Mehul Johnson has resigned as Managing Director and all other positions from Indiabulls Real Estate

1 Like

Finally NCLT has reserved the order. We might get some conclusion on merger soon.

https://nclt.gov.in/case-details?bench=Y2hhbmRpZ2FyaA==&filing_no=MDQwNDExNjAwMjkzMjAyMg==

7 Likes

I see three scenarios - one of which will play out

- merger takes place at exisitng ratios. the price assigned to india bulls in the merger was Rs. 92. This means it greatly undervalued as per the current market price.

- merger taking place at at higher value. This will mean india bulls real estate has an intrinsic value of more than 92.

- merger not taking place- prob of this happening seems very low. This would still mean india bulls has a lot of value- otherwise it would make no sense that Embassy group buys a stake of roughly 1000 cr in the company at Rs.150 per share

if the merger takes as it is- the market cap of combined entity will be Rs. 55*115= Rs.6300 cr, adding debt gives an EV of around 10,000cr - I feel this is a big undervaluation to the intrinsic value they have.

Disc- Invested

9 Likes

Partial or Incomplete information is always harmful as this might mislead people to act irrationally.

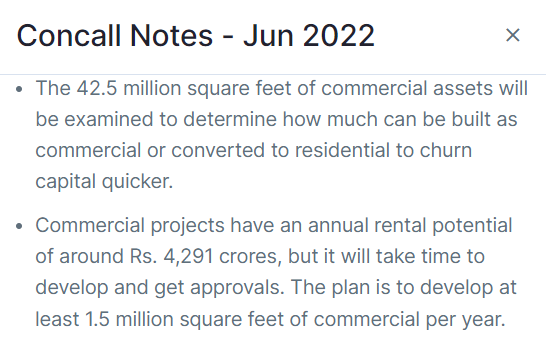

With 1.5 Million square feet of commercial development it would take close to 30 years to fully monetize the “potential” 42.5 million square feet and hence the “peak annual rent potential” of 4,291 Cr. Even at a liberal 12X EV/EBITDA the 51,492 Cr of “value” is 30 years hence.

11 Likes

Its a paid article, a summary of the content is

- Details of the order passed by NCLT, already discussed above

- Next steps according to unnamed sources - IBREL will be challenging the order before NCLAT. It realizes that it will be a complex process and is already working towards it.

Even after it became evident a few months ago (after reading the NCLT orders during the proceedings) that the valuation exercise was a joke and the swap ratio was decided to benefit Embassy, I was hoping that NCLT approves the merger, obviously with a hope to recoup my losses.

Mr. G was never known for good Corporate Governance, I had heard that Embassy’s Mgmt was good. Hence I bought. Very expensive lessons learnt

a) never buy based on hope/story - Chor bane Mor

b) never buy a stock if the management is a known crook, even if its an outgoing one

c) never buy if a stock is very popular on Twitter with many ‘Gurus’ calling it special situation stock

Obviously, behind the sham valuation exercise must have been a quid pro quo between G and V (something like - the underpriced selling of IBREL land to G’s unlisted companies)

Both G & V have been caught with their hands in the cookie jar and if what’s in the article is true (actually I just saw the company has confirmed), they are so shameless that instead of atleast now doing the right thing, they want to appeal to NCLAT. Wow!

I am not a legal or M&A expert so some of the below might be naive, I have been wondering that eventhough NCLT has not approved the merger, but for all senses and purposes IBREL is headed by Embassy Management for many months, so why

A) They have not been running IBREL like a proper going concern, they hardly did any business since last couple of quarters. All they have been doing is selling some land parcels and paying out debt. As far as I know, they have not even announced when the Q4 results will be declared.

B) If their excuse for not launching any new projects in the last few months is that they want the new projects to be under the Brand name of Embassy, what stops them from changing IBREL name to Embassy XXXXX? You don’t need NCLT approval to change names, no?

