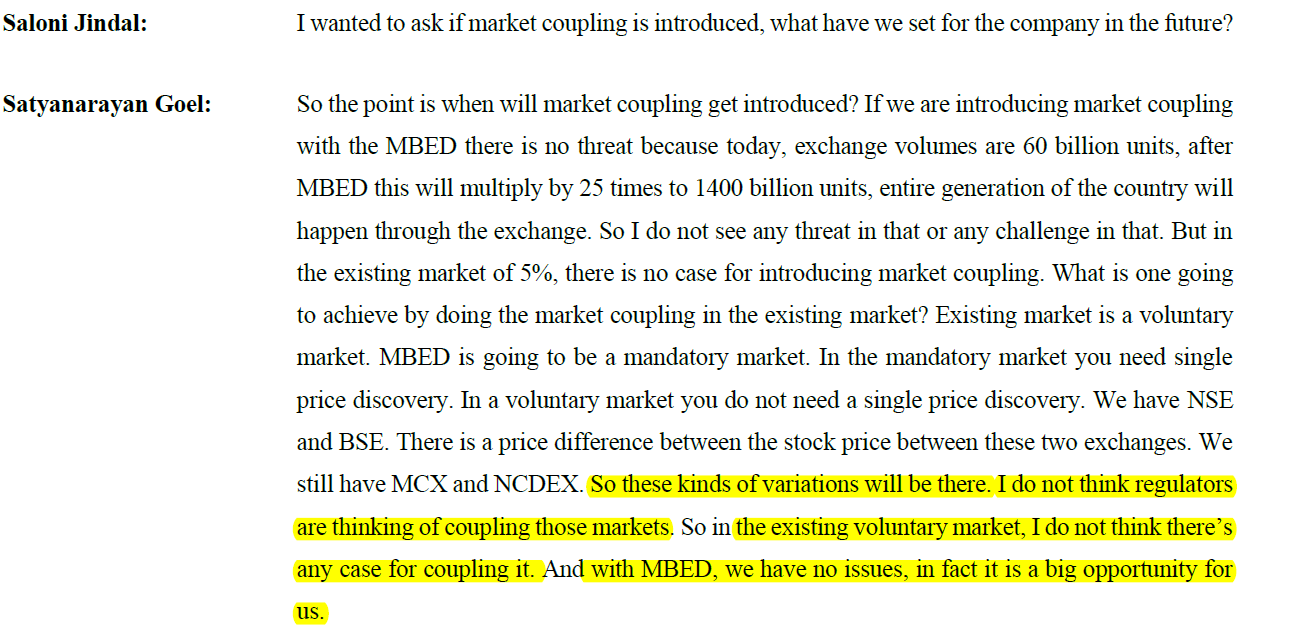

So the point is when will market coupling get introduced? If we are introducing market coupling with the MBED there is no threat because today, exchange volumes are 60 billion units, after MBED this will multiply by 25 times to 1400 billion units, entire generation of the country will happen through the exchange. So I do not see any threat in that or any challenge in that. But in the existing market of 5%, there is no case for introducing market coupling. What is one going to achieve by doing the market coupling in the existing market? Existing market is a voluntary market. MBED is going to be a mandatory market. In the mandatory market you need single price discovery. In a voluntary market you do not need a single price discovery. We have NSE and BSE. There is a price difference between the stock price between these two exchanges. We still have MCX and NCDEX. So these kinds of variations will be there. I do not think regulators are thinking of coupling those markets. So in the existing voluntary market, I do not think there’s any case for coupling it. And with MBED, we have no issues, in fact it is a big opportunity for us.

What I told is that in the present market model, which is a voluntary market, there is no compulsion on participants to purchase power from the exchanges. It depends on the demand and supply position. They can contract the shortfall through the bilateral market also or through the exchange and they can purchase power from any of the exchange, it is a voluntary market and it is only 5% of the total generation happening through this market. And IEX is already having 99% kind of market share in the day-ahead market and real-time market. So the competitive price discovery is already happening. I do not think we are going to get any additional value by doing market coupling in the existing model. And there is no need for doing market coupling in the existing model. But if you are going to implement MBED, in the MBED, entire power of the country is going to get dispatched through the exchanges. If that happens, then you need a common clearing price. You cannot have three clearing prices of the three exchanges. So since you need a common clearing price, and market coupling makes some sense if you want to implement MBED and if MBED is implemented then the entire volume which is 1400 billion units in the country, generation taking place, the entire generation will come to the market. So then there is no challenge. I mean, we are doing today 60 billion units and even if we get 50% of the market share, it becomes 700 billion units. So that is what my point is.

