Nam estate and embassy debt and book value

Total debt will be around 5000 cr

Nam estate and embassy debt and book value

Total debt will be around 5000 cr

Debt of 4270cr (850cr for 13% stake embassy bought in Indiabull while announcing merger)from embassy side is brought into merged entity. And indiabull is already net debt free. Combined entity debt of 4250cr is looks encouraging. And this is as per the mgmt guidance of achieving 3500cr debt by fy23 . If they achieve 2000-2500cr net debt by fy24 then it looks extremely good

Regards,

Sathish

Hi, saw on the SEBI website that AP HC threw out its own earlier verdict of directing SEBI to re-look into the merger. It agreed with IB/NAM that AP HC didn’t have jurisdiction over the case and said that it should be left to NCLT to decide.

You can read the judgment here

https://sebi.gov.in/enforcement/orders/nov-2022/order-of-the-hon-ble-high-court-of-andhra-pradesh-at-amaravati-in-w-a-no-832-2022-indiabulls-real-estate-limited-and-2-others-vs-dhanekula-dharanish-and-sebi_65775.html

Assume this means further delay to merger

Not really, it says AP high court case is not an obstacle. All depends on NCLT case today

No, it means atleast 1 hindrance has been removed. But now I see that BSE is also listed as one of the petitioners in the ongoing case. Today if the case is heard, BSE’s lawyer will also participate. Maybe yesterday’s intimation to the exchange (BSE) about the Assets & Liabilities of NAM Estate is related to BSE’s participation in the NCLT hearing.

Hoping that the ongoing case gets concluded soon but there are too many parties involved - Dhanekula Dharanish, IT Dept now BSE. In the cause list we can see, so many cases related to IBREAL & NAM merger, are to be heard together. So l guess we need to be patient. Firstly, lets hope that the case is heard today. Its not even part of the Priority List (don’t know whats the basis cases are listed as Priority/Ordinary).

What happened to NCLT hearing today? Any update.?

The price is saying again adjournment (:

Yes. Adjourned to Feb 3rd.

https://nclt.gov.in/case-details?bench=Y2hhbmRpZ2FyaA==&filing_no=MDQwNDExNjAwMjkzMjAyMg==

Disc: IBREALEST is my 2nd biggest position, I am offlate starting to feel a bit uncomfortable about my decision. Posting here my reason for both - investing initially and why feeling unsure now.

Why did I Buy?

Why I am feeling unsure now?