C) Both the parties have made IBREL stock radioactive, no big party in the stock market will be willing to touch it with a barge pole, so why don’t the Embassy management raise their stake via Open market rather than playing games, especially after being called out by IT dept and NCLT. I know the earlier mechanism was cashless for Embassy management, this will involve outgo of cash of around 1000 cr (as per current valuation) to increase stake by around 30%. I see why they wont do it - why pay 1000 cr when you can have it cashless by just a) swapping shares for free with your inflated shares of NAM b) paying off G by letting him buy IBREL assests for dirt cheap and letting him not pay back IBREL loans Too bad for them that IT dept came in to spoil their well laid out plan

D) Right thing to do - As they raise their stake via legal means (if they do), they can run IBREL business properly and then later amalgamate NAM Estates when they have done their valuations properly (if they are still interested). Why delay and run down IBREL? So that swap ratio is favorable to Embassy? A loss-making IBREL will fetch them a favorable swap ratio (once NCLAT also rejects the request and they have to re-do the swap calculations)

I know some of the IBREL shareholders like to see the positive side. Apologies if you find anything I have written offensive. My hope was that if Embassy Management is as honorable as they were made out to be by many when the news of the merger news came out, they will atleast now do the right thing. But seeing them going ahead to NCLAT disappoints me. I hope I am wrong and its indeed the right step and the Management is really better than what I think.

I prefer to be wrong and rich rather than proven correct and lose money.

24 Likes

Any Update about the hearing yesterday ?

1 Like

INDIA BULLS REALESTATE(CMP - 95) - Great Turn around in Infra Sector

THESIS :

- Looking Like A Very Good Turnaround Candidate

- Which Can Be A Big Outperformer Going Forward

- Would be very interesting to track this- please have a read on the entire tweet

-Institutions might have taken a huge delivery in this counter yesterday - Massive delivery volume of shares worth 808 CR VS Market Cap of 4870

Reasons :

1)The company has a massive land bank which is sufficient for proposed development over the next 5-

7 years. Unsold inventory stands at 10,612 CR Vs Market Cap Of 4,870 CR.

This provides a good revenue visibility

- New management has taken over the company since March 2023. The New Management is

committed to have the highest level of transparency and Corporate Governance standards. - Third reason why I am very bullish is that company aims to be net debt free by the current FY.

#indiabullsrealestate #IBrealestate #infrasector #upmove

3 Likes

Could you please share as to how did you arrive at 115 cr shares?

Can u please point me to the posts in Twitter, I am not able to find your posts there. Many thanks.

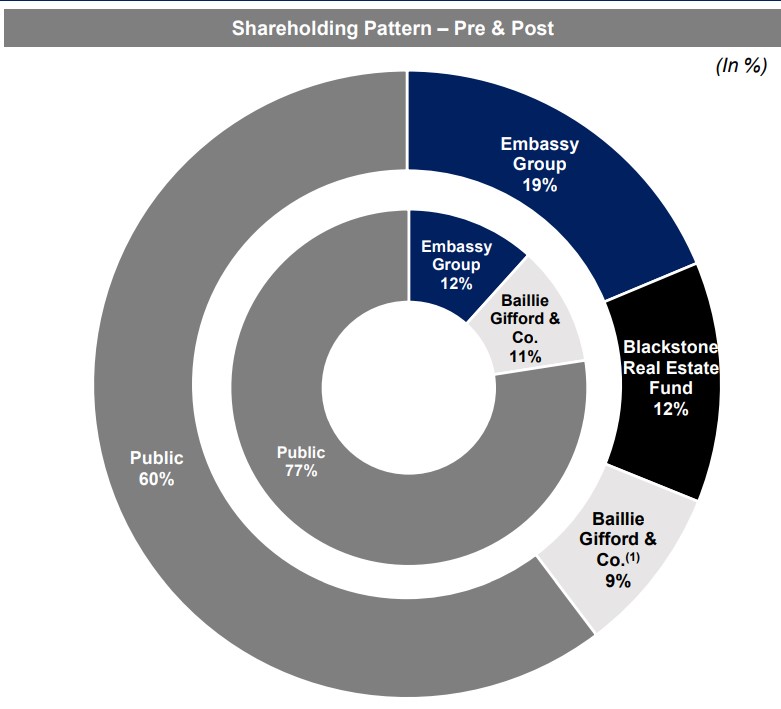

Preferential allotment by IBREL

Hello nJain1983…

agree with your observations. I being a chartered accountant used to be quite interested in merger ratio calculations . But yes … there seems a lot hiding under the carpet…

But real estate stocks are in a boom and in a boom retail investors get sucked into cheap sastha stories.

Malolan

1 Like

Change in name to Equinox India Developments Ltd

1 Like

2 Likes

Anyone knows why the share price has been constantly falling from the last week? It has fallen below its 50 day SMA & EMA. I could not find any news or other information regarding this apart from the Rename which happened in the month of June.

1 Like