MBED

Let me interrupt you. For discussion on MBED, we need one full good hour. I am willing to spend time with you. Let me tell you in brief that, with MBED the intention is to dispatch entire power of the country through exchange to meet entire demand of the country on the most efficient manner. So it is a true merit order despatch which will happen under the MBED. It is very simple to hear. But if you want to implement this process, there are many complications. All those complications will have to be addressed. You have to pay the capacity charges, you will have to pay for the energy charges on daily basis and there is going to be contract for difference, all those things will have to happen. I think it is as complicated as GST, very difficult to implement in the country. You also need the consent of the state. So I think it will need time, not going to happen very soon.

Open Access

Yes, there has been significant increase in the open access volume during this last six months, increase of almost about 32% in that in the last 3 months, mainly it has happened because of the low clearing price, our clearing price during this time was about Rs.2.50 against Rs.3.15 in the last year. So, the increase in open access was mainly on account of the low clearing price. States are still not encouraging open access. The tariff barriers and non-tariff barriers are still being created. We are working with the states and the state regulators. But the access is in a very limited manner. Open Access volume in first half is 26%. And if you look at second quarter, it is about 32%.

GTAM

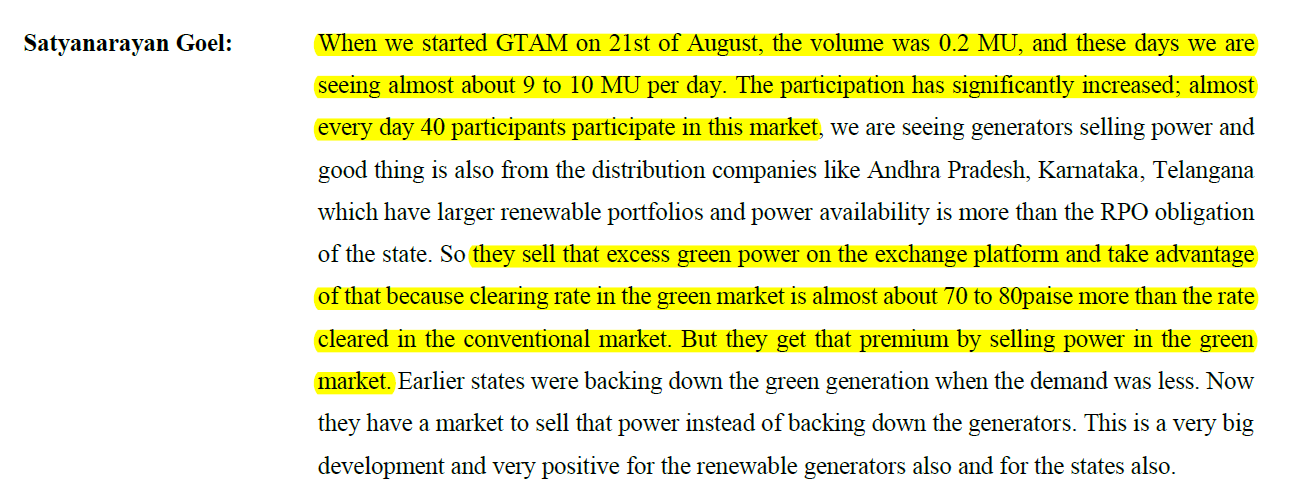

When we started GTAM on 21st of August, the volume was 0.2 MU, and these days we are seeing almost about 9 to 10 MU per day. The participation has significantly increased; almost every day 40 participants participate in this market, we are seeing generators selling power and good thing is also from the distribution companies like Andhra Pradesh, Karnataka, Telangana which have larger renewable portfolios and power availability is more than the RPO obligation of the state. So they sell that excess green power on the exchange platform and take advantage of that because clearing rate in the green market is almost about 70 to 80paise more than the rate cleared in the conventional market. But they get that premium by selling power in the green market. Earlier states were backing down the green generation when the demand was less. Now they have a market to sell that power instead of backing down the generators. This is a very big development and very positive for the renewable generators also and for the states also.