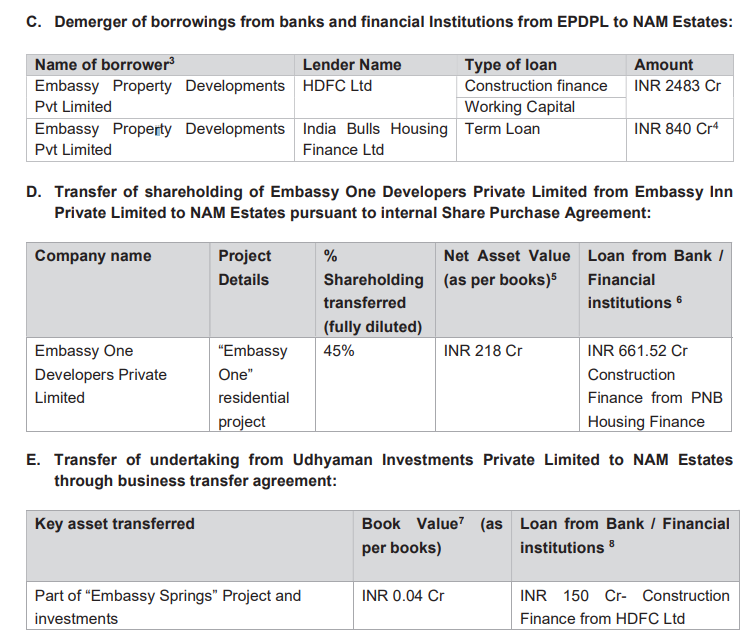

While the case dragging on may not be the Managements’s fault, the following is the real reason what’s making me have second thoughts - At the time of the merger announcement I was happy that bad reputation of IBREAL will be overtaken by Embassy goodwill, but now the picture has completely changed. It seems to me that Debt free & asset heavy (IBREAL) is being merged with a company with heavy debt and shaky cashflows (NAM). Even the debt (850 cr by IB Housing) used to buy SG’s IB stake will be on the merged entities’ books. So, its like a LBO transaction. In essence we the shareholders of the merged entity will be footing the bill of SG’s stake sale (This I deduced from the latest filing on BSE, related to NAM’s Assets & Liab. I may have misunderstood this, please correct me if you are sure that I am wrong). Embassy Management has been candid in stating that their plan to reduce debt (at least partially) is by selling IB landbanks. If my inferences are true then what are the current shareholders of IBREAL getting after we have paid off SG? NAM’s debt, dodgy cashflows (Embassy is late in payment of many of its loans - source: Embassy AR) is all I see now.

Recently IBREAL sold 35 acres of land in Sec 104 near Dwarka Expressway to SG’s entities for around 240 cr. What will SG do with this land if his intention was to leave RE (thats why he sold out of IBREAL, right?). Also, 240 odd cr for 35 acres is not even 7 cr per acre. I am no RE expert but to me it seems a very low price for land near Dwarka Expressway which is touted as one of the hottest growth areas in NCR. Since Gehlauts are no more classified as Promoters of IBREAL, there is lesser scrutiny for the deal to be at arms length from the regulators (assuming they care). For me this deal doesnt pass the smell test. Also, what about the hefty amount SG owed to IBREAL for the UK property which SG had promised Mr. Virwani that he will pay by Dec 2022. Mr. Virwani had said that he believed SG will come true on his promise. I am yet to see any exchange filing regarding the amount being repaid.

Sorry for the long post. I will be very happy if what I have written turns out to be FUD and the merger goes through soon and the merged entity is indeed strong fundamentally.

I would love to see counterarguments from other participants here.

Best wishes.

Hello @njain1983 . Thanks for the great post, would be great if you could also include a few supporting links for others to read along.

I believe the key thesis, which has been repeated ad nauseum, is two aspects,

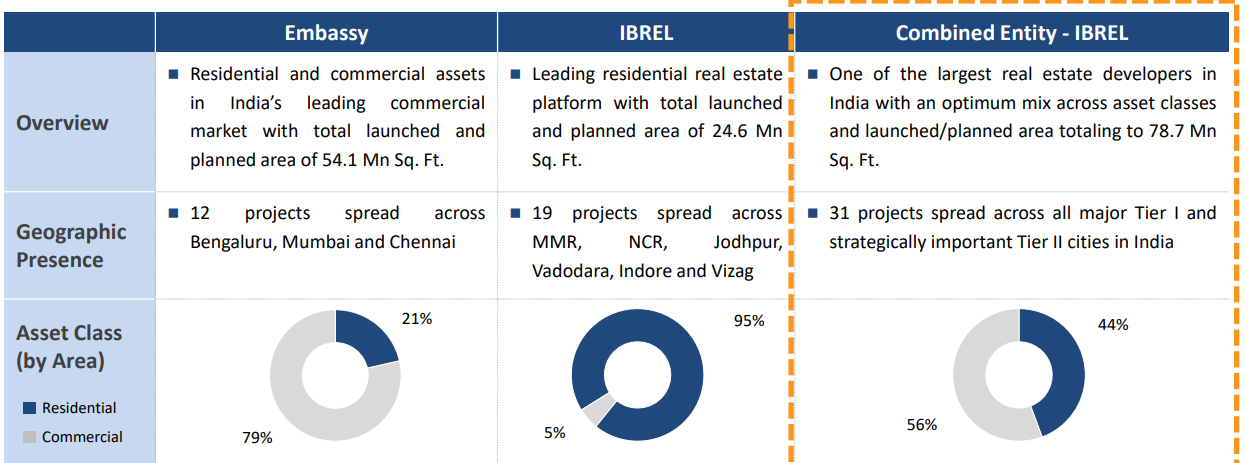

Moving to a very balanced residential + commercial mix through the merger

- 44% residential & 56% commercial link

The ability of the Embassy group to

a) manage liquidity for completion of IBReal residential projects & realize the surplus from projects

b) monetize their planned commercial portfolio through their listed REIT arm. 43mn sq ft

It seems from the latest court proceedings of 05.01.2023, there are multiple aspects which were discussed and hoping the next hearing on 03.02.2023 will assume significance towards concluding majority of these.

