Please use operating cashflow instead of this as PAT< Operating cashflows due to longer subscriptions sold by company to its suppliers (greater than 1 year) that would be better to forecast as deferred revenue is huge component and it creates float for company as it receives money in advance and recognise revenue later but expense being upfront in nature.

1 Like

Based on the 2025 annual report Indiamart has about 1500 cr investments in Mutual Funds and about 1200+ cr in Corporate bonds and Govt secs. My question is on the tax efficiency of these investments. On the capital gain from these investments the company would be paying CG Tax. In addition as the capital gain is part of other income to the company, they would also be paying corporate Tax. Is my assumption correct. I am naive on this subject. could someone clarify please..

If capital gains tax is paid, there will be no corporate tax again on the same income.

8 Likes

Nalanda India Equity Fund buys 11,17,834 shares @ 2110 INR via bulk deal. First new position in years.

Disc: Not invested, tracking.

7 Likes

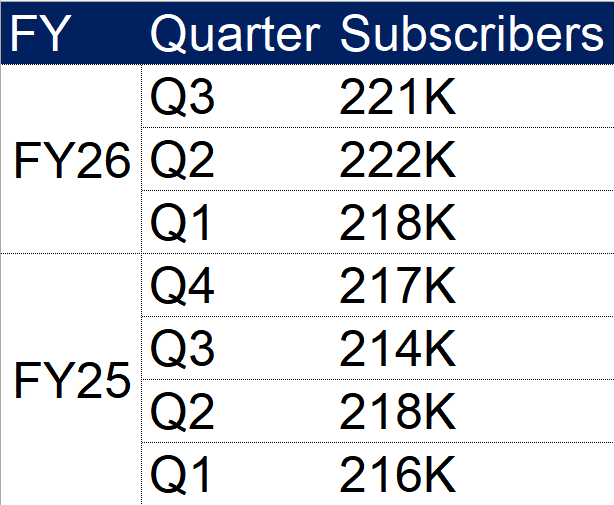

A question for those tracking IndiaMart, is anyone else concerned about the subscriber count staying flat? It’s been hovering around that 220K mark for nearly 7 Quarters now. The MSME market is around 63M, so is this stagnation on purpose to boost ARPU, or are they running out of people willing to pay? At what point does the lack of volume growth become a major red flag for the business?.

Disc: Not invested, tracking.

2 Likes

1 Like

63M number is a vanity TAM, many would be in business where IndiaMart cannot add value or limited to regional pockets of demand due to logistics cost.

Stagnation seems to be on purpose and imo necessary for the survival of business model from negative network effects. Chasing growth in supplier count by onboarding questionable suppliers would adversely impact the experience of buyers and once buyer brand IndiaMart as untrustworthy platform they may think twice before returning. Once the high intent buyers dry up so would the platinum and gold tier suppliers.

One could also argue that too many suppliers would drive down the lead dilution to a point that post fee no supplier is profitable.

I think the investment in Vyapar & Busy Infotech are acknowledgment by management that they would be better off building a walled garden ecosystem for paying subscribers than increasing the subscribers count number.

I would be very curious if these numbers increase materially. MSMEs are resource efficient and price sensitive, and many I think use silver tier strategically during the peak season as rest of the time, subscription price might not justify the value they get.

8 Likes

Is my understanding correct, a low subscriber count isn’t inherently negative. If identical leads are shared across Silver, Gold, and Platinum tiers while buyer numbers are limited, lower-paying members are naturally eliminated by price hikes?