One is in the green term-ahead market, our transactions are 1 GW in the peak hours. The transaction is mainly happening during the daytime. So, average, if you look on daily basis, the volume is about 9, 10 million units. Today, there is no generator which has got merchant capacity. Entire renewable capacity is tied up under the long-term contract. So, the participation is more by the distribution companies. The distribution companies who have got surplus renewable power generation, beyond the RPO obligation, they are selling power on exchange platform. But then, if you look at the clearing price of the day-time market, this price is about Rs.3.40 which is a very lucrative price considering that price discovered under the bidding route for the renewable generators, which is around Rs.2.50. So, I am sure looking at this price, maybe in future a couple of IPPs will set up capacity under the merchant route or they will keep 10% to 15% of their capacity for selling in the market and try to take advantage of this market. So, this is how the market will get developed. Ramping up from 1,000 MW today to maybe 10,000 or 15,000 MW, will take time, I mean, we have created a market and people will now see what kind of value they can take out of this market and accordingly make investment for selling power in this market.

Buyers are more than sellers right now. But on the sell side, we are seeing active participation of the state distribution companies which have surplus power, and today it is Karnataka and Telangana who are participating, but in the near future, we are expecting even Andhra Pradesh or Gujarat or Rajasthan or Maharashtra who have large renewable capacities to participate in this market.

Coal Exchange

On Mjunction and MCX, it is very difficult to say what kind of a coal exchange they are talking about. Because what I understand about exchange is exchange which is doing price discovery and also physical and financial settlement. Physical and financial settlement can be done for a commodity, in which there is no issue regarding quality and quantity. If you look at electricity or the gas, these are measured by automatic online measurement of the quality and quantity. In case of coal, I am sure you are aware what kind of coal we have and what kind of issues we have in the coal market. So, whether it is going to be a coal exchange, or it is going to be a reverse auction mechanism for price discovery similar to what we have on the DEEP platform, I am not really aware of what is their business model.

Merit Order Dispatch

Let me briefly explain you what a merit order dispatch is. Normally states are purchasing their power based on the long-term contract. So, they try to meet the demand through the long-term contracts and if there is a shortfall in demand, then they purchase power through the bilateral or the exchange. Now, regulator in case of Maharashtra and Delhi, have said very clearly that when you are setting your merit order, you should also factor in the exchange clearing price. If exchange clearing price is lower than the variable cost of some of your plants with the long-term contracts, you should back down the power from those costly plants and purchase power from the exchange. That is a true merit order because you are replacing high cost variable power. And there are many plants in the country where the variable cost is much higher than the exchange clearing price. So, if everybody starts doing merit order dispatch, then in that case, you will find that the objective of MBED will be automatically met through this merit order dispatch process.

ST vs LT Market

Yes, short-term market is hovering around 10% to 11% from the last I think four or five years. But government is seriously working in creating more liquidity in the short-term market. There are a few things which are happening now. One is long-term PPAs are not happening. So, whatever is the incremental demand, either it is met by the existing long-term contracts or it is going to come to the short-term market. The short-term market volume with the increase in demand will definitely go up. It is unfortunate that last year, the increase in demand happened only by 1%, and this year, there is a decline in the demand, and we may end the whole year maybe at a level of the last year or maybe lower than that. So that incremental demand has really not happened in these two years. That is why the volume in the short-term market has not increased. Secondly, government has already decided that the old inefficient plants will be phased out because they are not complying with the environmental norms. So, when those plants are phased out, these plants are supplying power under the long-term contracts. A part of the demand also will come to the market. Further, cross-border transactions which should happen anytime, CERC has issued regulations, the procedure is to be issued by the CEA. I understand that it is into the final stages. So, if that happens, that also will bring some volume to the shortterm market. I think these are the drivers for increasing volume in the short-term market. This should take the short-term market from 10% to 15% in the next two, three years.

GTAM vs REC

Today, generators who have set up capacity under the REC market, they have contract with the state distribution companies for supplying power to the discoms at the average cost of power purchase of the distribution company, and the green attribute they sell, they get REC for the green attribute and sell that to REC. In future, it is left to the IPPs whether they want to sell power in the renewable market, in the GTAM market, or they still want to sell power to the distribution company and take REC for the green attribute. But looking at the market clearing price and the payment position of the distribution companies, I am sure generators will be inclined to sell power in the green market and thereby they will be getting better valuation and also the prompt payment.

so, if a person is selling a green REC on the REC platform and is selling power to the distribution company, the combined price which he is getting, would that be higher than what he is getting on the green term market as of now, because that will define upon…?

It depends on what time the contract was signed. If the contract was signed five years back, at that time, the rate for the renewable power itself was Rs.5 per unit. But today, a state distribution company will not sign a contract to purchase power at a rate of Rs.3 or Rs.3.50. Under the bidding route, the rate is Rs.2.50. They would like to purchase green power which has got both energy and the green attribute. So, capacity addition under the REC market is not expected in future. Capacity addition will happen under the green market now.