(1) Income Tax department trying to wrap around their findings from Embassy raids from June 2022 and trying to link them to IBReal - which they are apparently not.

(2) Violations of disclosure norms and other aspects filed by minority shareholders. Again if Mr. Dharanish is acting a front end for some other interested party remains to be seen, but disclosures obtained because of this activist movement has been beneficial for minority shareholders - to say the least.

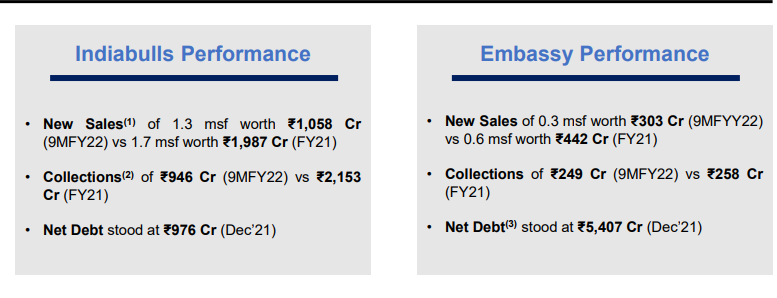

Yes, can’t agree more. We have seen a very high debt number from Embassy being floated towards December 2021, of 5,407 Cr along with all cash flow issues you highlighted.

Subsequently from the Jan 4, 2023 disclosures, we have seen this coming down to 4300 Cr.

Again the end use of debt is debatable because the IB Housing term loan originated in April 2020 as per the filing, while the promoter buyout happened in 2019.

Not all of the IBReal landbank is promisable and they will monetize certain parcels as was highlighted in the last conf. call back in June 2022. Going back to the buy thesis, I do not see the core thesis being derailed from this non-core asset monetization.

Very fair arguments, given Sameer Gehlaut’s minority stake in Dhani and “Promoter” tag not being applicable.This could indeed be some sort of quid pro quo.

However, their realization of 240 Cr for 35 acres is double the last revaluation disclosure from Q2FY23 filings

IBReal sold the Hanover Square property in 2019 to SG for £200 (purchase price £162 Mn).

From the Jun-22 concall only £60mn is left unpaid at that time.

SG is focusing on the London RE market through this new company Clivedale London, launching the new service apartments and premium hotels near the Hanover Square area. So I am assuming the remaining dues are recoverable for IBReal.

Finally, someone has looked into the recent sale transaction of 35 acres of land in Gurugram for 240 crs. It is behind a paywall so I couldn’t read. If someone has access, it will be great if you can summarize what the reporter has mentioned. Hoping against hope that there is a plausible explanation

The article has raised several questions, most of which IBREL spokesperson has answered. Now whether you trust the explanation is upto you.

Summary of IBREL’s response published in the article:

Pertinent points raised by the Journalist:

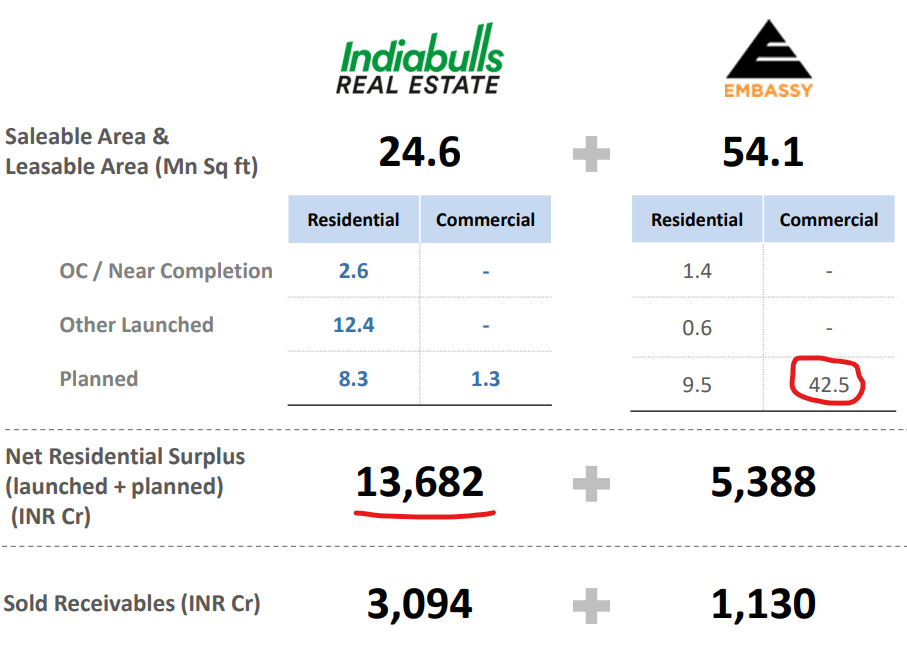

Even as late as Nov 2022, in the latest Investor presentation IBREL mentioned that net surplus from One Indiabulls project was Rs. 1868 cr (ref: pg 19).

(My comment: How come within a month IBREL found that the piece of land is worth only 240? Also, IBREL sold half of land 2 yrs ago for 140 and have been trying to sell rest, then why you mentioned in the Nov presentation that the project will fetch you net surplus of Rs 1868 cr, when you knew that the land wasnt finding any takers? How reliable is the rest of Net surplus figure?)

As per Aug presentation (ref pg: 12), Gross Development value (anticipated revenue) of the land was reported to be Rs 880 cr

(My comment: Land in acres is mentioned as 25 not 35. In Aug you say its 880 cr but in Nov presentation (ref: pg 19) you say unsold inventory and net surplus is 2926 cr and 1868 cr respectively )

IBREL made investments of Rs 534 cr in one of the two subsidiaries sold, including 110 cr just 2 weeks before the sale transaction.

(IBREL response: There was no new investment and only a loan was converted to equity so that the sale transaction could be completed. Now there is no loan/debenture to be redeemed/converted into equity pending between IBREL & sold subsidiary.) Journalist disputes this claim based on RoC papers

My take: Maybe what IBREL is stating as the reason for the undervaluation of the deal is accurate but why have they been throwing around such big Net Surplus numbers around eventhough they knew the issues plaguing the land?

Disclosure: IBREL is a big position in my PF. I have not yet made up my mind to sell and wait for clarity or continue holding. I understand RE space, especially in India, is muddled and sometimes we need to ignore a few things and not expect everything to be Kosher.

Thanks, @njain1983 for putting up all details here. 3 clear takeaways for me

Good to see that there is no dubious transaction with Dhani Services (SG entity). The prior deal with Hero group gives confidence and the realized land value is 2X the fair deal valuation from 2021, as highlighted in my previous post.

Gurugram not being in focus. The clarity and asset monetization strategy are helpful given Embassy’s focus on Mumbai & Bangalore. Surplus realization is anyways far-fetched and needs to be considered with buckets of salt. I am sure the 240 Cr cash from the transaction will prove useful for near-completion projects.

Management walking the talk. From the recent monetization deals to making IBReal net debt-free, management is showing proactiveness. I believe a lot of new launches are planned in Mumbai with the new branding once the court proceedings are over.

The funny thing is a lot of media and court activism is being seen as we are nearing the final closure of the merger deal. If it is indeed with vested interest from competitors, we have a winning candidate on hand…

Yes, I am also now less worried about the recent sale transaction.

Regarding the court activism, did you notice that a new party Tejo Ratna Kongara (CA No. 8/2023) has done a share purchase agreement with Sh. Dhanekula Dharanish, the minority shareholder who has filed cases against the merger. Now Tejo wants to replace Dhanekula in the original case (CA No. 192/2022). Will be interesting to see in the next hearing what is Tejo’s objective. I do have a speculation (which if true will result in a speedier resolution), but since this forum is only for hard facts, I will keep it to myself ![]()

Any updates on NCLT hearing ? There was a hearing today. No updates on nclt website as of now.

Order Listed for 1st March , on NCLT website.

Why a minority investor wants to stall the long pending Indiabulls Real Estate-Embassy Group merger

The objections were raised by the minority investor before the NCLT’s Chandigarh bench, which is also the final authority to give final nod to the proposed merger.

Apart from the minority investor, the income tax department has also filed an objection against the said merger pertaining to the internal scheme of arrangement of NAM Estates.

The NCLT, Chandigarh will next hear the case on March 1, 2023.